ECON6033—Corporate Finance 2021

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECON6033—Corporate Finance

Assignment 1

2021

1. Mr. Wong bought an apartment at a price of $7,000,000 on January 1, 2018. He borrowed 70% of the property value from Hang Seng Bank at that time. The ![]() rst monthly installment was due on January 31, 2018. The mortgage is a

rst monthly installment was due on January 31, 2018. The mortgage is a ![]() oating-rate one and has a maturity of 10 years. The interest rate on the loan is set equal to the prime rate minus 1.5%.

oating-rate one and has a maturity of 10 years. The interest rate on the loan is set equal to the prime rate minus 1.5%.

On March 1, 2020, Mr. Wong’s apartment had a market value of $9,000,000. Mr. Wong talked to Hang Seng Bank to arrange a new mortgage to replace the old one. In the new mortgage, Mr. Wong borrowed 70% of the market value of his apartment. The new mortgage has a maturity of 10 years with the ![]() rst monthly installment due on March 31, 2020. The interest rate is set equal to the prime rate minus 2.5%. The prime rate has been constant at 5% from January 2018 to March 2020.

rst monthly installment due on March 31, 2020. The interest rate is set equal to the prime rate minus 2.5%. The prime rate has been constant at 5% from January 2018 to March 2020.

(a) What is the monthly installment of the original mortgage?

(b) How much would Mr. Wong receive from Hang Seng Bank when the new mortgage was arranged to replace the old one on March 1, 2020?

(c) What is the monthly installment of the new mortgage?

2. Mr. Wong has just been ![]() red as CEO at the beginning of 2021. As consolation the board of directors give Mr. Wong a consulting contract that pays him $1,500,000 at the end of each year for 5 years.

red as CEO at the beginning of 2021. As consolation the board of directors give Mr. Wong a consulting contract that pays him $1,500,000 at the end of each year for 5 years.

(a) What is the duration of this contract if Mr. Wong’s personal discount rate is 9%?

(b) What is the change in the contract’s present value for a 0.5% increase in Mr. Wong’s discount rate?

(c) Use duration to calculate the change in the contract’s present value for a 0.5% increase in Mr. Wong’s discount rate? How is the answer di![]() erent from that in part (b)?

erent from that in part (b)?

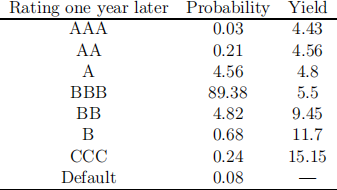

3. Consider a 6-year 5.5% coupon bond that is rated BBB when issued at par (i.e., $1,000) at the beginning of this year. Assume that the recovery rate is 46% of the face value in the case of default.

(a) Plot the probability distribution of the bond value one year later, where the ![]() rst-year coupon is included. What do you

rst-year coupon is included. What do you ![]() nd?

nd?

(b) What is the expected value of the bond one year later? What is the standard deviation of the bond value one year later?

(c) If you plan to hold this bond for one year, what is the VAR in dollar terms at the 99% con![]() dence level assuming that the bond value is normally distributed? What is the VAR in dollar terms at the 99% con

dence level assuming that the bond value is normally distributed? What is the VAR in dollar terms at the 99% con![]() dence level using the true distribution of the bond value? Are these two VARs the same?

dence level using the true distribution of the bond value? Are these two VARs the same?

2022-01-26