关键词 > 125.350

125.350 Financial Risk Management Semester 2, 2025

发布时间:2025-09-19

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

125.350 Financial Risk Management

Semester 2, 2025

Option pricing and option trading strategies

Total marks: 100

Due: 11pm 06th October 2025 (NZST)

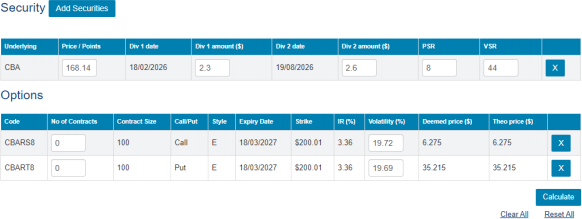

Pick one stock from the ASX50 list (stock code is available here:https://www.asx50list.com/) and search for its options in https://www.asx.com.au/marginestimator/. You can choose any pair of European call and put options with the underlying asset as the stock you picked, whose expiry date are in March 2027. As an example, you may see information like this (please note the date that you extract the information):

Tasks:

1. When choosing the call/put option pair, do not use the pair exactly matching the given example. Notes:

a. Find the pair with same underly stock, contract size, expiry date, strike price and IR.

b. It has to be the European option,

c. The volatility levels are approximately the same.

d. Be noted about the dividend payments when working out the option pricing.

2. [10 marks] Use the Black-Scholes Option Pricing model to verify the theoretical price of the options as seen in the “Theo Price” column. Verify the Put-Call parity relationship.

3. [30 marks] Use the information of the “volatility” column to set up the two-step Binomial Tree and work out the option prices using the Binomial Option Pricing Model.

4. [60 marks] Consider that you, as a trader, are predicting about the future scenarios in the stock market in March 2027. Design an appropriate trading strategy using more than one option in each of the following scenarios that you expect, and illustrate each strategy’s payoffs via payoff diagrams (note that you can choose available options other than using in task 2 and 3):

a. The stock you picked will increase (bull market).

b. The stock you picked will decrease (bear market).

c. The volatility of the stock you picked will be small.

d. The stock you picked will experience a large move, but you do not know in which direction the move will be.

e. The stock you picked will experience a large move, and you bet that an increase in the stock price will be more likely than a decrease.

f. The stock you picked will experience a large move, and you bet that a decrease in the stock price will be more likely than an increase.

Note:

• This is an individual assessment. You MUST complete this assignment by your own. Discussion with your peers to learn, verify and extend your understanding is allowed. However, the works MUST be done by yourself. Any evidence of the plagiarism, same works submitted by different students will be marked as Fail for the assessment.

• You can do your work in excel and report in forms of Tables, Diagrams, and Figures in the word document. Please also submit your excel worksheet together with your word document.

• Clearly explain the rationale of your choices for trading strategies and provide description on how the trading strategies work depending on the scenarios of the stock prices.