MANG6299W1 QUANTITATIVE FINANCE 2019-20

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

MANG6299W1

SEMESTER 1 EXAMINATIONS 2019-20

QUANTITATIVE FINANCE

This paper contains FIVE questions, and each question is worth 25 marks.

Answer FOUR questions in total.

If you attempt more questions than required, only the required number of answers will be marked. Please strike through any answers that you do not wish to be marked. If you do not do this the marker will mark the answers in the order that they appear in your exam booklet(s).

For each question, an outline marking scheme is shown in brackets to the right of each question.

Only University approved calculators may be used.

A foreign language direct ‘Word to Word’ translation dictionary (paper version) ONLY is permitted provided it contains no notes, additions or annotations.

1. Provide a brief explanation of the following:

a) homoscedasticity

[5 marks]

b) moving average (MA) model

[5 marks]

c) kurtosis

[5 marks]

d) non-rejection region

[5 marks]

e) the F-test

[5 marks]

2. Suppose that two variables, ![]()

![]() and

and ![]()

![]() , are related by means of the following regression model:

, are related by means of the following regression model: ![]()

![]() =

= ![]()

![]()

![]() +

+ ![]()

![]() . Notice there is no constant in the regression, a special case of the regression line.

. Notice there is no constant in the regression, a special case of the regression line.

a) Assuming this is a good description of the relationship between the two variables, find ![]() , the Ordinary Least Squares (OLS) estimator of

, the Ordinary Least Squares (OLS) estimator of ![]() .

.

[10 marks]

b) Using the sample of six observations below, compute:

i) ![]() , the OLS estimator of

, the OLS estimator of ![]() obtained in a).

obtained in a).

ii) the sample estimator of the variance of the error term Var(![]()

![]() ).

).

[7 marks]

c) Explain any two properties of the OLS estimator.

[8 marks]

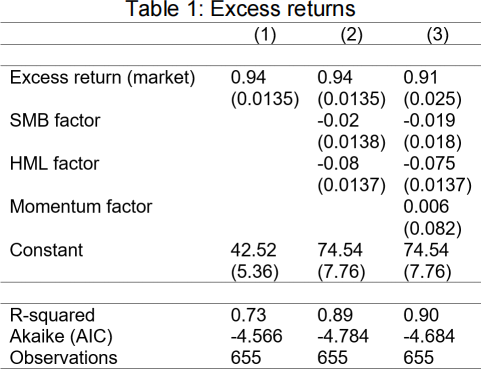

A3. This exercise is based on the CAPM model, as well as the

Fama and French three factor and the four factor models. Three regressions were estimated, and the most relevant output has been summarised in the following table:

Notes: The coefficients are estimated by OLS; their standard errors are in parentheses.

The dependent variable is the excess return on a portfolio of 50 stocks over the risk-free interest rate. The free risk asset to compute excess of return is the 3-month treasury bill.

a) In column (1), the regression includes only the excess returns on the market (proxied by the stock market index). Explain how this regression tests the CAPM model and the meaning of the two coefficients.

[7 marks]

b) In column (2), two additional factors are considered: the book-to-market factor (HML) and the size factor (SMB). This is the three-factor model. Does this model fit the data better than the CAPM? Perform the suitable hypothesis test to support your answer.

[7 marks]

c) In column (3), we consider one additional factor to the previous model. This is the so-called “momentum” factor, which captures the tendency for the stock price to continue rising if it is going up and to continue declining if it is going down. Should the momentum factor be included in the regression? Perform the suitable hypothesis test to support your answer.

[5 marks]

d) The table also indicates the R-squared and the Akaike information criterion for each of the three regressions. Using these statistics, which model would you select as the best?

[6 marks]

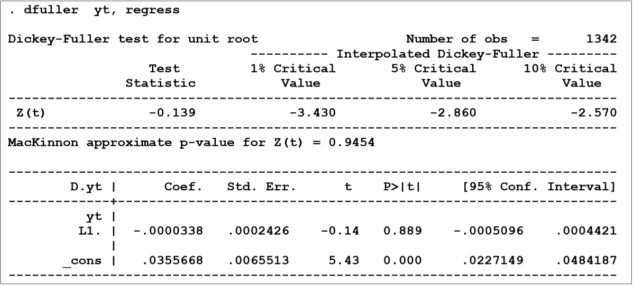

4. The main variable of interest is yt.

a) Use the Stata output below to test if the variable features a unit root. What is the conclusion?

[9 marks]

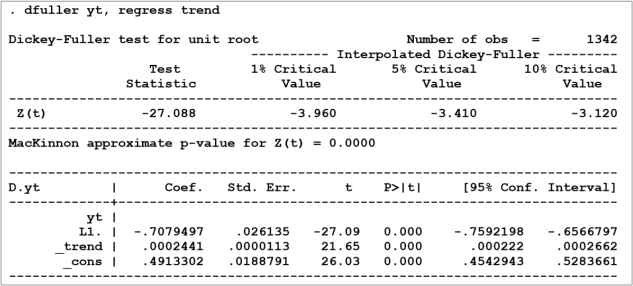

b) We now perform a second test, adding a time trend to the model outlined in part a). Below you can find the Stata

output. Perform the test for a unit root. Is the conclusion the same than in a)? Explain the differences between the two tests.

[9 marks]

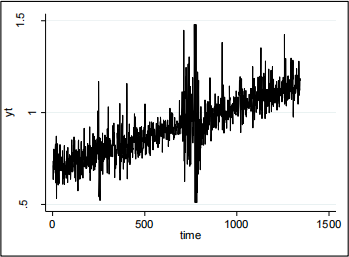

c) Below you can find a plot of the series ![]()

![]() over the relevant time period. What does this plot suggest regarding the two tests for a unit root you have carried out?

over the relevant time period. What does this plot suggest regarding the two tests for a unit root you have carried out?

[7 marks]

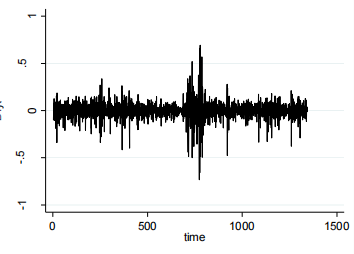

5. The exchange rate in logs is represented by ![]()

![]() , which is measured with a daily frequency. The main variable of interest is its first difference (∆

, which is measured with a daily frequency. The main variable of interest is its first difference (∆![]()

![]() ).

).

a) The plot below shows ∆![]()

![]() over time. Explain the concept of volatility clustering.

over time. Explain the concept of volatility clustering.

[8 marks]

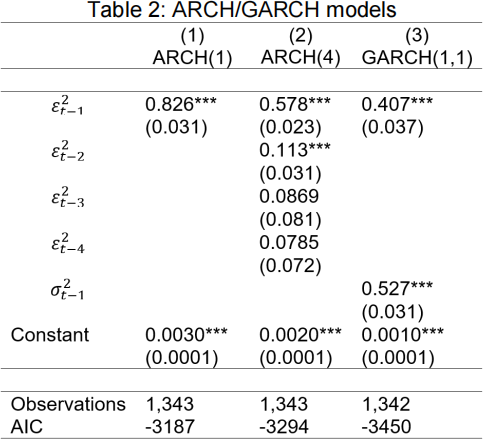

b) The table below shows estimates of three models of volatility: ARCH(1), ARCH(4) and GARCH(1,1). In the three models, the conditional mean equation for ∆![]()

![]() only includes an intercept ( ∆

only includes an intercept ( ∆![]()

![]() =

= ![]() +

+ ![]()

![]() , where

, where ![]()

![]() is the error term with variance

is the error term with variance ![]()

![]() 2).

2).

i) Outline the equation for the conditional variance of the ARCH(1) model. Based on column (1), identify the estimates of the key parameters.

[7 marks]

ii) Explain which of the three models provides the best fit and compare them.

2022-01-15