MATH 375 Stochastic modelling in insurance and finance

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

MATH 375

MOCK FINAL ASSESSMNET

Stochastic modelling in insurance and finance

1. Let α, β, γ, λ, x0 , be given positive constants, and (~W(t), t k 0) a standard Brownian motion under the risk-neutral probability measure ![]() . Let (x(t), t k 0) be the solution to the following equation:

. Let (x(t), t k 0) be the solution to the following equation:

Consider the following interest rate model:

i) Can the process (r(t), t k 0) take a negative value for some t k 0? Justify your answer.

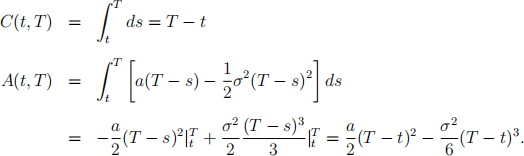

ii) Derive the price p(t, T) of the zero-coupon bond.

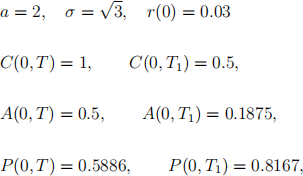

iii) Let α = 1, β = ,3, γ = 1, λ = 1, x0 = 0.03. Consider a forward con- tract on the zero-coupon bond of part (ii) with maturity T = 1, the delivery date of which is T1 = 0.5 and the delivery price is K = 0.8. Find the value of this forward contract at time t = 0 for the holder with a short position. [10 marks]

Solution. [Similar to seen.]

(i) Yes, this process can take a negative value since:

where ~W(t) 』N(0, t), and thus there is a positive probability for r(t) < 0.

(ii)

where a := γ + λα and σ := λβ. The price of the zero-coupon bond is:

where

(iii) The required price is Kp(0, T1 ) 十 p(0, T). For the given numerical values, we have:

Finally, the required price is Kp(0, T1 ) 十 p(0, T) = 0.0648.

2. State the three types of recovery rules for the intensity based credit risk models. If the intensity is constant, i.e. γ(t) = λ > 0 for all t k 0, then what is the expected value and the variance of default time τ under the risk-neutral probability measure?

Solution. [Partially seen.]

The three recovery rules in the intensity based models are: zero-recovery, frac- tional recovery, and recovery at default. If γ(t) = λ > 0 for all t k 0, then τ 』 Exp(λ) under the risk-neutral probability measure, i.e. τ is an exponential random variable with parameter λ. Its mean and variance are thus:

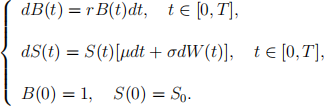

3. Consider a market of a bank account B(t) and a stock S(t), that satisfy the equations:

Here r, µ, σ, S0 are known positive constants, and (W (t), t ↓ [0, T]) is a standard Brownian motion. Let 0 < K1 < K2 be two given constants. Consider a contract with the following terminal payoff:

Find the price X(t) at time t ↓ [0, T] of this contract.

Solution. [Unseen, but the pricing of derivatives is covered.]

This is a super-share option, and its terminal payoff can be written as:

which means that it is the difference of terminal payoffs of two European stock- or-nothing call options with strike prices K1 and K2 . The required price is:

where

The student is expected to derive this price rather than just state it.

2022-01-17