ACCY 231 FINANCIAL ACCOUNTING 2019

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

EXAMINATIONS – 2019

TRIMESTER 2

ACCY 231

FINANCIAL ACCOUNTING

QUESTION ONE: PROPERTY, PLANT AND EQUIPMENT

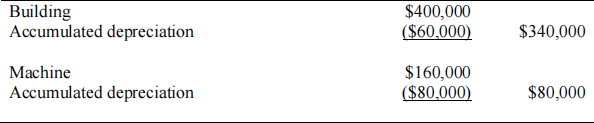

On 30 June 2019, the draft Balance Sheet of Hopeful Ltd. included the following non-current assets after charging depreciation:

Hopeful Ltd. has adopted the fair value method for the valuation of non-current assets. This has resulted in the recognition in previous periods of an asset revaluation surplus for the building of $15,000.

On 30 June 2019, an independent valuer assessed the fair value of the building to be $320,000. Assume that after the revaluation on 30 June 2019, the building had a remaining useful life of40 years with zero residual value.

The machine was purchased on 1 July 2017 and has a useful life of4 years with no residual value. Its fair value equals its carrying value. On 1 October 2019, it was sold for $64,750.

Hopeful Ltd. uses straight line depreciation.

Required:

(a) Prepare the necessaryjournal entries to record the effect of the revaluation of the building

as at 30 June 2019.

(b) Prepare the necessaryjournal entries to record the sale ofthe machine on 1 October 2019.

(12 marks)

[TOTAL OF 20 MARKS]

QUESTION TWO: STATEMENT OF CASH FLOWS

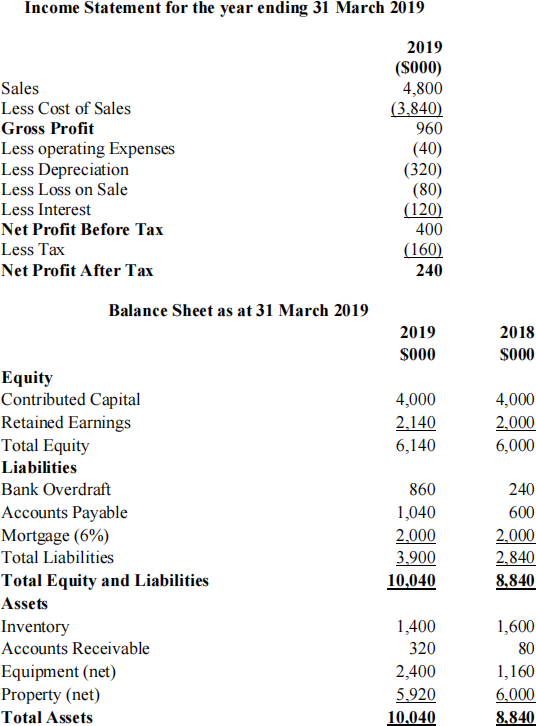

The abbreviated 2019 and 2018 comparative financial statements for Jonty Ltd. are presented below.

The following additional information was provided by the company:

• At the beginning of the year ending 31 March 2019, half of the equipment held at 31 March 2018 was sold at a loss of $80 thousand. New equipment was purchased at the same time for $2,060 thousand. There were no purchases or sales of property (depreciation relating to property was $80 thousand).

• All interest was paid. No interest was received.

• All sales were made on credit.

• Accounts payable relates to purchases of inventory.

• Dividends were paid in cash.

Required:

From the above abbreviated financial statements of Jonty Ltd. and the additional information provided by the company, prepare the Statement of Cash Flows for the year ended 31 March 2019. Presentation should be in accordance with NZ IAS 7. For the purposes of this question, ignore GST effects. You are NOT REQUIRED to provide notes to the Statement ofCash Flows including the reconciliation of net profit as shown in the Income Statement with net cash flows from operating activities as shown in the Statement of Cash Flows.

(20 Marks)

[TOTAL OF 20 MARKS]

QUESTION THREE: EMPLOYEE BENEFITS

Amber Ltd. provides long service leave entitlement of 12 weeks of paid leave after 10 years of continuous employment. The provision for long service leave had a credit balance of $185,000 at 1 January 2019. During the year ended 31 December 2019, long service leave of $45,000 was paid. At the end of the year, the present value of the obligation for long service leave was $181,000.

Required:

Prepare all journal entries in relation to long service leave for the year ended 31 December 2019. (Show workings).

[10 MARKS]

QUESTION FOUR: ACCOUNTING FOR INCOME TAXES

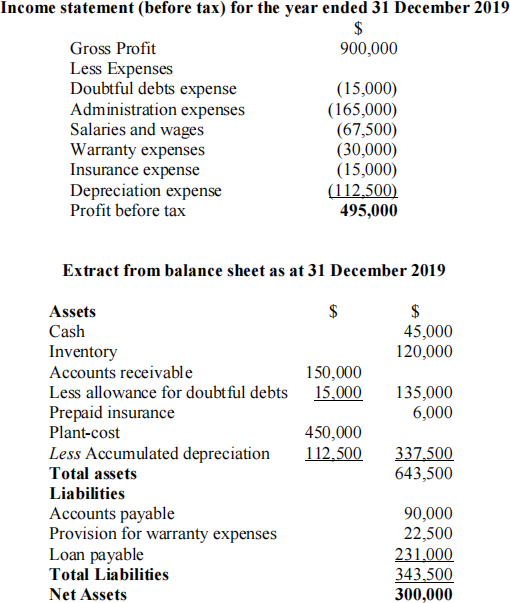

Kayla Ltd. commenced operations on 1 January 2019 and is preparing its first annual financial statements at the end of its financial year, 31 December 2019. Its draft financial statements have been prepared before considering taxation. Extracts from its Income Statement and Balance Sheet are shown below.

Additional information:

• All amounts received from sales, including those on credit terms, have been taxed at the time each sale is made.

• Insurance was initially prepaid to the amount of$21,000. As at year end, $6,000 remained to be expensed.

• The plant is depreciated straight line for both accounting and tax purposes; over 4 years for accounting purposes, but three years for taxation. The plant will have no residual value at the end of its useful life.

• All administration, salaries and wages expenses have been paid as at year end.

• Warranty expenses were accrued during the year. Warranty payments for the year equalled $7,500.

• After these differences between accounting and tax rules have been examined, the taxable incomefor theyear ending 31 December 2019 has been determined to be $489,000.

• Assume a tax rate of 30%.

Required:

(a) Prepare the journal entry to recognise current tax as at 30 June 2019 for Kayla Ltd. (Note: Do not prepare the current tax worksheet as the taxable income has been calculated for you.)

(4 Marks)

(b) Complete the deferred tax worksheet for Kayla Ltd. as at 30 June 2019 on the separate Yellow Answer Sheet. (Only include relevant assets and liabilities in your worksheet.)

(20 Marks)

(c) Record the journal entry for Kayla Ltd. to recognise deferred tax as at 30 June 2019.

(6 Marks)

[TOTAL OF 30 MARKS]

QUESTION FIVE: PROVISIONS, CONTINGENT LIABILITIES AND ASSETS

(a) Briefly explain the key differences between provisions and contingent liabilities.

(5 Marks)

(b) Provisions are recognised as a liability in the statement of financial position whereas

contingent liabilities are not recognised in the financial statements but disclosed, if material and not remote, in the notes to financial statements.

Required:

Briefly explain why provisions are recognised in financial statements but contingent liabilities are not recognised?

[TOTAL OF 10 MARKS]

QUESTION SIX: US GAAP VERSUS IFRS GAAP

US Financial Reporting Standards (US GAAP) have traditionally been viewed as rules based while International Financial Reporting Standards (IFRS GAAP) have been viewed as based on principles.

Required:

(a) With respect to the reporting requirements for Cash Flow Statements, Employee Benefits or Tax Effect accounting, describe a total oftwo differences between the requirements of US GAAP and IFRS GAAP that illustrate the rules versus principles distinction. The two differences may be drawn from any ofthe above three areas of financial reporting.

(b) Provide one possible reason for US GAAP being rule based, and one possible reason for IFRS GAAP being based on principles.

[TOTAL OF 10 MARKS]

2022-02-10