关键词 > MTH322

MTH322 Assignment Two-2024

发布时间:2024-05-20

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Introduction

This part of the course assessment is worth 15% of the final mark for the course, and consists of a take-home course assignment that will be worked on and submitted properly.

This project aims to practice your skills in analytical pricing, and conduct an empirical study on option pricing with market data.

SCENARIO:

Suppose you are working on a security market consisting of a stock index (e.g., S&P500), a Treasury bond and a set of European (call/put) options:

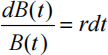

1) a Treasury bond delivers the annual yield of r with continuous compounding, and has the constant maturity (e.g., with the fixed Tbond). Under a risk-neutral probability measure Q, the

bond price follows a process as follows:

And the current bond price is $1.0, e.g., B(0) =1.0.

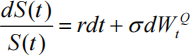

2) the price of the stock index follows a geometric Brownian motion. Under a risk-neutral

probability measure Q, the process for the stock price is given by:

3) There are a set of European call/put options on this stock index with the specific time-to- maturity (τ=T-t where t stands for the “current” time of valuation and T presents the maturity of the option) are specified with the strike prices as follows:

Requirements:

I. PART I (Theoretical Analysis) (50%)

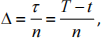

Consider a binomial option model defined by the triple of (u, d, q) under the risk-neutral measure, where the parameters u and d present the jump-up/down size of stock price, and q indicates the jump-up (risk-neutral) probability of stock over the time interval of Δ .

a) Work out the values of u, d and q so that the stock price S produces the first two moments over the time interval of Δ in this model:

Suppose that r and σ are constants.

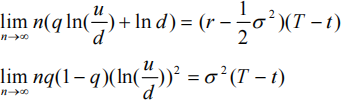

b) Now consider an n-period binomial model with  prove the following results:

prove the following results:

c) Let φ(n, k, q) present the risk neutral probability that the number of upward moves in the asset price is greater than or equal to kin the n-period binomial model, where q is given

above. With  prove the following results:

prove the following results:

where

so that

II. PART II (Valuation Exercise) (40%)

By specifying a date (e.g., 20240425), you can collect the following data samples:

. 10 standard options on the S&P500 index (SPX) with the different strikes as follows

and all options have the same time-to-maturity

. the close price of S&P500 index

. the close price of the government bond with the 3-month constant maturity

(Note that the information about all data sources is listed in Appendix.)

You are asked to complete the following tasks:

d) Establish a binomial model with N steps (N ≤ 10) to price a European call/put option

e) Given a specification of the European option, search for the optimal implied volatility (σ) that can generate the Black-Scholes price close to the market one with the minimal pricing errors

f) Given all 10 estimated implied volatilities from the collected options, draw a plot of the implied volatility in Y axis against strikes in X axis

III. PART III (Reporting) (10%)

Summarize all the results in Part I and Part II and make short comments on your ALL results in a report with the maximum of THREE pages, and other supportive results can be listed in Appendix

(without the limit on page number).

Assignment Guideline

This assignment assesses Learning Outcome A-E.

Note that you need:

1) Show all the results with comprehensive interpretations in a report (see the requirement in Part III);

2) Show other relevant and supportive results in Excel or other program language code (if applied).

As the outcome from this project, you are expected to submit a report, associated with the Excel files. Please disclose the detailed process/results in the report and appendices. The deadline of the assignment submission to LMO is at 5pm on May 26, 2023.

Your report must include:

1) A brief description of the project

In the first section, your work should contain a formal introductory section that provides an overview of the project, including the title of the project, the setup of the securities market and the process of asset prices and the main goals that this project aims to achieve.

2) Process of the optimal hedging strategies and performance analysis

After specifying the security market that you are working on, you are ready to complete the tasks in I) and II) which can be presented in two separate sub-sections. It is suggested that you describe the process of analytical thinking process in detail and report the performance analysis of your empirical study with market data, and then provide the details about the implementation of option pricing in the binomial-tree model and the Black-Scholes model. Also, please clearly explain how you obtain the required results, supported by your models in Excel files.

Note: the lecture and tutorial in Week 9&10 will demonstrate the strategy how to complete these tasks in a simplified case.

3) Comments on results

In the final section, you need briefly comment your analytical results in Part I, and explain your observations from empirical exercise with market data in Part II. It is very important for you to understand those theoretical results discussed in the lectures by conducting practical investigations in a specified market, which will help to improve your skills in financial modelling and investment management in practice.