ECN6520 Macroeconomic Analysis Autumn Semester 2020/21

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECN6520

DEPARTMENT OF ECONOMICS

Macroeconomic Analysis

Autumn Semester 2020/21

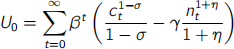

1 An infinitely-lived household’s lifetime utility can be expressed as follows:

where ci is consumption and ni are hours worked. σ and η are parameters deter- mining the curvature of the utility function. The parameter determining the dis- utility of labour is γ . The representative household produces goods, yi , using a Cobb-Douglas technology in hours worked and the capital stock:

The parameter α denotes the share of capital and lies between 0 and 1. Total factor productivity (TFP), ai evolves as follows: ln ai = ρ ln ai _ 1 + ei where ei is an iid shock with a zero mean. The capital stock, ki is pre-determined in period t and evolves as follows:

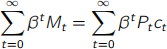

The firm belongs to the household, which chooses consumption, hours as well as next period’s capital stock.

(a) Set up the Lagrangian function and derive the first-order conditions for ci , ni and ki+1. (20 marks)

(b) Derive the so called Euler equation and show how the value of σ determines the volatility of consumption. (20 marks)

(c) Use the first-order conditions for ci and ni to analyse the effect of an exogenous increase in consumption (assume that household wealth has risen) on the supply of labour. (20 marks)

(d) In your own words, explain how TFP shocks (shocks to ai ) can lead to business cycles. (40 marks)

2 A firm, existing for two periods, produces output using capital and labour. The firm’s production at any time i can be described by a simple production function zb kb(a)n b(1)_a . The firm faces the following profit function expressed in real terms:

ab , sb and db denote the quantity and price of shares as well as dividend payments of shares held by the firm in period i in real terms. n and k denote labour input and capital stock, respectively. The firm has to borrow to invest in new capital stock. The amount it can borrow is constrained by the value of its stock holdings:

where R < 1 is a parameter that limits investment spending to a fraction of the firm’s stock holdings.

(a) Set up the constrained optimisation problem and derive the first-order con- ditions for n1 , n2 , k2 and a1 . (20 marks)

(b) Use the first-order conditions to derive the firm’s demand for capital sched- ule. (30 marks)

(c) Carefully explain the effects of an unexpected increase in R on the capital stock, the share price and on output. (50 marks)

3 A country’s consolidated government budget constraint in period t is defined as:

Where g is government spending, B denotes bonds held by the private sector, Pu is the price of bonds, T denotes taxation and M the money supply. The consumer price index is denoted by P .

(a) Use the consolidated government budget constraint to derive an intertem- poral government budget constraint. (20 marks)

(b) In your own words, explain why a non-Ricardian fiscal expansion will always end in inflation. (40 marks)

(c) In your own words, explain the mechanism behind the fiscal theory of the price level. (40 marks)

4 Assume an economy where households receive utility from consumption of goods and disutility from hours worked. Households maximise expected utility:

where the parameter ω > 1 . Households maximise expected utility subject to an infinite sequence of flow budget constraints:

In addition, households face the following cash-in-advance constraint in every period:

Pi ci is nominal consumption, (1 + ii ) is the nominal interest rate on bonds bonds, Bi is the level of bond holdings, Si is the share price, ai the stock of shares purchased by the household in period t , Di is a dividend payment and Mi is the money stock held by agents at the end of period t . wi ni denotes the household’s labour income.

(a) Set up the intertemporal Lagrangian and derive the first-order conditions with respect to ci , ni , ai , Bi and Mi . (20 marks)

(b) Show how the presence of a cash-in-advance constraint distorts the consumption-labour decision. Explain why a nominal variable can affect the choice between two real variables. (40 marks)

(c) What happens to consumption and price of bonds if the cash-in-advance constraint becomes non-binding [when the multiplier on the CIA constraint becomes zero]. (40 marks)

2022-01-27