关键词 > ACF518/ACF566

ACF518 / ACF566 CORPORATE FINANCIAL REPORTING JAN 2023

发布时间:2025-08-13

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

UNIVERSITY EXAMINATIONS: JAN 2023

Module Code: ACF518 / ACF566

CRN: 25062/31115

Module Title: CORPORATE FINANCIAL REPORTING

SECTION A – Answer BOTH questions

Question 1

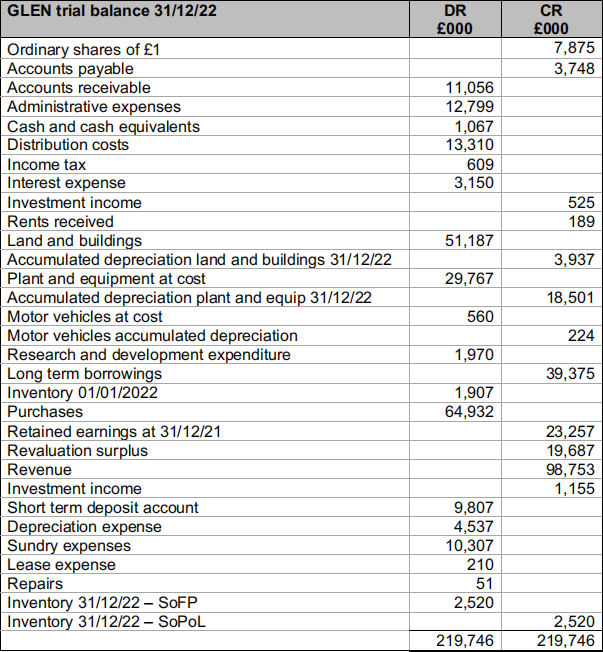

GLEN Plc (GLEN) drew up the following trial balance as at 31/12/22

Additional information:

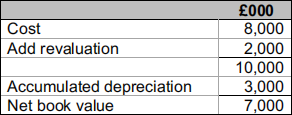

1. Due to a downturn in the property market, the recoverable amount of one of GLEN’s properties has fallen below its net book value. The property currently has a fair value less costs of disposal of £4,500k. It has been included in the financial statements as follows:

(5 marks)

2 On 01/06/2022 a customer tripped on an uneven floor in GLEN’s premises and broke their arm. They subsequently sued GLEN, claiming £100,000 in damages. GLEN had CCTV footage showing the customer had been looking at their phone at the time they tripped. As a consequence, GLEN’s lawyers felt it likely the claim would not be successful and no provision was made. The case went to court on 05/01/2023. The customer admitted looking at their phone at the time of the incident but argued GLEN should have expected customers to behave in this manner and ought to have smooth flooring. The also showed they had been looking at an order update sent by GLEN when they tripped. In light of this the judge ordered GLEN to pay £80,000 damages to the customer by 31/01/2023. (5 marks)

3 GLEN’s closing inventory was £2,520,000 valued at cost. Included in this are inventories which cost £150,000 but were damaged by rain. This inventory may be sold as scrap for £80,000 but GLEN will incur selling costs of £10,000 to realise this. (5 marks)

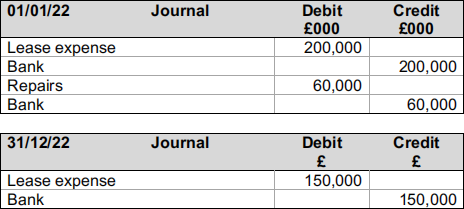

4 On 01/01/22 GLEN acquired an item of plant under a 3 year lease agreement. The agreement had an implicit finance cost of 4%. GLEN made an initial payment of £200,000 at the inception of the agreement and pays further annual payments of £150,000 on the 31/12/22, 31/12/23 and 31/12/24. GLEN incurred expenses of £60,000 re shipping and installation of the plant. The plant has a useful life of 5 years. Plant and equipment is depreciated on a straight line basis.

The only entries in the accounts are as follows:

(10 marks)

5 GLEN’s holiday year runs from 1st January to 31st December each year. All staff receive 30 days paid holidays per annum. Staff are allowed to carry forward up to 5 days leave into the subsequent year. At 31/12/2022 staff were carrying a total of 124 days, with a wages value of £26,000 into the year ended 31/12/2023. (5 marks)

Required:

Explain the required treatment of items 1 to 5 above. Your explanation should refer to relevant accounting standards and include any journal entries necessary to correct the trial balance.

Round figures to the nearest £000.

[Total: 30 Marks]

Question 2

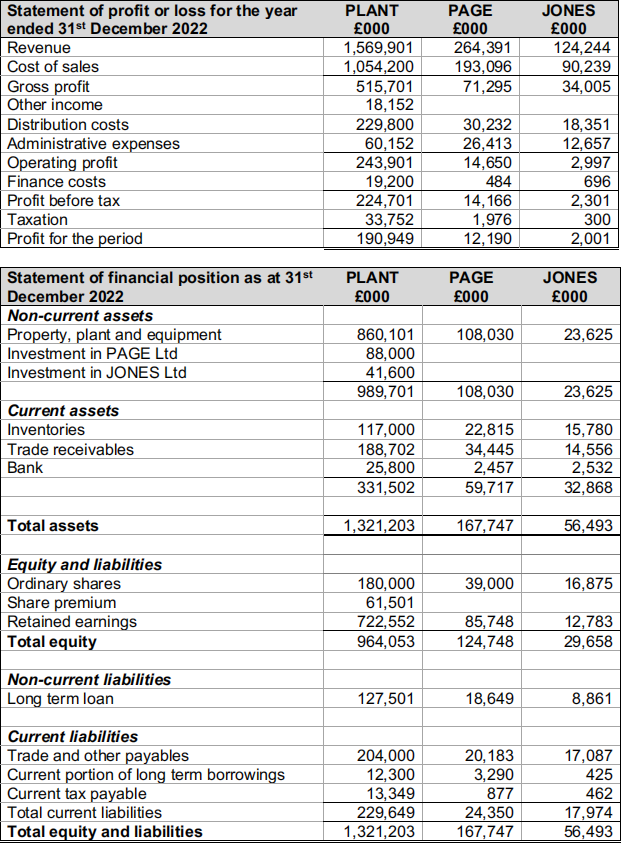

The financial statements of PLANT Plc (PLANT), PAGE Ltd (PAGE) and JONES Ltd (JONES) are presented below.

Additional information:

1. PLANT acquired a 40% shareholding in JONES on 01/09/2022. The Directors of PLANT do not have a role in the day-to-day running of JONES.

2. Since acquisition, JONES sold £1,000,000 of goods to PLANT at a margin of 20%. At the year end half these goods remained in PLANT’s closing inventory, JONES’s accounts receivable include £300,000 owed by PLANT.

3. PLANT acquired 15,600,000 £1.50 ordinary shares in PAGE on 01/01/2017. The retained earnings at that date were £32,000,000; the fair value of PAGE’s net assets was the same as their book value, with the exception of property. The market value of property was £15,000,000 above the book value. At acquisition, the property had a remaining useful life of 15 years, depreciation is charged to administrative expenses. The fair value of the remaining 10,400,000 shares was £36,000,000 on 01/01/2017. PLANT values non-controlling interests at fair value when calculating goodwill on acquisition of subsidiaries.

4. Since acquisition PAGE has become a customer of PLANT. PLANT’s accounts receivable include £4,800,000 owed by PAGE; total sales to PAGE in the year were £8,000,000. PLANT sells goods to PAGE at a mark-up of 25%. At 31/12/2022, PAGE still held 20% of these goods in inventory.

5. An impairment test on the goodwill of PAGE, conducted on 31/12/2022, concluded that goodwill on acquisition is now impaired by £10,000,000. The value of the investment in JONES was not impaired.

6. PAGE paid dividends of £2,400,000 relating to the period from 01/01/2022 to 31/12/2022. JONES did not pay dividends during the year ended. All dividends receivable by PLANT have been credited to other income in the statement of profit or loss above.

7. All items in the above income statements are deemed to accrue evenly over the year.

Required:

Prepare the consolidated statement of profit or loss for the PLANT Group for the year ended 31/12/2022 and a consolidated statement of financial position as at that date. (Show workings including ALL JOURNAL ENTRIES REQUIRED)

Round figures to the nearest £000. (30 marks)

[Total: 30 Marks]

Question 3

IAS 37 Provisions, contingent liabilities and contingent assets has applied for accounting periods starting after 01 July 1999.

Required:

(a) Set out the definition of a provision as per IAS along with the criteria it sets out for recognising a provision. (4 marks)

BARRI Plc (BARRI) is a conglomerate business with a year end of 31/12/2022 working across many different industries. The assistant accountant has asked for your assistance with the following issues:

1. BARRI supply concrete to building firms. At the beginning of 2022 a building company was supplied with a faulty batch of cement. As a consequence a number of houses they constructed will have to be demolished and rebuilt. The builder is suing BARRI for £1,500,000, the selling price of the houses. BARRI’s solicitors have examined the case and the builder appears to have sufficient evidence to show the problems were caused by the cement BARRI supplied. The solicitors feel it is almost certain BARRI will have to pay damages, but the most likely amount to be paid is the cost of constructing the houses, £1,000,000 rather than the selling price. The case is forecast to cost BARRI £100,000 in solicitors/architects/engineers fees.

BARRI in turn are suing the company who supplied the cement to BARRI. BARRI’s solicitors feel they have and 80% chance of success, with £700,000 the most likely amount they will receive. (6 marks)

2. BARRI manufactures and sells widgets. They offer warranties on goods which are not performing to the customers’ satisfaction. From past-experience, 80% of customers make no warranty claim, 15% make claims which cost BARRI £500 to repair each unit and 5% make claims which cost BARRI £2,000 to repair each unit. Total sales for the year ended 31/12/2022 were 10,000 units. BARRI has no current provision for warranty claims, expensing each claim as it is received. (5 marks)

3. BARRI also operate a construction company. They entered into a contract to build a large office block on 01/01/2022. It is a fixed price contract with BARRI receiving £5,000,000 on completion, which is due on 31/03/2023.

Since entering into the contract building costs and labour prices have risen dramatically. BARRI’s total costs to date are £4,000,000 and they estimate it will cost a further £2,000,000 to complete the office block. (3 marks)

4. BARRI has had recent difficulties with its Republic of Ireland factory and are considering closing it down in six months’ time. The Board of Directors has discussed this action at its last meeting but no firm decision has been made. The company estimates the redundancy costs of winding up operations at £400,000. No provision has been made as the factory will continue production until 30/06/2021. (2 marks)

Required:

(b) Explain how BARRI should account for the above under IAS 37 Provisions, contingent liabilities and contingent assets, along with any journal entries necessary to correct the financial statements for the year ended 31/12/2022.

[Total: 20 Marks]

Question 4

PILA Plc prepares financial statements to 31 December each year. PILA has a number of highly skilled employees it wishes to retain and has put two schemes in place to encourage staff retention:

Scheme A

On 01/01/2022 PILA granted share options to 300 employees. Each employee was entitled to 400 options to purchase equity shares (nominal value £1) at £8 per share. The options vest on 31/12/2024 if the employees continue to work for PILA throughout the three-year period. Payment for the shares is due from the employees on 31 January 2025.

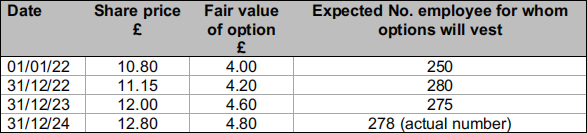

Relevant data is as follows:

Scheme B

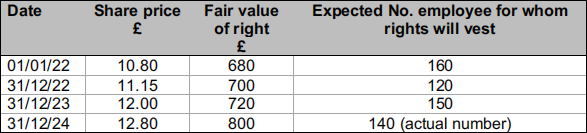

On 01/01/2022 PILA granted 2 share appreciation rights to 200 employees. Each right gave the holder a cash payment of £200 for every 50p increase in the share price from the 01/01/2022 value to the date the rights vest. The rights vest on 31/12/2024 for those employees who continue to work for PILA throughout the three-year period. Payment is due to the employees on 31 January 2025.

Relevant data is as follows:

Required

(a) For both schemes apply the principles of IFRS 2 Share Based Payment to calculate the annual charge to the income statement over the course of the schemes and draw up the extracts from the accounts relating to the schemes for the years ended 31/12/22, 31/12/23, 31/12/24, 31/12/25. (12 Marks)

(b) Draw up journals to record the schemes in each year. (8 Marks)

Do not round figures, show in £.

[Total: 20 Marks]

Question 5

“In a future society, successful firms are going to be those that can link together the environment, society and their economic prosperity. They will look to the long term and find resources that are sustainable and assurance that those costs are not going to skyrocket. ”

Michael Radcliffe, KPMG Director Global Sustainability Network (2002) Required:

Explain what is meant by the green revolution in financial reporting and critically evaluate the attempts by the accounting profession to achieve greater transparency in reporting of environmental issues.

(20 Marks)

[Total: 20 Marks]