关键词 > ECMT6002/6702

ECMT 6002/6702: Econometric Applications Week5 Tutorial

发布时间:2023-09-03

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECMT 6002/6702: Econometric Applications

1 Practice problems

1. Consider the following linear regression model:

Consider the following hypotheses:

The Wald statistic for the above hypothesis is defined as

where

(i) What is the limiting distribution of the above statistic if H0 is true?

(Optional) We know under standard assumptions,

Can you obtain the limiting distribution of the Wald statistic based on the above result?

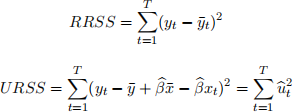

(ii) Show that RRSS and URSS are given as follows:

Note: The restricted/unrestricted models are given as follows:

(iii) Show that T (RRSS − URSS)/URSS is equivalent to (1.2).

(iv) Suppose that RRSS = 1105, URSS = 900, T = 100. We want to implement the Wald test with 5% significance level. Let A be the Wald statistic, B be the critical value and C be defined by

Find the value of A + B + C.

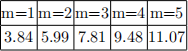

(Note) 95% quantile of χ2 (m)

(v) Suppose that RRSS = 1200, URSS = 900, T = 100. We want to implement the LM test with 5% significance level. Let A be the LM statistic, B be the relevant critical value and C be defined by

Find the value of A + B + C.

(vi) Write down the auxiliary regression for the White’s heteroskedasticity test. Assuming that R2 from the auxiliary regression is given by 0.3, compute the test statistic (A) and find relevant critical value (B), and then find the value of A + B. (Note : White’s test is already based on the asymptotic properties of the OLS estimators. So you can do this as in the Week 3 lecture note. I would recommend you to check how many variables will be included in the auxiliarly regression for the White’s heteroskedasticity test in a more general case where k regressors.)

2 Empirical application

We will consider the housing pricing example given in Wooldridge’s textbook. Suppose that we have the following regression model:

Instructions:

1. Compute the OLS estimates.

2. Examine H0 : β2 = 0.1, β3 = 0.01 using the Wald, LR, LM tests (with 5% significance level).

- Construct the restricted/unrestricted models and compute URSS and RRSS, and the compute the statistics. They must be close to

Wald = 159.87, LR = 91.13, LM = 56.75. (2.1)

- To compute the critical value, you can use qchisq(0.95,2) in R.

3. Examine H0 : β2 + β3 = 0.1 using the Wald, LR, LM tests (with 5% significance level).

- Note that the restricted model can be written as

y t − 0.1x3t = β1 + β2 (x2t − x3t) + β4x4t + ut. (2.2)

- The results must be close to

Wald = 3.7299, LR = 3.6530, LM = 3.5782. (2.3)

- To compute the critical value, you can use qchisq(0.95,1) in R.

4. This computing exercise is not mandatory.