BMAN30111 ADVANCED CORPORATE FINANCE 2021

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

BMAN30111

ADVANCED CORPORATE FINANCE

2021

![]()

Answer any TWO questions.

All questions carry EQUAL marks

QUESTION 1

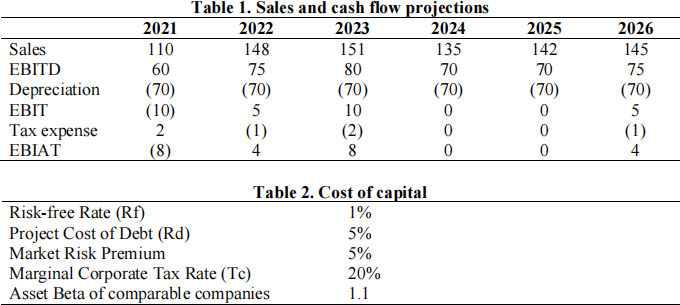

(a) A very successful and profitable firm is currently considering a new, large investment project that could be initiated at the start of 2021. The project involves the

acquisition of a plant, which requires an initial outlay of £420 million. Although it is not clear for how long the project will last, there is an expectation that over the first six years of the project its initial capital investment should be fully depreciated. The firm’s accountants have prepared the following projections on expected sales and cash flows, and information on the cost of capital of the company:

Required:

Carry out the following calculations, always assuming that cash flows occur at the end of their respective years:

(i) Estimate the NPV of the investment project at the start of 2021 if it is 100% financed with equity and assuming that the project is terminated at the end of

2026. Show and explain your calculations and comment on your findings.

(10 marks)

(ii) Use the WACC method to estimate the NPV of the investment at the start of 2021 assuming that it is financed 55% with equity and 45% with debt and that the project is terminated at the end of 2026. Show and explain your calculations and comment on your findings.

(10 marks)

(iii) Calculate again the NPVs of parts (i) and (ii) by assuming that the project is not terminated in 2026 and that, instead, it is expected to produce the same cash flow (i.e. with zero future growth in cash flows) as that for the year 2026 in perpetuity. Show and explain your calculations and comment on your findings.

(10 marks)

(b) What are the main assumptions underlying standard applications of the WACC method? Are these assumptions plausible, also in light of the existing empirical evidence?

In the alternative APV method, it is often assumed that the tax shields should be discounted using the cost of debt. Do you think this a reasonable assumption in real- world, practical applications?

[Word limit: 350 words]

(20 marks)

(c) Compare and contrast the assumptions and implications of the trade-off theory with those of the pecking order theory of capital structure . Briefly highlight evidence that supports the pecking order theory while being inconsistent with the trade-off theory.

[Word limit: 300 words]

(15 marks)

(d) Empirical tests of the (dynamic) trade-off theory are often based on estimations of

the following dynamic regression model:

![]()

![]() −

− ![]()

![]() −1 =

−1 = ![]() (

(![]()

![]() −

− ![]()

![]() −1) +

−1) + ![]()

![]()

Explain the logic behind this model and carefully describe each part of it (except uit), with a particular focus on λ and Levit*.

Let us assume that we have estimated the model above and found λ to be equal to 20%. What do we learn from this estimation? Is our finding consistent with the trade- off theory?

[Word limit: 350 words]

(20 marks)

(e) Your company has hired a financial consultant to better understand whether and how your company’s capital structure, which only includes equity, can be enhanced. The consultant is convinced that your company should significantly increase leverage to a very high level and borrow as much as possible. The consultant’s conviction is based just on two considerations:

- The effective tax advantage of debt (T*) is positive;

- Since T* is positive, the value of your company is positively related to the level of debt.

In your opinion, is the consultant’s analysis logically sound and comprehensive enough to provide reliable advice? If not, what is missing from the analysis? Provide some brief suggestions as to how the analysis could be improved.

[Word limit: 300 words]

(15 marks)

QUESTION 2

(a) At time t=-1, a publicly listed firm owns some assets in place and a positive NPV project in which the firm could invest at time t=0. However, both the firm’s managers and the outside investors do not know the precise values of the firm’s assets in place and of the NPV of the project. The firm has no financial slack and must issue equity to new shareholders to invest in the project at time t=0. All the assumptions of Myers and Majluf’s (1984) pecking order model hold. At time t=0, the firm’s management receive private information about the values of the firm’s assets-in-place and the NPV of the investment project. When deciding whether to issue equity and go ahead with the new project, the management act in the best interest of the passive, existing shareholders. The key financial information about the firm and its investment opportunity can be found in the table below.

|

Firm type |

High quality |

Low quality |

|

Probability of firm type |

0.35 |

0.65 |

|

Financial slack (in £ million) |

0 |

0 |

|

Assets in place (in £ million) |

320 |

110 |

|

Initial outlay of new project (in £ million) |

45 |

45 |

|

NPV of new project (in £ million) |

22 |

9 |

Required:

(i) Derive a rational expectations equilibrium (REE) in which investors’ rational beliefs at time t=0 are consistent with the management’s actions at time t=0. Show your calculations in detail and comment on your results.

(15 marks)

(ii) Compute the value of the firm at time t=-1. Compare this to the value of the firm at time t=-1 with symmetric information, i.e. assuming that the managers and the outside investors simultaneously observe firm type at time t=0. Explain the difference (if any).

(7 marks)

(iii) What would the equilibrium outcome of the model be if the firm’s financial slack was equal to 40 (S=40)? Show the steps in detail and discuss the potential value of financial slack in mitigating the underinvestment problem.

(8 marks)

(b) Describe the assumptions, implications and predictions of the pecking order theory. Explain why asymmetric information frictions can lead to underinvestment.

Based on the pecking order theory and its implications, what is the relationship between a firm’s financial slack and the likelihood that the firm underinvests? Also, is the probability of underinvestment in a particular project affected by the expected value of the project?

[Word limit: 300 words]

(15 marks)

(c) Academics argue that a firm’s effective tax advantage of debt T* should be considered by the firm’s managers to improve their financing choices. However, what are the practical challenges and complexities managers face to estimate T*? Describe the complex issues that practitioners may face when estimating T*.

[Word limit: 350 words]

(20 marks)

(d) Graham and Harvey (2001, “The theory and practice of corporate finance: evidence from the field”, Journal of Financial Economics) find that two of the most important factors that affect the decision to issue debt are “Financial flexibility” and “Interest tax savings”. As for the decision to issue equity, two relevant factors are “Magnitude of equity undervaluation/overvaluation” and “If recent stock price increase, selling price ‘high’” . Comment on whether these findings and the related content of the survey are consistent with the predictions of the pecking order theory.

[Word limit: 300 words]

(15 marks)

(e) Empirical papers often focus on the relationships between leverage and several variables. The following is a list of well-known determinants of capital structure:

- Firm size

- Asset tangibility

- Profitability

- Market-to-book (MTB) ratio

- Industry capital structure

For each of these variables, describe the sign (positive or negative) of the relationship that is typically observed with leverage. Also, explain whether such a relationship is expected based on the trade-off theory or on the pecking order theory.

[Word limit: 350 words]

(20 marks)

QUESTION 3

(a) Case study on WorldCom, “Restoring Trust at WorldCom”.

What are Mr. Breeden’s areas of reform that are most important for creating a sound governance structure within WorldCom? Use both theoretical arguments and empirical evidence to critically support your views.

[Word limit: 500 words]

(30 marks)

(b) Within the outsider system:

(i) explain in detail what “passivism of institutional investors” means and what the potential consequences are within a company. Use empirical evidence and readings to support your arguments. [Word limit: 400 words]

(25 marks)

(ii) Explain in detail the “regulatory mechanisms” as a way to

reduce potential agency costs between managers and shareholder. Using empirical evidence and readings, critically discuss the effectiveness of each different regulatory.

[Word limit: 350 words]

(20 marks)

(c) Within the insider system:

(i) explain all possible issues arising from a conflict of interest between large shareholders and minority shareholders. Describe in detail the problem of tunnelling and how the effects of tunnelling can be exacerbated by the presence of complex ownership structures, such as pyramids.

[Word limit: 200 words]

(10 marks)

(ii) In your opinion, are complex ownership structures widespread

across countries? Provide empirical evidence to support your answer.

[Word limit: 250 words]

(15 marks)

QUESTION 4

MagnusBane International Plc, a listed company operating in the entertainment sector, has a current market value (net of coupon payments on its debt in the current period) of £170 million. The firm’s market value has been projected to either increase by 50% or decrease by 30% in any one year.

The company is financed through equity and callable, convertible debt consisting of 1,500,000 debentures. Each debenture has a face value of £100, a coupon of 3%, and a remaining term to maturity of two years. Each debenture may be converted into 20 shares at any time up to and including maturity. The company has the right to call the debt at any time. If the debt is called, debtholders must choose to either convert their debt immediately or accept the call amount consisting of a fixed payment of £130 per debenture.

In addition to the callable, convertible debt, the company is also financed with a total of 5 million outstanding shares. So far, the company has never paid dividends, and it is not expected to do so within the next two years.

The annual risk-free rate of interest is predicted to remain constant at 3% per annum over the next two years.

Required:

(a) Using the binomial option-pricing model:

i. calculate the current value at t = 0 of MagnusBane International Plc’s straight debt;

(5 marks)

ii. calculate the convertible and callable convertible debt values. For your calculations assume that debtholders act as one (i.e. in unison). Explain each step you have taken to obtain your answers, and explain the actions of debtholders at each stage.

(10 marks)

(b) Suppose now the firm’s market value is estimated to increase by 100%

and decrease by 60% over the next two years. If everything else remains as in part (a), how would this affect your results in part (a)? Explain in detail your answer.

[Word limit: 200 words]

(20 marks)

(c)

(i) Suppose that MagnusBane International Plc is financed only through equity and straight debt. The company is exposed to conflicts of interest between shareholders, on one hand, and the outstanding debtholders, on the other hand. In your view, would an issue of convertible debt reduce such conflicts? Use theoretical arguments and empirical evidence to support your answer.

[Word limit: 200 words]

(15 marks)

(ii) Critically discuss other rational motives for companies to issue

convertible debt, by presenting also the empirical evidence. [Word limit: 400 words]

(20 marks)

(d) Critically discuss other debt-related mechanisms that might reduce the agency costs of debt. Are such mechanisms always effective? Use empirical evidence to critically support your discussion.

[Word limit: 500 words]

(30 marks)

2022-01-26