关键词 > ACF518

ACF518 CORPORATE FINANCIAL REPORTING MAY 2024

发布时间:2025-09-24

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

UNIVERSITY EXAMINATIONS: MAY 2024

Module Code: ACF518

Module Title: CORPORATE FINANCIAL REPORTING

CRN: 50702

Time Allowed: 3 HOURS

SECTION A – Answer BOTH questions

Question 1

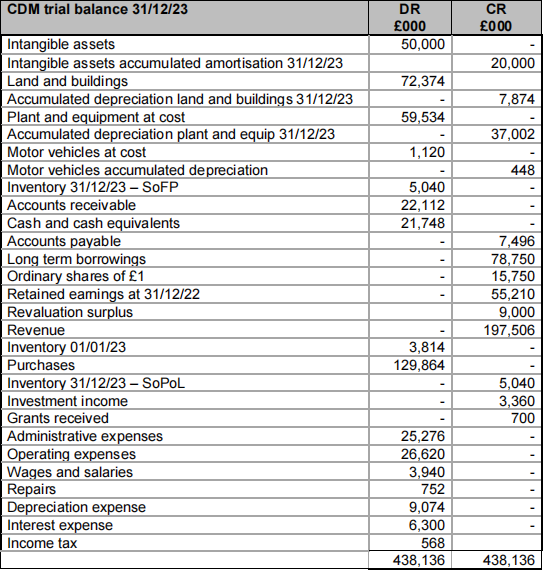

CDM Plc (CDM) drew up the following trial balance as at 31/12/23

Additional information:

1. CDM have carried out an impairment review and have identified two items which may be impaired as follows:

A piece of land purchased on 01/01/2015 for £1,500,000. On 31/12/2018 the land was revalued to £2,500,000 but due to a downturn in the market at 31/12/23 it has a fair value less costs of disposal of £ 1,200,000. (Note: Land is not depreciated).

A piece of equipment

The equipment has a fair value less costs of disposal of £200,000 and a value in use of £250,000. (6 marks)

2 Due to an arithmetic error inventory at 31 December 2022 was understated by £300,000. Any adjustments to comparative figures must be made manually, adjustments to the prior year’s trial balance will not feed through to the current year. CDM does not pay any dividends and taxation may be ignored. (6 marks)

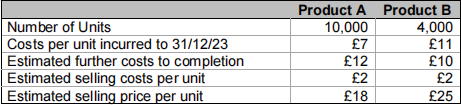

3 Included in closing inventories are 10,000 units of product A at a total cost of £70,000 and 4,000 units of product B at a total cost of £52,000. Relevant information on product A and product B is provided below:

(6 marks)

4 CDM operates in a regulated industry. On 1st January 2023, it purchased a licence allowing them to operate in a new geographic area. The licence cost £ 1,500,000, lasts for 20 years and has been charged to operating expenses. (6 marks)

5 CDM employees are paid monthly in arrears on the 8th of each month. At 31/12/2023 CDM owes staff £300,000 for work carried out from 09/12/2023 to 31/12/2023.

CDM employees are entitled to 30 days paid holidays per annum and may carry up to 5 days leave forward to the following years leave entitlement. At 31/12/2023 a total of 80 days are to be carried forward with associated wages of £20,000.

No entries have been made in the accounts in respect of wages owed or holidays carried forward. (6 marks)

Required:

Explain the required treatment of items 1 to 5 above. Your explanation should refer to relevant accounting standards and include any journal entries necessary to correct the trial balance.

Round figures to the nearest £000.

[Total: 30 Marks]

Question 2

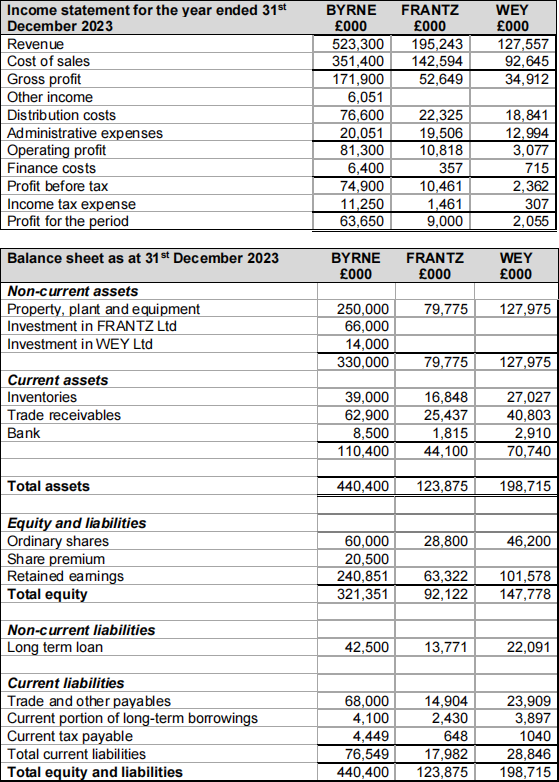

The financial statements of BYRNE Plc (BYRNE), FRANTZ Ltd (FRANTZ) and WEY Ltd (WEY) are presented below.

Additional information:

1. BYRNE acquired a 25% shareholding in WEY on 01/09/2023. The Directors of BYRNE do not have a role in the day-to-day running of WEY.

2. During the period 01/09/2023 to 31/12/2023 BYRNE sold goods to WEY for £1,200k at a margin of 40%. At the year-end WEY still held £250k of these goods in inventory. BYRNE’s receivables include £300k due from WEY. This agreed to the amount included in WEY’S trade payables.

3. BYRNE acquired 23,040k £ 1.00 ordinary shares in FRANTZ on 01/01/2022. The retained earnings at that date were £35,000k; the fair value of FRANTZ’s net assets was the same as their book value, with the exception of property. The market value of the property was £4,000k above the book value. At acquisition, the property had a remaining useful life of 25 years, depreciation is charged to administrative expenses. The fair value of the remaining 5,760k shares was £12,000k on 01/01/2022. BYRNE values non-controlling interests at fair value when calculating goodwill on acquisition of subsidiaries.

4. Since its acquisition BYRNE has sold goods to FRANTZ. FRANTZ’s Trade payables include £1,200k owed to BYRNE, this matched BYRNE’s trade receivables; total sales to FRANTZ in the year were £8,000k. BYRNE sells goods to FRANTZ at a mark-up of 25%. At 31/12/2023, FRANTZ still held 20% of these goods in inventory.

5. An impairment test on the goodwill of FRANTZ, conducted on 31/12/2023, concluded that goodwill on acquisition is now impaired by £3,000k. The value of the investment in WEY was not impaired.

6. FRANTZ paid dividends of £1,500k relating to the period from 01/01/2023 to 31/12/2023. All dividends receivable by BYRNE have been credited to other income in the income statement above.

7. All items in the above income statements are deemed to accrue evenly over the year.

Required:

Prepare the consolidated income statement for the BYRNE Group for the year ended 31/12/2023 and a consolidated balance sheet as at that date. (Show workings including ALL JOURNAL ENTRIES REQUIRED)

Round figures to the nearest £000. (30 marks)

[Total: 30 Marks]

SECTION B – Answer two questions from three

Question 3

VALT Plc (VALT) manufacture washing machines. They are in the process of finalising their financial statements for the year ended 31 December 2023. There are a number of areas which may require provisions as follows:

(i) VALT machinery requires a major overhaul every five years, costing c£2m each time. The company has decided to spread this cost over the four years preceding the overhaul, the first years provision has been recognised as follows:

(ii)

(3 marks)

(iii) VALT has been accused by local environmentalists of polluting the local river, causing major damage to salmon stocks. The company is contesting this on the grounds most of the damage was caused by farmers overusing phosphates. VALT’s lawyers feel they have a 70% chance of losing the case and being forced to pay to rectify the damage which will cost £ 1,200,000. VALT has therefore made a provision of £ 1,200,000 * 70% = £840,000 and charged it to other expenses. (4 marks)

(iv) VALT offers a 12-month warranty on goods which are not performing to the customers satisfaction. From past experience, 80% of customers make no warranty claim, 12% make claims which cost VALT £200 to repair each unit and 8% make claims which cost VALT £300 to repair each unit. Total sales for the year ended 31 December 2023 were 300,000 units. VALT has no current provision for warranty claims, expensing each claim as it is received. (4 marks)

(v) In a bid to tackle increasing energy costs VALT installed a wind turbine on 01 January 2023 at a capitalised cost of £1,000,000. As part of the planning conditions the wind farm must be decommissioned at the end of its 5-year life and returned to a green field site. It is estimated the decommissioning and site clean-up costs will be £100,000. There have been no amounts recognised in the financial statements regarding site clean-up. The wind farm is to be depreciated straight line over 5 years.

VALT have calculated a pre-tax discount rate of 6% on long term provisions.

(6 marks)

Required:

(a) Set out the definition of a provision as per IAS 37 Provisions, contingent liabilities and contingent assets, along with the criteria IAS 37 sets out for recognising a provision. (3 Marks)

(b) Applying the principles set out in IAS 37, determine if the above items have been treated correctly, provide an explanation for your decision and, where necessary, indicate the correct treatment and any journal entries required.

In the case of part (iv) prepare a schedule detailing the treatment of the site clean-up costs and associated provision (if any) over the life of the windfarm.

Round figures to the nearest £000. (17 Marks)

[Total: 20 Marks]

The International Accounting Standards Board (IASB) has recently released a new standard on leasing, IFRS 16.

(a) Required:

Explain why the IASB has felt it necessary to rethink the accounting treatment for leasing contracts and briefly outline the approach they intend to take on accounting for simple leases. (2 Marks)

(b) TORINO Plc (TORINO) has a year end of 31 December. On 1st January 2022 TORINO leased a machine from ROMA Ltd (ROMA). The machine cost ROMA £900,000 to manufacture and had a fair value of £ 1,500,000 on 1st January 2022.

The agreement contained the following clauses:

Lease term: 3 years

Deposit £500,000 (Paid 01/01/22)

Annual rental, paid in advance: £260,000 (payments to be made 01/01/22, 01/01/23, 01/01/24)

Interest rate implicit in lease: 6%

• The lease is cancellable only with the permission of the lessor. The expected useful life of the machine is 10 years, and the machine will be returned at the end of the lease term.

• Included in the annual payment is £ 10,000 to cover maintenance and insurance paid by the lessee.

• TORINO also paid £20,000 on 01/01/2022 for the drawing up of the lease agreement.

• No entries have been made to record the lease.

Required:

(i) Classify the lease for the lessee based on guidance in IFRS 16 Leases. (1 Mark)

(ii) Prepare extracts from the financial statements of TORINO, showings all workings, to illustrate how TORINO Plc should comply with IFRS 16 over the duration of the lease. (9 Marks)

(iii) Draw up the journal entries to record the lease of the machine in the books of TORINO Plc for the year ended 31 December 2022. (4 Marks)

(iv) Draw up the journal entries to record the lease of the machine in the books of TORINO Plc for the year ended 31 December 2023. (4 Marks)

Do not round figures, show in £.

[Total: 20 Marks]

“In a future society, successful firms are going to be those that can link together the environment, society and their economic prosperity. They will look to the long term and find resources that are sustainable and assurance that those costs are not going to skyrocket. ”

Michael Radcliffe, KPMG Director Global Sustainability Network

Required:

Explain what is meant by the green revolution in financial reporting and critically evaluate the attempts by the accounting profession to achieve greater transparency in reporting of environmental issues. (20 Marks)

[Total: 20 Marks]