FIN 430 Practice Midterm 2019

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FIN 430 Practice Midterm

Department of Finance and Statistical Analysis

2019

1. Valuation and Cost of Capital

ACME Corp., a maker of components for consumer electronics products, went public relatively recently. Its capital structure consists of publicly traded bonds and shares as explained below. ACME has 1 million 4.5% annual coupon bonds outstanding, with a face value of $1,000 each. ACME’s bonds have yield-to-maturity of 3.6% (EAR) and their price today is $1,050. ACME has 100 million shares of stock outstanding and the current stock price is $21. The beta of ACME common stock is unknown, due to lack of data (only a few months of trading since their recent IPO). The expected market risk premium is 4% and the interest rate on safe government securities equals 3%. The effective marginal corporate tax rate is 25%.

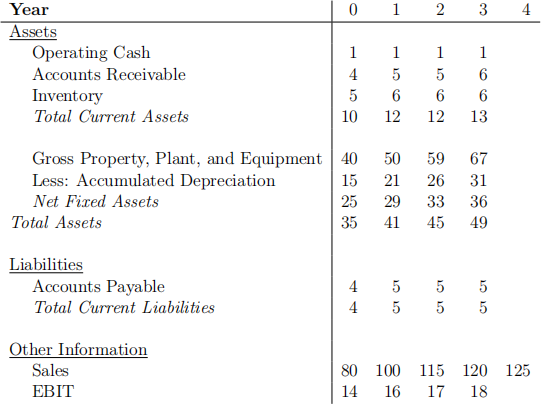

ACME management is pondering the acquisition of a rival firm; privately held Coyote Inc. ACME does not expect the acquisition to change its capital structure (the acqui- sition will be financed with the same proportion of equity and debt as the ACME’s existing operations). A group of consumer electronics component makers (companies that are all very similar to ACME) have an average (levered) equity beta of 1.25. These comparable firms have an average cost of debt of 4% and a debt-to-equity ratio of one (D/EComparables = 1). The table on the following page is part of a forecast of Coyote’s expected revenues and profits and other financial information (all amounts in the table are in $million). In all your calculations assume that companies have a target capital structure (firms strive to maintain a constant D/E ratio rather than a constant amount of debt).

(a) Calculate the discount rate that ACME’s should use to evaluate the Coyote acqui- sition.

(b) Estimate Coyote Corp’s free cash flows for years t = 1, 2 and 3 using the information below. Increases in gross PPE reflect capital expenditures (CAPEX). Similarly, increases in accumulated depreciation can be used to estimate annual depreciation amounts. All amounts (except years) above are in millions of dollars.

(c) Estimate Coyote Corp’s terminal value based on its expected sales at t = 4. Use the following additional assumptions:

![]() Operating Margin in year 4: EBIT/Sales = 0.16

Operating Margin in year 4: EBIT/Sales = 0.16

![]() Return on investment after year 4 and in all subsequent years: ROI = 8%

Return on investment after year 4 and in all subsequent years: ROI = 8%

![]() Reinvestment Rate at t = 4 and all subsequent years: Reinv. Rate = 30%

Reinvestment Rate at t = 4 and all subsequent years: Reinv. Rate = 30%

(d) What is your estimate of the value of Coyote Corp based on your results in b) and

c) above?

2. Capital Structure

Reliable Car Parts Industries (RCPI) has 5 million shares outstanding with a market price of $50.40 per share and no debt. RCP Industries has had consistently stable earnings and cash flows and pays taxes at a 40% corporate tax rate. Although investors expect RCPI to remain all-equity financed, management announces that the company will borrow $120 million on a permanent basis (after borrowing the $120 million, the amount of RCPI’s debt is not expected to change). RCPI will use the borrowed funds to repurchase some of their outstanding shares. Management’s expectation is that levering up will boost RCP Industries’ share price.

Note: Use Modigliani and Miller’s theory of capital structure with corporate taxes and permanent debt when answering questions a), b), and c) below.

(a) What is RCP Industries’ firm value before the announcement?

(b) What is RCP Industries’ firm value and share price immediately after the announce- ment (before the debt is issued)? (Think about the implications of the Efficient Market Hypothesis.)

(c) How many shares will RCP Industries repurchase? How many will remain out- standing and what is the market value of RCP Industries’ equity (the value of all RCP Industries shares combined) after the share repurchase is completed?

(d) Besides corporate taxes, what other factors will influence RCPI’s firm value as a result of the increase in leverage? Use the trade-off theory of capital structure to examine the impact of the change in RCPI’s capital structure. (No calculations are required.)

3. Going Public

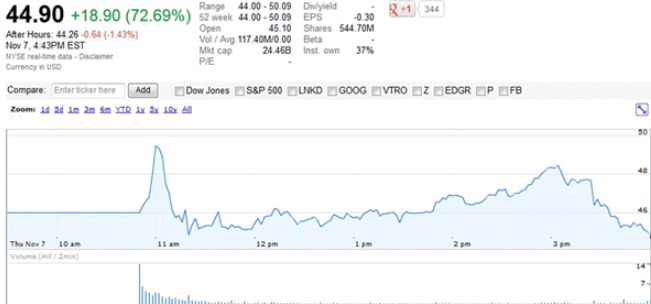

The image below was captured less than an hour after the close of trading in New York on the day of Twitter Inc.’s IPO. Have a careful look at the image and then answer the questions below.

(a) What happened to Twitter’s stock price on the day of the IPO? (In other words, compare Twitter’s closing market price to the offering price.) Briefly discuss three theories that explain such changes in price on the first day of trading.

(b) Describe how the syndicate of investment banks will i) protect Twitter’s price from dropping in the aftermarket following the IPO, and ii) hedge any risk the syndicate may face as a result of supporting Twitter’s price. What are the costs to Twitter (if any) of the price support provided by its investment banks? Do you think the Green Shoe (aka overallotment) option was exercised in Twitter’s case? Why or why not?

(c) Discuss IPO stocks from the perspective of typical retail investors trying to receive an allocation of newly issued shares at the offering price.

2022-02-12

Department of Finance and Statistical Analysis