Math 361 Spring ’22

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Department of Mathematics

Math 361 Spring ’22

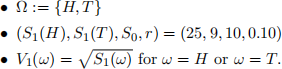

1. Consider a one-period economy with the following information:

Compute

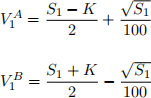

2. Assume a one period, trinomial state model for the evolution of a non- dividend paying stock. We know that the yearly rate for discounting is r = 0.25, today’s (time 0) stock value is S0, and that there there is a market for the following two financial derivatives VA and VB defined by the following payoff conditions at expiration time T = 1:

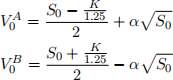

where K is a ”strike” chosen by the option purchaser. We will assume that a risk-neutral measure ![]() exists in this world. An analysis of past data shows that the market for financial derivatives A and B have their prices (for some α to be determined) as

exists in this world. An analysis of past data shows that the market for financial derivatives A and B have their prices (for some α to be determined) as

where K is again left to the buyer to determine.

(a) Is there enough data here to find the price F of a Forward contract on a unit of stock S1 at time T = 1? If so, what is F in terms of

the initial stock price S0 at time 0? (40 pts.)

(b) Does α depend on K? (10 pts.)

2022-01-29