FNCE 4308 - Introduction to Algorithmic Trading

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FNCE 4308 - Introduction to Algorithmic Trading

Final Examination (due before Friday, November 21, 2025, 6 PM EST)

This is an individual examination. You are required to submit your report, where you describe your process and answer questions, in a Word document, as well as all .m and .mat (or Excel) files on HuskyCT.

(1) Download at least 3 years of daily prices of a financial instrument other than S&P 500 ETFs.

(2) Modify the stationarityTests.m script to run the ADF and variance-ratio tests, estimate the Hurst exponent, estimate the half life of mean reversion, and backtest the strategy discussed in class. The strategy calls for the daily dollar amount of the position in the instrument to equal -1 * (its price – its moving average )/its moving standard deviation.

(3) Use the stepwiseLR.m script to estimate a stepwise regression tree that predicts the 1-day return and uses the 1-, 2-, 5-, and 20-day returns as potential predictors. Make sure to change the value of the “tday” variable to “1:your number of observations” without the double quotes. Also, replace line 77 with “plot(cumret);” without the double quotes. The strategy consists of taking a long position on days when the predicted return is positive, and a short position on days when the predicted return is positive.

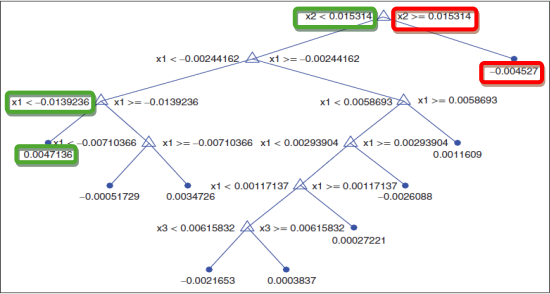

(4) Use the SmallrTree.m script to estimate a regression tree that predicts the 1-day return and uses the 1-, 2-, 5-, and 20-day returns as potential predictors. Again, make sure to change the value of the “tday” variable to “1:your number of observations” without the double quotes. Submit a picture of the regression tree in your report. Use this tree to change the code in (5).

(5) Modify the SmallrTree.m script to backtest a strategy that takes a long position based on the path (in the tree from question 4) that yields the highest expected 1-day return, and a short position based on the path that yields the lowest expected 1-day return.

For example, the below tree suggests a long position for days when the 2-day return is less than 1.53% and the 1-day return is less than -1.39%; that path yields the highest 1-day expected return of 0.47%. A short position should be taken on days when the 2-day return is greater than 1.53%.

(6) Compare the pictures of the cumulative profit chart from all 3 strategies.Which strategy seems to be more profitable? Why? Explain the details of your argument.

2025-11-21