MATH375 Class Test 2

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

MATH375 Class Test 2

In all questions below (W (t), t > 0) is a standard Brownian motion and (于(t), t > 0) is its natural filtration.

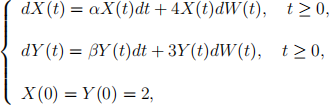

1. Consider the following stochastic differential equations:

where α and β are constants. Find the differentials of X〇 (t) and Y2 (t). What values should α and β take so that X〇 (t) and Y2 (t) are martingales with respect to (于(t), t > 0)?

2. Let a, b, σ, be positive constants, and X尸 a real number. The differential of the process (X(t), t > 0) is:

Find solution X(t) of this equation. What is the distribution of X(t)?

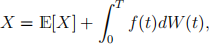

3. Let a and b be given constants. Also let the random variable X be defined as: X := cos(aW (T) + b).

Find the representation:

i.e. find 3[X] and the process (f(t), t e [0, T]).

2022-01-17