Linear regression

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

1. random variable basics:

a) Given that  is normed, non-negative & linear [ specifically as in Chpt.5, p.4 ]

is normed, non-negative & linear [ specifically as in Chpt.5, p.4 ]

verify that the continuity property:

is equivalent to σ-linearity:

(b) Verify

c)

2. Lebesgue linear spaces

a) For R-valued random variables, any p > 0, we define, exactly as on p.39 of Chpt.5,  But in that case, specifically for p = 1, for any X ∈ L1, verify that |EX| ≤ E|X|, and describe the circumstances for equality.

But in that case, specifically for p = 1, for any X ∈ L1, verify that |EX| ≤ E|X|, and describe the circumstances for equality.

b) For Rn-valued random variables as on pp.27-31, Chpt.6, any p > 0, we define  So explain simply how it is that

So explain simply how it is that

c) For any  , show that |EX| ≤ E|X| and indicate the precise circumstances for equality.

, show that |EX| ≤ E|X| and indicate the precise circumstances for equality.

3. Linear regression in practice

a). For X1,...,Xk & Y in L2, the correlation coefficient of Y with  = op(Y |1, X1,...,Xk) is usually/often referred to in the literature on multivariate statistics, as the multiple correlation of Y on X:

= op(Y |1, X1,...,Xk) is usually/often referred to in the literature on multivariate statistics, as the multiple correlation of Y on X:

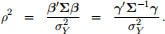

In the notation of ESP6.12 show that if |Σ| > 0 and σY > 0, then

b). In the special case of polynomial regression, we find that for any X & Y in L2, there will be unique coefficients β0,..., βk such that

4. statistical independence & conditional expectation

Given any distribution

and suppose X statistically independent of Y [Chpt.6, Defn.5.7.1, p.53, Eqn(103)]

— denoted

(a) Show that

(b) For any  explain why it is automatic that

explain why it is automatic that

(c) Prove that

5. Indefinite integral of  with respect to P

with respect to P

denoted  or, much more simply, by dλ = XdP.

or, much more simply, by dλ = XdP.

Verify the following :

a) λ is σ-additive.

b) uniqueness :

2025-11-12