International Banking and Financial Markets Assignment 1 – Spring 2022

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

International Banking and Financial Markets

Assignment 1 – Spring 2022

Instruction

— Please answer all questions. This is an individual assessment – submission to be made elec-

tronically via the course Moodle page. This includes a written report including analytical steps taken, numerical answers, diagrams, tables and comments. Clearly number each ques- tion and sub-question. Each part carries a weight described below:

— You can use a calculator or a software to carry out computations but intermediate steps

building up to the final answers should be included.

— Creating clear and effective diagrams and tables is an important feature to convey information

as a part of any written report. These must be self-explanatory with descriptions, variable units and axes’ labels.

Question 1 Assume a property investment with horizon of five years, a fixed market interest rate of 5% and a 40% increase in terminal value of the flat over the initial purchase price of ↔1,879,815.

Rent is assumed to be constant at ↔57,180 per year.

(1.1) What is the NPV of this property investment?

(1.2) What percentage would the IRR be for this property investment?

Include the steps taken and the final answers rounded up to 2 decimal points.

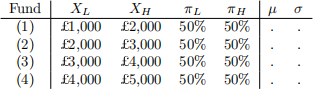

Question 2 Consider a financial investment company offering four funds described in the table below, where each fund either performs well and delivers a high payoff XH or performs poorly and delivers a low payoff XL , with probabilities πH and πL = 1 - πH , respectively. A risk-averse investor whose preferences over payoffs are summarised by a square-root form U := │X assesses funds (1)-(4):

Illustrate your results in a table arranged as above.(2.1) Compute the expected value (u) and the standard deviation (m) associated with each fund.

(2.2) Determine the price of risk for funds (1), (2), (3), and (4) from the perspective of the

investor who asks for compensation in return for committing to risk when assessing the funds. Illustrate the price of risk associated with the four funds in a diagram, where the horizontal axis shows the funds in order from (1) to (4), and the vertical axis shows the price of risk. What pattern do you observe (e.g. U-shape, inverted U-shape, decreasing, increasing, flat)?

(2.3) Explain the reason why this pattern arises.

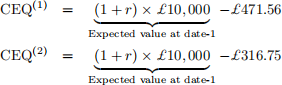

Question 3 An investment company has complied information about a specific investment port- folio (e.g. Fund A) that delivers on an annual basis (date-0 to date-1) either a 8% net return with probability 98.5%, or alternatively the fund defaults with probability 1 g5% leading to loss of the investment. Thus the investment company is expected to generate a net return equal to r on an initial investment value. Two risk-averse investors (1) and (2) indicate that, given the risk profile described, they are willing to pay the following self-declared amounts:

where CEQ(1) and CEQ(2) are the certainty equivalents for investors (1) and (2), respectively, and 戈471g56 and 戈316g75 are observed prices for risk asked by risk-averse investors (1) and (2). (3.1) What is the expected net annual return (r) of investment in Fund A? What is the standard

deviation of this return?

(3.2) The investment company lacks knowledge of the investors’ preferences and intends to de-

termine their risk-aversion attitudes based on a general power characterisation given by U := (X1 −γ )/(1 - 礻). Given the observed prices for risk, find each investor’s risk-aversion parameter 礻 (consider that the investors weigh payoffs equally over time i.e. no time dis- counting).

Question 4 (Empirical Work) On the course Moodle page, you can find descriptions of ac- cessing the following data from WRDS from January 2000 to the most recent observation available on the platform:

— Market index returns data on a value-weighted market portfolio including dividends rein- vested (variables vwretd) and excluding dividends (variable: vwretx)1. This is based on the US Total Market Index produced by the CRSP that comprises nearly 4,000 constituents across mega, large, small and micro capitalizations, representing nearly 100% of the U.S. investable equity market.

Further variables descriptions are provided by the CRSP2.

(4.1) Explain how to construct the dividend-yield from the variables provided.

(4.2) Implement a routine in Excel or an alternative software to construct the dividend-yield from

the series on monthly and quarterly frequencies. Plot both constructed series over time.

(4.3) What is the average value of dividend-yield during {2000-01 to 2009-12}, and during 2018,

2019 and 2020? Summarise the average values in a table.

2022-02-10