ACFI201: Financial Reporting I 2021

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

JANUARY EXAMINATIONS 2021

ACFI201: Financial Reporting I

Question 1

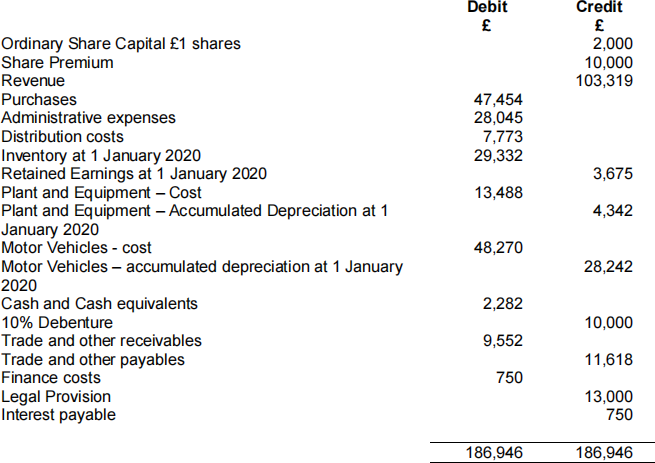

Highfields Ltd has prepared the following trial balance at 31 December 2020 before taking

Additional information

1. Inventories as at 31 December 2020 had a cost of £28,000

Within this figure there are some items currently included at their cost of £8,000 that have become damaged they can only be sold for £9,000 once they have had repair work at a cost of £3,500.

2. On 30 June 2020 Highfields issued 500 new £1 shares at a price of £5 per share, this was accounted for correctly in the Trial Balance above

3. A dividend of 50p per ordinary share was paid on 1 October 2020 on the correct number of shares in issue at that date. This was incorrectly debited to admin expenses.

4. Highfields Ltd charges depreciation as follows:

![]() Plant and Machinery – straight line over 10 years charged to cost of sale

Plant and Machinery – straight line over 10 years charged to cost of sale

![]() Motor vehicles – 25% per annum reducing balance charged to distribution costs

Motor vehicles – 25% per annum reducing balance charged to distribution costs

5. The legal provision relates to ongoing litigation from a customer relating to a faulty product sold to them. On 31 December 2020 legal advisors received new updated information about the legal provision.

The latest advice is there’s a 20% chance no settlement is required, 25% chance £5,000 will need to be paid and 55% chance £10,000 will need to be paid. Expenses relating to this are taken to Admin expenses.

6. Within plant and machinery there is a piece of machinery bought on 1 January 2019 for £2,000. At 31 December 2020 due to changes in customer demand its value in use is £1,300, it could be disposed of for £1,600 however selling costs of 8% would be incurred. Any impairment is to follow the same treatment as depreciation,

7. Included in trade and other receivables is a sale of $2,800 made on 10 December 2020.This was correctly translated at an exchange rate of $1.25/£1 at 10 December. The exchange rate on 31 December 2020 was $1.35/£1, no entries have been made to reflect this. Exchange differences are treated as admin expenses.

8. The final quarter of interest on the debenture has not been accounted for, the debenture is due to be settled on 31 December 2026.

9. The income tax charge for the year has been estimated as £2,850.

Requirement

a) Prepare a statement of profit or loss, and a statement of changes in equity for Highfields Ltd for the year ended 31 December 2020 and a statement of financial position as at 31 December 2020, in a form suitable for publication.

Notes to the financial statements are not required, expenses should be presented analysed by function and ignore the tax effects of any adjustments.

(25 marks)

b) With reference to the conceptual framework, does the legal provision meet the definition of a liability and why?

(3 marks)

(28 marks)

Question 2

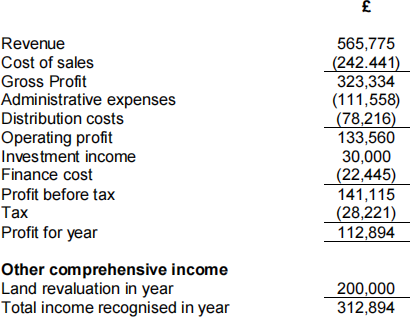

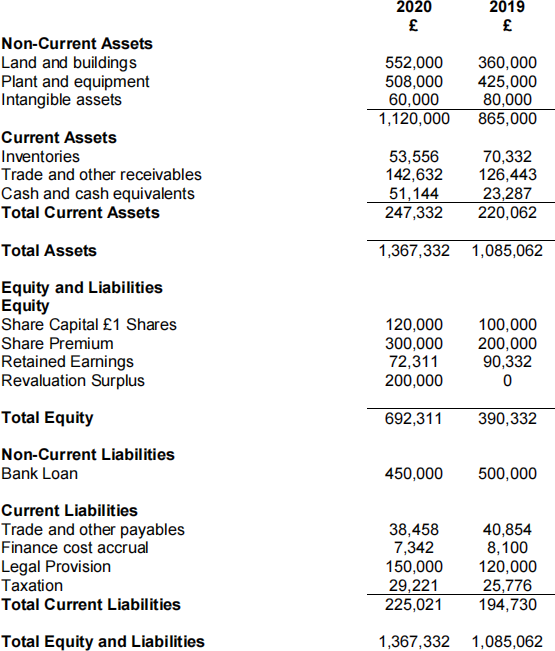

Kylemore Ltd (a toy manufacturer) has prepared the following financial statements and additional information as at 31 December 2020.

Statement of profit or loss and other comprehensive in income for year ended 31

December 2020.

Statement of Financial Position at 31 December 2020

Additional information

1. The depreciation charge in the year was £8,000 for buildings and £75,000 for plant and equipment.

2. Kylemore sold plant and equipment with a carrying amount of £22,500 and made a gain on disposal of £7,500. The gain on disposal has been credited to administration expenses. There were no disposals of plant and equipment during the year.

3. Within trade and other receivables there is a balance that relates to interest receivable of £20,000 for year ended 2020 (£15,000 year ended 2019).

4. There were no acquisitions or disposals of intangibles in the year.

5. At the year end, one of Kylemore’s purchased brands with a carrying amount of £30,000 was assessed as having a recoverable value of £20,000.

6. There was an ordinary share issue in the year.

7. New information became available regarding ongoing litigation based on which Kylemore’s legal provision was revised.

8. Kylemore paid an ordinary dividend in December 2020

Requirements

Prepare a statement of cash flows for Kylemore in accordance with IAS 7 Statement of cash flows for the year ended 31 December 2020. The indirect method should be used starting with profit before tax.

(Total: 23 marks)

Question 3

You are a recently qualified financial controller of Ashcroft PLC, a company that manufactures and sells Tablet PCs. You are helping prepare the financial statements for the year ended 30 September 2020 which must comply with International Financial Reporting Standards.

The following issues have been identified as outstanding by the finance director and they have asked you to review them.

Research and Development

On 1 December 2019 Ashcroft began work to develop a new processor to incorporate into future Tablet PCs, in the early stages results were inconclusive. However on 1 April 2020, incorporation of the new processor into future tablets was approved by the board, and future funds to continue work to conclusion on it were made available.

Costs relating to research and development of this processor up to 30 September 2020 are £300,000 and accrue evenly over that time. As at 30 September 2020 the processor is incomplete and due for launch on 1 June 2021.

Corporate sale with support

On 1 July 2020 Ashcroft entered into an agreement to supply a customer with Tablet PCs for a price of £60,000.

The price includes after sales technical support to them for the next 2 years. The cost of providing the support is estimated to be £5,000 per annum, the entity earns a mark-up of 25% on support contracts.

The usual selling price of the tablet PCs is £62,500

Requirement

a) Explain the accounting treatment of these items and they impact they would have on the financial statements in the year ended 30 September 2020

(17 Marks)

b) How would the accounting treatment differ for research and development had it been under UKGAAP?

(2 Marks)

As of 1 October 2019 Ashcroft had in issue 200,000 £1 ordinary shares. On 1 February 2020 Homer issued 100,000 at the market rate of £3 per share. On 1 June 2020 Ashcroft made a 1 for 6 rights issue of £2.10 a share, at this date the market rate was £2.80 a share.

Profit attributable to ordinary shareholder in the year ended 30 September 2020 was £345,000

EPS for year ended 30 September 2019 was 96.8p per share.

There had been no other share issues prior to this for a number of years

c) Calculate earnings per share and restate prior year comparative.

(7 Marks)

Question 4

You are acting as a financial reporting consultant to Ottos plc, a company that owns and runs a chain of restaurants throughout the UK and Ireland. They are in the process of finalising the financial statements for the year ended 30 September 2020 and have come across the following issues that need addressing.

Future sale of Irish restaurants

On 30th June 2020, the board made the decision to sell its Irish restaurants. As at 30th June 2020 they have a carrying amount of £3,000,000 in the financial statements. A sales price of £5,000,000 has been agreed with an interested party, the board are confident the sale will be completed in the next 6 months. The legal costs of the sale are expected to be £50,000 and there is 2% agent’s commission on sale.

Profit from the Irish restaurants in the year ended 30 September 2020 is expected to be £120,000 of the total company profit of £650,000.

Government Grant

On 1 April 2020 Ottos replaced all its ovens for a new energy saving model at a total cost of £80,000, they have been able to secure a government grant of £20,000 to help fund this construction. The expected life with nil residual value of the ovens is 4 years.

The directors want to consider all available accounting treatments possible for this

Poor Quality Wine.

A consignment of 500 bottles wine purchased during September 2020 was later found not to be of adequate drinking quality. The cost of the wine had been £10 per 750ml bottle, Otto had expected to sell this by the glass as £7 per 250ml. Due to the less than adequate taste the wine was considered only good enough to make a red wine sauce which could be sold to customers at £2 per 250ml after incurring conversions costs of 50p per 250ml serving.

Requirement:

a) Advise the directors how each of the above issues should be dealt with in the financial statements for the year ended 30 September 2020

(20 Marks)

A friend of yours that works for an investment bank is interested in investing in shares in Ashcroft PLC, she’s heard about ongoing work regarding development of a new processor, she understands its success will impact the share price and has asked us for an update on its progress.

b) Explain the ethical issues with this request and the possible courses of action you should take.

(3 Marks)

2022-01-14