关键词 > 110.309

110.309 ADVANCED FINANCIAL ACCOUNTING SEMESTER ONE 2022

发布时间:2024-06-10

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

EXAMINATION FOR

110.309 ADVANCED FINANCIAL ACCOUNTING

SEMESTER ONE 2022

SECTION A: FOREIGN CURRENCY

Scenario Information

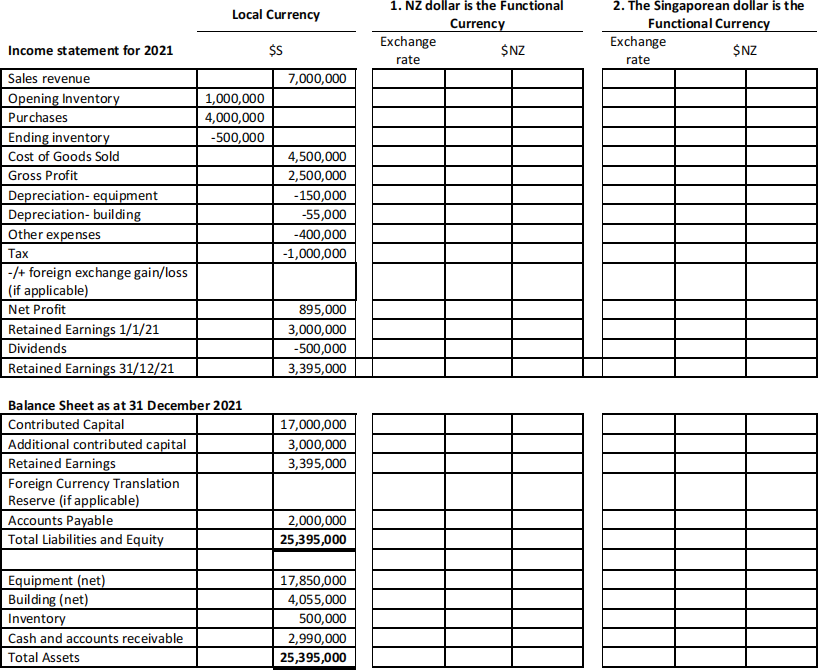

You are the financial accountant at Kiwiana International Ltd (KIL), a New Zealand listed company. On 1 January 2021, KIL acquired all the issued shares of Singapore Ltd (SL), located in Singapore. The CFO of KIL, Jenny Zhang, asked you to prepare the translated financial statements of SL. SL prepares its financial statements using its local currency, the Singaporean dollar (S$).

SL balance sheet on 1 January 2021 is as follows:

S$ 000

Share Capital 17,000

Retained Earnings 3,000

Accounts Payable 6,000

Total Liabilities and Equity 26,000

Equipment (net) 18,000

Inventory 1,000

Cash and accounts receivable 7,000

Total Assets 26,000

The financial statements of SL as at 31 December 2021, the fiscal year end, as well as the relevant exchange rates are provided in the Excel spreadsheet template file for this examination paper.

Additional information:

• Dividends were declared and paid on 1 October 2021.

• The opening inventory was on hand at the time of the acquisition of SL. The closing inventory was acquired on 15 December 2021.

• All the equipment (net) account relates to equipment that was on hand at the time of the acquisition.

• The building was acquired on 15 October 2021.

• On 1 December, KIL contributed additional capital to SL of S$3 million.

• Sales, purchases, and other expenses were incurred evenly throughout 2021.

Question 1

Refer to the scenario information in Section A and answer Question 1 in the Excel spreadsheet template file provided.

Required:

Using the Excel spreadsheet template file provided, translate the SL financial statements for the year ended 31 December 2021 into New Zealand dollars (NZ$), assuming:

a. The NZ dollar is the functional currency of SL. (8 marks)

b. The Singaporean dollar is the functional currency of SL. (8 marks)

Relevant exchange rates were as follows:

1 January 2021: S$1.00 = NZ$ 1.10

1 October 2021: S$1.00 = NZ$ 1.14

15 October 2021: S$1.00=NZ$ 1.16

1 December 2021 S$1.00= NZ$ 1.17

15 December 2021: S$1.00 = NZ$ 1.18

31 December 2021: S$1.00 = NZ$ 1.20

Average 2021: S$1.00 = NZ$ 1.15

Question 2

You presented the two versions of the translated financial statements for SL at a meeting of KIL Board. During the board meeting, aboard member asked you to explain how the exchange differences are presented in the financial statements for both methods and the reasons for such presentations.

Briefly explain how the exchange differences arepresented in the financial statements under the two translation methods and the reasons for the different presentations. (4 marks) [TOTAL = 20 MARKS]

SECTION B: FINANCIAL INSTRUMENTS Scenario Information

On 1 April 2020, North Shore Ltd acquired 100,000 shares of Manuka Ltd as a long-term investment at a cost of $500,000. The year-end market prices of Manuka shares were $6.50 on 31 March 2021 and $5.50 on 31 March 2022.

Question 3

Refer to the scenario information in Section B and answer the following question:

Provide the required journal entries for North Shore Ltd to account for the investment in Manuka Ltd if North Shore Ltd has made the election to account for the equity investment at fair value through other comprehensive income (OCI). (6 marks)

Question 4

Refer to the scenario information in Section B and answer the following question:

If North Shore Ltd has NOT made the election to account for its equity investments at fair value through OCI, provide the required accounting journal entries for North Shore Ltd to account for the investment in Manuka Ltd using fair value through profit and loss. (6 marks)

Question 5

Explain why it is that when the market’s required rate of return is less than the coupon rate being offered on a bond the price the bond will be sold for (its fair value) will be above its face value. (3 marks)

Question 6

What is a financial instrument? State for each balance sheet item whether it is or is not a financial instrument. Briefly explain your answer.

a. Cash and cash equivalents

b. Receivables from customers

c. Inventories

d. Deferred tax asset (5 marks)

[TOTAL = 20 MARKS]

SECTION C: ACCOUNTING AND CULTURE/DIVERSITY Scenario Information

i. “Seventy thousand years ago, HOMO sapiens was still an insignificant animal minding its own business in a corner of Africa. In the following millennia, it transformed itself into master of the entire planet and the terror of the ecosystem … .. We are more powerful than ever before, but have very little idea what to do with all that power” (Harari, 2011, pg. 465-466).

ii. “Every culture has its typical beliefs, norms and values, but these are in constant flux” (Harari, 2011, pg. 181)

Question 7

Refer to the two quotes by author Yuval Harari in the scenario information in Section C and answer the following question:

Discuss the influence of culture on accounting. In your discussion, you are expected to raise at least four well-reasoned points from the following:

• Institutional factors which may influence accounting;

• Examples of how religion influences accounting;

• Hofstede’s ‘cultural dimensions’ which may influence accounting.

You must raise at least one point on each of the above three bullet points, as well as a forward-looking conclusion which relates culture, accounting standards and climate change.

[TOTAL = 10 MARKS]

SECTION D: GROUP/CONSOLIDATIONS

Scenario Information

Luke Ltd had acquired 80 per cent equity in Jack Ltd on 1 July 2012. At that date the capital and reserves of Jack Ltd were:

Share capital $1,500,000

Retained earnings $1,275,000

$2,775,000

At the date of acquisition, all assets were considered to be fairly valued.

Additional information:

1. The management of Luke Ltd measures any non-controlling interest at the proportionate share of Jack Ltd’s identifiable net assets.

2. The management of Luke Ltd believes that goodwill acquired was impaired by $22,500 in the financial year ending 30 June 2021. Previous impairments of goodwill amounted to $168,750.

The following financial statement of Luke Ltd and its subsidiary Jack Ltd have been extracted from their financial records at 30 June 2021.

|

|

Luke Ltd ($) |

Jack Ltd ($) |

|

Detailed reconciliation of opening and |

|

|

|

closing retained earnings |

|

|

|

Sales revenue |

5,175,000 |

4,350,000 |

|

Cost of goods sold |

(3,480,000) |

(1,785,000) |

|

Gross profit |

1,695,000 |

2,565,000 |

|

Dividend revenue - from Jack Ltd |

558,000 |

- |

|

Consulting fee revenue |

198,750 |

- |

|

Profit on sale of plant |

262,500 |

- |

|

Expenses |

|

|

|

Administrative expenses |

(231,000) |

(290,250) |

|

Depreciation |

(183,750) |

(426,000) |

|

Consulting fee expense |

- |

(198,750) |

|

Other expenses |

(758,250) |

(577,500) |

|

Profit before tax |

1,541,250 |

1,072,500 |

|

Tax expense |

(461,250) |

(316,500) |

|

Profit for the year |

1,080,000 |

756,000 |

|

Retained earnings - 1 July 2020 |

1,852,500 2,932,500 |

1,794,000 2,550,000 |

|

Dividends paid |

(487,500) |

(697,500) |

|

Retained earnings - 30 June 2021 |

2,445,000 |

1,852,500 |

Question 8

Refer to the scenario information in Section D and answer the following question :

Calculate the amount of goodwill recognised on consolidation at the date of acquisition. Please show all your workings. (3 marks)

Question 9

Refer to the scenario information in Section D and answer the following question :

Provide the appropriate journal entries to Luke Ltd to eliminate the cost of the investment in Jack Ltd and recognise goodwill as at 30 June 2021. (4 marks)

Question 10

Provide the appropriate journal entries required by the transactions/events listed as 1-6 below for the consolidated accounts for the year ended 30 June 2021, before considering any NCI (Note: You should consider the effect of tax in your answers). Provide journal narrations and show your workings.

Transactions:

1. During the year, Luke Ltd made total sales to Jack Ltd of $487,500, while Jack Ltd sold $390,000 in inventory to Luke Ltd.

2. The opening inventory in Luke Ltd as at 1 July 2020 included inventory acquired from Jack Ltd of $315,000 that had cost Jack Ltd $262,500 to produce.

3. The closing inventory of Jack Ltd includes inventory acquired from Luke Ltd at a cost of $90,000. This had cost Luke Ltd $72,000 to produce.

4. The closing inventory in Luke Ltd includes inventory acquired from Jack Ltd at a cost of $252,000. This had cost Jack Ltd $210,000 to produce.

5. On 1 July 2020 Luke Ltd sold an item of plant to Jack Ltd for $870,000 when its carrying value in Luke Ltd’saccounts was $607,500 (cost of $1,012,500,accumulated depreciation of $406,500). This plant is assessed as having a remaining useful life of six years.

6. Jack Ltd paid $198,750 of consulting fees to Luke Ltd in the current reporting period.

7. Jack Ltd paid a dividend of $697,500.

Assume a tax rate of 30 percent throughout this question (13 marks) [TOTAL = 20 MARKS]

SECTION E: FINANCIAL ANALYSIS AND BEYOND/ACCOUNTING THEORIES

Scenario Information

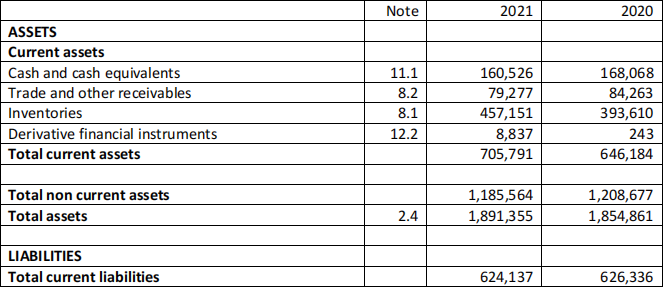

i. These are selected extracts from the Financial Statements of The Warehouse Group:

Consolidated Balance Sheet

As at 1 August 2021

ii. The Warehouse Group’s Annual Report for 2021 contains over 100 pages of information including the following three items:

a. Financial Statements

b. An Integrated Report

c. Global Reporting Initiative (GRI) Disclosures

Question 11

Refer to the scenario information in Section E (i) and answer the following question:

Discuss the liquidity of The Warehouse Group, using appropriate ratios, as well as horizontal and vertical analysis to support your comments. (5 marks)

Question 12

Refer to the scenario information in Section E (ii) and answer the following questions:

a. State the name of the umbrella term used by the XRB to describe reporting forms like integrated Reports and GRI disclosures. (1 mark)

b. Identify one further such form of reporting which is expected to become mandatory for around 200 large financial institutions in NZ entities from 2023. (1 mark)

c. Identify any two of the six ‘capitals’ within Integrated Reports. (1 mark)

d. Briefly describe the ‘ethical branch’ of Stakeholder Theory and relate this to a major difference between approaches taken in Integrated Reporting as opposed to GRI standards. (2 marks)

[TOTAL = 10 MARKS]

SECTION F: SEGMENT REPORTING AND RELATED PARTY DISCLOSURE

Scenario Information - Segment Reporting

The following divisional information is presented for Clyde Limited. This information is regularly reviewed by the Board of directors of Clyde Limited.

|

Division |

Revenue ($000) |

Profit/ (Loss) ($000) |

Division Assets ($000) |

|

Insurance |

300 |

130 |

900 |

|

Banking |

150 |

30 |

300 |

|

Agriculture |

60 |

20 |

120 |

|

Telecom |

45 |

(15) |

80 |

|

Total |

555 |

165 |

1400 |

Question 13

Refer to the scenario information for segment reporting in Section F and answer the following question:

Which divisions must be reported separately as segments in accordance with NZ IFRS 8? Please explain. (6 marks)

Related Party Disclosure

Question 14

Which of the following situations/transactions constitute a related party of an entity within the scope of IAS 24? Give reasons for your answer.

a. A person who has the authority to plan, direct and control the activities of the entity

b. The personal partner and children of a director of the entity.

c. A subsidiary company that is directly controlled by the entity.

d. Dividend payment to employees who are holders of an entity’sshares. (4 marks) [TOTAL = 10 MARKS]