BMAN21020 FINANCIAL REPORTING AND ACCOUNTABILITY 2020

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

BMAN21020

FINANCIAL REPORTING AND ACCOUNTABILITY

2020

SECTION A (COMPULSORY)

Question 1: Consolidated Financial Statements

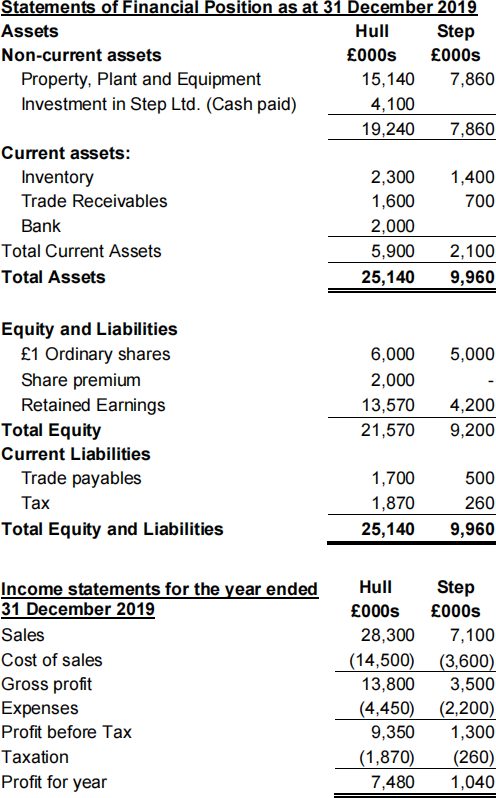

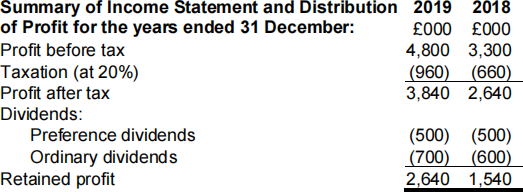

The summary financial statements of Hull plc and Step Ltd are:

Additional Information:

1. On 1 April 2019, Hull acquired 70% of the ordinary shares of Step when the retained earnings of Step stood at £3.42m. Consideration comprised cash of £4.1m and a share-for-share exchange on the basis of 1 share in Hull for every 4 held by Step’s shareholders. Hull's shares had a market value of £4.00 at that time. Hull has not yet accounted for this share exchange. At the date of acquisition, the fair value of the Non-controlling interest was £1.9m and Hull considered the fair value of a building held by Step to have a fair value £400,000 in excess of carrying value. At that time the building had a useful life of 20 years with no residual value. Depreciation is charged on a monthly basis. There has been no change in Hull's share capital or share premium since acquisition.

2. Inter-group sales from Hull to Step in the year ending 31 December 2019 were £1.5m, on which Hull earned a gross margin on sales of 20%. Step still holds part of this inventory at 31 December 2019 which it values at £0.5 million.

Required:

a) Prepare a consolidated income statement for the year ended 31 December 2019. (10 marks)

b) Prepare a consolidated statement of financial position at 31 December 2019.

(20 marks)

(Total 30 marks)

Question 2: Conceptual Framework and Intangible Assets

Research and development costs play a vital role in an entity’s economic sustainability, although the IASB requires very different accounting treatment for each, based on IAS 38 Intangible Assets and the Conceptual Framework for Financial Reporting (2018). This has led to an argument that a “flawed application of the balance sheet (asset valuation) model during the dramatic shift of corporate value-creating resources from tangible to intangible assets (is) resulting in an increasing mismatch between revenues and expenses” 1

Required:

Discuss whether you feel that IAS 38 Intangible Assets causes a mismatch between revenues and expenses, based on the Conceptual Framework’s fundamental qualitative characteristics, definitions for assets and expenses, and recognition

criteria. (Total 20 marks)

SECTION B

Question 3: Published Financial Statements.

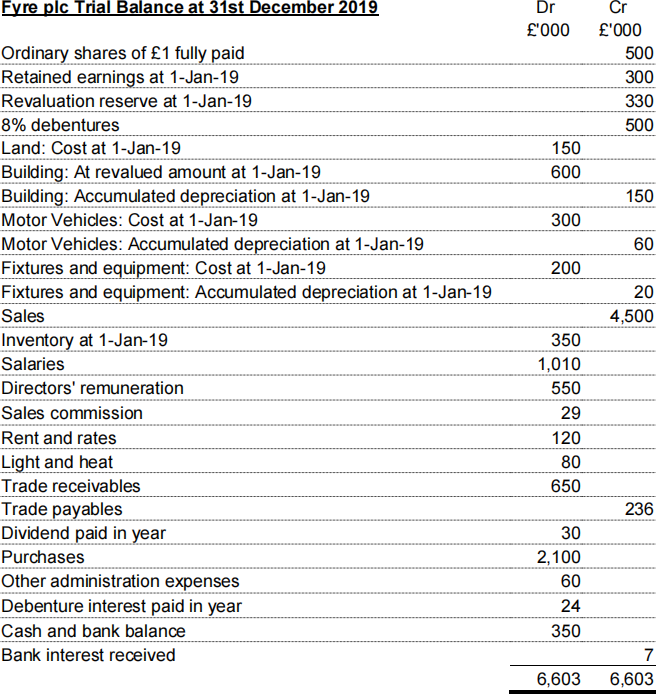

The trial balance at 31 December 2019 for Fyre plc, a manufacturing company is:

Additional information is available as follows:

1. Closing inventory on 31 December 2019 is valued at £380,000.

2. The building, which originally cost £300,000, was revalued some years ago. It was damaged on the first day of the current reporting year (1 January 2019) and the directors revised its value down to £240,000. Its remaining useful life at the time was 30 years. An adjustment is required to account for this impairment.

3. No non-current assets were bought or disposed of during the year.

4. The buildings, equipment and vehicles are expected to have no residual value at the end of their useful lives. Depreciation is calculated as follows:

• Buildings: a straight line basis, based on revalued amount and remaining useful life at revaluation date

• Motor Vehicles: 20% reducing balance per annum

• Fixtures and equipment: 10% straight line per annum

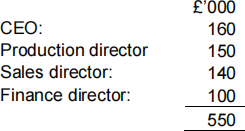

5. Directors’ remuneration is made up as follows:

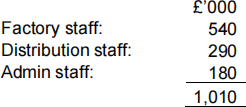

6. Salaries are to be allocated as follows:

7. All other unallocated expenses, including buildings and fixtures/equipment depreciation, are to be allocated according to the proportion of space occupied as follows:

Factory: 50% / Distribution: 25% / Administration: 25%

8. Tax for 2019 is estimated at £80,000 (payable in the next accounting year) .

Required:

a) Discuss whether the Conceptual Framework’s qualitative characteristics support

the use of a revaluation model as opposed to historic cost. (5 marks)

Prepare for publication, showing all your workings:

b) A Statement of Comprehensive Income for the year ended 31 December 2019. (10 marks)

c) A Statement of Financial Position as at 31 December 2019.

(10 marks)

(Total 25 marks)![]()

Question Four: Earnings Per Share.

Below are extracts from the income statements for Tree plc (Tree) for the years ended 31 December 2018 and 2019, and additional information needed to prepare earnings per share ratios for both years:

Tree reported an earnings per share of 37p for the year ended 31 December 2017 During the year ended 31 December 2018:

On 1 January 2018 Tree had 5m ordinary shares in issue. On 1 May 2018, Tree made a rights issue on the basis of one share for every four in issue, at a cum rights price of £3.50, when the market price per share was £5.00.

During the year ended 31 December 2019:

On 1 May 2019, Tree made a bonus issue on the basis of one share for every five in issue. Tree also issued £3 million worth of 4% convertible loan stock at par on 1 April 2019, redeemable at par on 31 December 2023 or convertible into 15 shares per £100 at the choice of the holder.

Required:

a) Calculate Tree’s earnings per share (EPS) for the year ended 31 December 2018, including a comparative EPS for 2017. (8 marks)

b) Calculate Tree’s earnings per share (EPS) for the year ended 31 December 2019, including a comparative EPS for 2018. (4 marks)

c) Calculate Tree’s Diluted Earnings per Share for the year ended 31 December

2019 and explain why this is regarded as useful information for the ordinary shareholders of Tree, in addition to the Basic Earnings per Share. (8 marks)

d) Discuss whether the Conceptual Framework’s qualitative characteristics support the need for disclosure of both Basic and Diluted Earnings per Share. (5 marks)

(Total 25 marks)

Question 5: Provisions and Impairment

Soola plc is a mining business that operates in a number of different countries. It is facing a challenging year ended 31 December 2019, and you have been asked to explain the accounting treatment for the following three items:

Item 1: Clean Up of toxic waste

Soola has been silver mining in the country of Freedonia for many years. To clean the silver, Soola uses toxic chemicals which it then deposits back into the mines. There has never been any legislation requiring the cleaning up of environmental damage in Freedonia. Soola has a policy of only observing its environmental responsibilities when legally obliged to do so. In December 2019, the Government of introduced laws forcing mining companies to clean up environmental damage that they had caused in the past. Soola estimates that the damage already caused will cost £10m million to rectify, with the work starting in February 2020, although the work would not be payable until December 2021. It also estimates that damage likely to be caused by its operations each year for the remaining four years of the mines' lifespan will be £2 million, payable at the end of each relevant year. The required return (discount rate) specific to this operations is 10%.

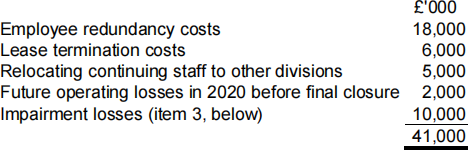

Item 2: Closure of Operations

Due to increasing costs and a fall in demand , Soola decided to close a business operation in the country of Malania. The decision was approved in the directors’ board meeting on 15 December 2019, and an outline of a plan was immediately announced to employees alongside a press release. The closure began on 4 January 2020, and the sale of the division is expected on 30 June 2020. The costs associated with the closure include:

The directors are seeking your advice on whether a provision is required, and if so, the amount to be recorded.

Item 3: Impairment relating to Closure of Operations

Prior to the decision to close (item 2), an impairment review was undertaken for the business operation in Malania. The review assessed the recoverable amount to be £20m and an impairment loss of £10m was recognised in the income statement . The net assets of the business operation prior to the impairment were:

![]()

The directors are seeking your advice on whether how to allocate the £10 million impairment loss between the net assets of the business operation.

Required:

a) Prepare notes setting out and explaining how each of the three items outlined should be accounted for and disclosed in the financial statements of Soola for the year ended 31 December 2019. Your answer should refer to relevant International Accounting Standards and the principles of the Conceptual Framework. (20 Marks)

b) Discuss whether the process of an impairment review complies with the Conceptual Framework’s qualitative characteristics. (5 Marks)

(Total 25 marks)

2022-01-25