SESS0111: Basics of Financial Markets 25/26

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

SESS0111: Basics of Financial Markets 25/26

Individual coursework

Released: Monday 2nd March

Due: Friday, 23rd March 2026, 3pm UK time

Submission: Upload on Moodle

Word limit: 2000 words

This is an INDIVIDUAL assignment. The front page should be the complete Coversheet available on Moodle.

Answer ALL questions. Please provide detailed solutions and calculations, and, most importantly, explain your methodology, solution and choices in full detail. All explanations must be precise, accurate, well-argued and -phrased and demonstrate actual understanding of the subject and the methods, as opposed to copy-pasting material and mechanical applications. Provide examples, graphs and detailed answers where appropriate and present the workings and thought process in full detail. UCL guidance on plagiarism and the use of AI applies as described on Moodle. You MUST include the completed Coversheet, available on Moodle, as the first page of your submission. The word count of 2000 words is based on Chapter 10.11 of the SSEES Student Handbook and applies to net text only (does not include numbers, equations, tables and figures, captions and titles, references, abstract etc.). If you face problems in submission, please contact your Programme Administrator or [email protected].

Marking criteria - All questions and sub-questions carry the denoted marks. Arriving at a correct result without any explanation is worth minimal marks. Marks are awarded based on i) understanding the course material and question requirements ii) showing insight and creativity iii) correctness iv) proper use of terminology, accuracy and clarity in explanation and language v) proper presentation and notation. The criteria are in random order. Computer-formatted submissions are strongly encouraged. Plots and diagrams can be hand-drawn but must be properly placed within the text and properly labelled. Do not round up numbers during the calculations but only when reporting the final result. All questions can be answered based on course material but some require own research, decision making, judgement and appropriate framing and justification of the answer.

Any questions must be posted on the TFM 2 Teams group, not sent by email or personal message, to benefit as many students as possible.

Question 1 (30 points)

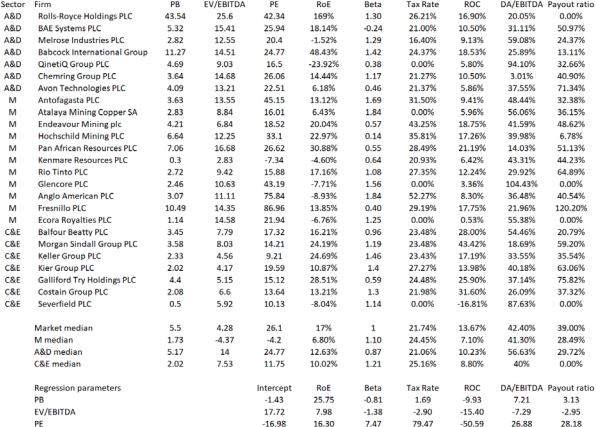

You are an asset manager that considers adding some stocks from three sectors in your portfolio. The three sectors are Mining, Aerospace and Defence (A&D) and Construction and Engineering. You intend to do relative valuation based on the Price-Earnings (PE) ratio, the Price-to-Book (PB) ratio and Enterprise Value over EBITDA (EV/EBITDA) with a margin of safety of 30% for each metric. Apart from the raw data in the table, you are also provided with regression parameter estimates, which you can select and use in models according to your judgement.

(1) Which of the firms below would you select, based on the data provided and the models you construct? (15 points)?

(2) Based on real-world information on those firms, would you trust your valuation above? Explain in detail using real-world information and cite your sources. (15 points)

Notes: The same parameters can be used for market and sector analysis. You can use the same parameter value for every model you construct, i.e. assume that a change in the model variables does not affect the parameter estimates. Do not try to improve on those simplifying assumptions.

Question 2 (10 points)

Assume a portfolio that holds $53mil in 10-year US Treasury bonds. What was the percentage and absolute (dollar) change in the value of the position between 4th and 11th April 2025 (use this source)? Then, compare and discuss the equivalent changes in 1-year, 5-year, 10-year and 30-year maturities using FRED data (see above source).

Question 3 (20 points)

You invested £50,000 in a homemade equally weighted fund-of-funds between 1st January 2022 and 31st December 2025, rebalanced at the end of each calendar year. The portfolio consists of two mutual funds, [1] and [2], with administrative fees (“max annual charge”) as stated, and two hedge funds, [3] and [4] (note: treat them as hedge funds), with administrative fees of 2% plus performance fees of 20% subject to a fixed hurdle rate of 7%. Every fund applies those fees at end-of-year, does not charge fees for withdrawing assets and charges the administrative fee on newly invested assets, with the charge applying on the date of transaction (including the start of the investment). The close prices at daily frequency and fees, where applicable, are in the hyperlinks above and you can consider the portfolio liquidated at the end. All rates are per annum.

What is the net value of assets under management at the end of the investment, the absolute (dollar) profits or losses, the annual and total percentage returns for the investor and total fees paid as a percentage of net assets under management at the end of the investment? Comment on the performance, structure and rationale of the investment strategy.

Question 4 (40 points)

Read the following resource (requires UCL VPN or library access). Identify and discuss the main arguments, findings, assumptions, rationale and underlying real-world conditions and information of the resource. Have the findings proven to be accurate, and are they still relevant today (i.e. how has the investment environment changed since then)? How have hedge funds changed since then and where do they stand today compared to other investment instruments in terms of popularity, performance, importance, cost and use of trading strategies? You can base your answer on academic and practitioner sources but make sure they are publicly accessible and correctly cited.

2026-03-10