FINA 200 - Personal Finance

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FINA 200 - Personal Finance

Winter 2026

Case 1

(due Monday, March 9, 2026, before 11:59 p.m. ET)

Covering Chapters 1 – 7

PLEASE READ THESE INSTRUCTIONS CAREFULLY

· Write your name and student ID above.

· This is an individual assignment, to be completed by you alone.

· There are 10 pages to this Case 1 including the cover page – please ensure that you have all 10 pages.

· The case consists of two sections. Answer:

Section I: respond directly on the Case. You MUST highlight AND underline your response to the multiple-choice questions.

Section II: respond directly on the Case in the space provided for each Mini-Case question. You MUST highlight AND underline where requested.

· You may submit your solution in English or French; acceptable submission formats include Word (.docx or.doc) or PDF. EXCEL is NOT accepted.

· Ensure that all responses with calculations are to two decimal places.

· Tables can be found at the end of the Case to help respond to some of the questions.

· Outside research will be required (research does not require citations).

· Show your work (some questions award partial marks).

This Case is 15% of your grade.

For marking purposes only:

|

Multiple Choice |

Mini-Case A |

Mini-Case B |

Mini-Case C |

Mini-Case D |

Mini-Case E |

Total |

|

/2.5 |

/3.25 |

/2 |

/3.5 |

/3.25 |

/.5 |

/15 |

Section I: Five (5) Multiple-Choice Questions (2.5 marks - .5 marks each)

Highlight AND underline your response.

1) After earning his degree from Concordia University in December, Andrew began working full-time at Shopify in January 2026. He was invited to participate in the company’s Group Registered Retirement Savings Plan (RRSP) which would have allowed him to contribute $350 per month, for which Shopify would have matched dollar for dollar. Feeling that retirement was too far in the future, Andrew declined to enroll.

Assume instead that Andrew had enrolled at age 22, contributing $350 per month with an equal employer match, for a total contribution of $700 at the end of each month. If the funds earned an average annual return of 8%, compounded semi-monthly, how much would be accumulated in Andrew’s RRSP by the time he turned 65?

a) $3,839,331

b) $3,132,460

c) $3,145,708

d) $2,992,110

e) $3,006,725

2) On February 26, 2026, Wei, a resident of Quebec, turned 19. To celebrate, he received a substantial amount of money as a birthday gift and is now considering putting it into a Tax-Free Savings Account (TFSA). Although he’s not entirely sure how TFSAs work, he’s heard of others earning good returns through them. Wei would like to know the maximum he’s allowed to contribute to his TFSA and how much can be deducted on his 2025 personal income tax returns. (Refer to Table C)

a) He can make a $14,000 contribution and can claim a $7,000 deduction on his 2025 personal income tax returns (and carryforward $7,000 to claim on his future 2026 tax returns).

b) He can make a $14,000 contribution but cannot claim a deduction on his personal income tax returns.

c) He can make a $7,000 contribution and can claim a deduction of $7,000 on his 2025 personal income tax returns (he must wait until the end of 2026 to determine how much he can deduct on his 2026 returns).

d) He can make a $14,000 contribution and can claim a deduction of $14,000 on his 2025 personal income tax returns ($0 on his 2026 returns).

e) He can make a $7,000 contribution but cannot claim a deduction on his personal income tax returns.

3) Scott is struggling with his debts and is looking at a Consumer Proposal. Which of the following statements is true?

a) Scott’s filing a Consumer Proposal will result in automatic bankruptcy.

b) Scott must sell his assets before he can file a Consumer Proposal.

c) Scott’s filing a Consumer Proposal guarantees he will repay his debt in full.

d) Scott’s filing a Consumer Proposal immediately removes all negative information from his credit report.

e) None of the responses.

4) It is March 1, 2026, and Eric has officially reached 18 years of age. He began part-time employment when he was 16 and is now planning to contribute to a Registered Retirement Savings Plan (RRSP) for the first time. With a visit to the bank scheduled for tomorrow, he would like your help determining the maximum RRSP contribution he can deduct on his 2025 income tax return.

(Refer to Table E)

Eric’s gross yearly earnings:

2024 (16 years old): $4,000

2025 (17 years old): $5,000

2026 (18 years old): $10,000 (earned to date)

a) $720

b) $900

c) $1,625

d) $2,700

e) $3,420

5) Back in 2023, Priya invested $8,000 to buy 1,600 shares of a Canadian tech company called BrightSpark Innovations Inc. and held them in a non-registered account. On December 18, 2025, she sold 800 shares when the price reached $8 per share, and put the proceeds from the sale of the shares into a newly opened Tax-Free Savings Account (TFSA). She was aware that this sale would trigger a capital gain she’d have to report on her 2025 tax return. However, she also sold some mutual funds in December 2025, taking a $200 capital loss on that sale. Since Priya lives in Quebec and falls into the highest marginal tax bracket, how much tax will she owe from these investment transactions for 2025? (Refer to Table A). Two decimal places.

a) $1,100

b) $2,200

c) $1,086

d) $480

e) $586

Section I completed, continue to Section II.

Section II: Five (5) Mini-Cases (12.5 marks)

Write your response in the template or space provided.

Mini-Case A: (3.25 marks)

Jiaqi is looking to better understand Registered Retirement Savings Plans (RRSPs) and Tax-Free Savings Accounts (TFSAs).

a) Indicate whether the statement is True or False. (3 marks for .25 marks each)

|

Indicate whether the statement is True or False.

|

RRSP (True or False)

|

TFSA (True or False) |

|

Tax-free withdrawals. |

|

|

|

Tax-deductible contributions. |

|

|

|

All Canadians who are eligible to contribute are subject to the same annual contribution limit. |

|

|

|

You can withdraw money under the Home Buyers' Plan (HBP), (to a certain limit) to help finance the purchase of your first home.

|

|

|

|

Contribution eligibility begins in the year an individual reaches the age of majority. |

|

|

|

Unused contribution room carries forward to future years if it is not fully used. |

|

|

b) The deadline for making a Registered Retirement Savings Plan (RRSP) contribution to count as a deduction in the 2025 income tax return is ___________________________. (.25 marks)

a) within the first 60 days of the following year (i.e., March 2, 2026, since the 60th day falls on a Sunday).

b) before the end of February, i.e. February 28, 2026.

c) in the first 31 days of the following year, i.e. January 31, 2026.

d) before the end of the year, i.e. December 31, 2025.

e) before the end of the year, i.e. December 31, 2026.

Mini-Case B: (2 marks)

We are March 1, 2026, Arjun, who is 60 years old, has been diligent about contributing to his Tax-Free Savings Account (TFSA). Since the TFSA program was introduced, he has made the maximum annual contribution at the very start of each calendar year in January, without ever making a withdrawal. (See Table C)

a) Given that Arjun has already made his full TFSA contribution for 2026, what is the total amount he has contributed to his TFSA to date since the plan’s inception? (.5 marks)

Response: (.5 marks)

b) As of March 1, 2026, the investments in Arjun’s TFSA have grown to a total market value of $286,432. Suppose he decides to withdraw the entire amount to fund a major home renovation project he’s been dreaming about. When would be the earliest date Arjun could contribute to his TFSA without incurring any penalties? (.5 marks)

Date: _______________

c) Based on the date in b), what is the maximum amount that Arjun could contribute to his TFSA without triggering penalties? (1 mark)

Response: (1 mark)

Mini-Case C: (3.5 marks)

You have been roommates with John and Joanne since last year and rent an apartment near Concordia. They have turned to you for some advice as you are taking a Personal Finance course. Despite you being great with finances, John insisted on taking care of paying the bills each month. You and Joanne both agreed to the arrangement, making it easier for both you and her to simply e-transfer a lump sum to John based on his monthly calculations. All of you are Canadian citizens, residing in Quebec. Information as of March 1, 2026:

Joanne (currently 23 years old with an upcoming birthday on May 2, 2026):

· is a full-time student at Concordia.

· lives on a tight budget but manages to set aside $25 from each paycheque from her part-time job for her Tax-Free Savings Account (TFSA) and, to date, has contributed $2,600.

· has never contributed to a Registered Retirement Savings Plan (RRSP).

· has been working part-time (12 hours/week) earning $20/hour at the Bank of Montreal:

§ 2023 gross annual salary for part-time work $12,000

§ 2024 gross annual salary for part-time work $13,000

§ 2025 gross annual salary for part-time work $14,000

§ 2026 gross annual salary for part-time work $15,000

John (currently 25 years old, birthday was on January 23, 2026):

· graduated in April 2025 with a degree in software engineering but attempted to earn income by playing video games professionally.

· has yet to earn income as a gamer despite claiming that he does.

· his parents provided him with a budget throughout his school years, except for tuition, which he covered through a government student loan. After telling his family he was earning significant income as a professional gamer, his parents stopped providing monthly financial support.

· has never contributed to a TFSA nor an RRSP.

a) Calculate the following to see how much each could contribute to a Tax-Free Savings Account (TFSA) as of today. Take contribution room from previous years into consideration; use information from Table C. (2 marks for 1 mark each)

|

Joanne’s total TFSA contributions |

(1 mark)

|

|

John’s total TFSA contributions |

(1 mark)

|

b) All three of your names are on the lease agreement. The internet bill is in your name, and the electricity bill is in Joanne’s name. John is responsible for making the monthly payments, which both you and Joanne appreciated, as taking care of the monthly finances was tedious. Each month, you and Joanne e-transfer the amounts John calculates. It has now come to light that John has not been paying the rent or the internet and electricity bills for some time, after delinquency notices were received from the landlord and service providers. Provide two potential financial impacts these non-payments could have on you.

(.5 marks for .25 marks each)

1) Impact:_____________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

2) Impact:_____________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

c) John admits that he used the money to buy lottery tickets and for online gambling. You explain that his actions have put both you and Joanne in a difficult financial position. John then tells you he has won $10,000 and promises to use it to catch up on the outstanding payments. He asks for your financial advice, specifically whether the money he has won is taxable. (Underline and highlight your response). (1 mark for.20 marks each)

1) Lottery ticket winnings are taxable: Yes or No (.20 marks)

2) Online gambling winnings are taxable: Yes or No (.20 marks)

3) Interest earned on investing the money from the lottery is taxable in a non-registered account: Yes or No (.20 marks)

4) Interest earned on investing the money from the lottery inside a TFSA is taxable: Yes or No (.20 marks)

5) Capital gains on investing in a non-registered account: Yes or No (.20 marks)

Mini-Case D: (3.25 marks)

Macy has a credit score of 690. She is looking to make an offer on a condo for $475,000 in two weeks on March 12, 2026. She cannot afford a conventional mortgage and has savings of 10% to use as a down payment. For Macy to get a mortgage, she requires mortgage loan insurance and needs to meet the following requirements under Canada Mortgage and Housing Corporation (CMHC) to qualify for mortgage loan insurance:

· The maximum amortization for insured mortgages is 25 years.

· The minimum down payment is 5% on a home valued at $500,000 and under.

There are several other requirements to be approved for a CMHC insured mortgage for which these requirements can change in response to economic downturns or other factors. Use the following current rates to be eligible for CMHC mortgage default insurance coverage:

· Have a Gross Debt Service ratio of less than 39%*

· Have a Total Debt Service ratio of less than 44%*

· Have a credit score of at least 680 (minimum credit score of 600 (at least one borrower))

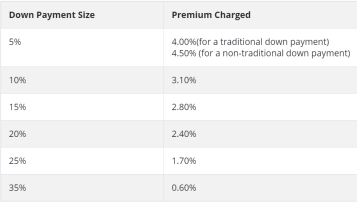

Default Mortgage Insurance rates:

a) Macy is going to the Royal Bank of Canada (RBC) to discuss her potential mortgage with them. RBC will be calculating Macy’s Total Debt Service (TDS) ratio. Macy’s gross annual income is $129,000. The property that she is looking to purchase would result in monthly heating costs of $475, condo fees of $1,900 per year, while her annual property taxes would be $4,750. Her only debt is a car loan of $875 per month.

Calculate her TDS ratio using a monthly mortgage payment of $2,500. (1 mark)

Calculation: (1 mark)

b) Calculate her GDS ratio using a monthly mortgage payment of $2,500. (1 mark)

Calculation: (1 mark)

c) Calculate Macy’s mortgage default insurance using the above table Default Mortgage Insurance rates? (1 mark)

Calculation: (1 mark)

d) What is default mortgage insurance? (.25 marks)

___________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Mini-Case E: (.5 marks)

Sarah went to the bank to enquire on a car loan in the amount of $25,000. CIBC has proposed a loan with the principal and interest due as a lump sum in 5 years. The interest rate on the loan from CIBC would be 7% compounded monthly. Sarah decided to go to her parents and ask for a simple interest loan for the same amount (i.e. $25,000 due in a lump sum in 5 years but with simple interest of 7%). Her parents of course refused as they would be losing out on interest. What is the difference in compounding interest over simple interest? (.5 marks)

Calculation: (1 mark)

2026-03-11