Fin 5240 Options and Futures HW 1

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Fin 5240

Options and Futures

HW 1

2.1. What rate of simple interest is equivalent to a continuous compounding rate of 5%? And what continuous compounding rate is equivalent to a simple interest rate of 10%?

2.2. You will receive $110 in one year for an investment of $100 today. What is the percentage rate of return per annum (p.a.) with:

a) annual compounding?

b) semiannual compounding?

c) continuous compounding?

2.3. A 1-year forward contract on a non-dividend paying stock is entered into today when the stock is $40 and the risk-free rate is still 10% p.a.

a) What is the forward price today (time 0) ?

b) Six months later (time 0.5), the price of this stock is $45 and the risk-free rate is still 10% p.a., what is the forward price ?

c) Suppose you have a long position at time 0, what is the value of the contract if the stock price turns out to be 30 and 50 at T (time 1), respectively ?

d) Suppose you have a short position at time 0.5, what is the value of the contract if the stock price turns out to be 30 and 50 at T (time 1), respectively ?

e) Suppose you have both the long and short positions in Problems c) and d), what is the value of your positions if the stock price turns out to be 30 and

50 at T (time 1), respectively ?

2.4. A stock is expected to pay a dividend of $1 per share in 2 months and in 5 months. The stock price is $50 and and the risk-free rate of interest is 8%. An investor has just taken a long position in a 6-month forward contract on the stock.

a) What is the present value of the dividends ?

b) What should be the forward price today ?

c) Three months later, the price of the stock is $48 and the risk-free rate is still 8% p.a., what is the forward price ?

2.5* . (note: the stared problems are more challenging, but you are encouraged to solve them which may occur as bonus questions in exams.) A bank offers a corporate client a choice between borrowing cash at 11% p.a. and borrowing gold at 2% p.a. with annual compounding. (If gold is borrowed, interest and principal must be repaid in gold.) With continuous compounding, the risk-free rate is 9.25% p.a. and storage costs are 0.5% p.a. Discuss whether the interest rate on the gold loan is too high or too low relative to the interest rate on the cash loan.

2.6** . Let F1 and F2 be two futures contracts on the same commodity with maturity dates t1 and t2 , 0 < t1 < t2 . Show that

F2 ≤ (F1 + C)eˆ(r)(t2 −t1 )

where ˆ(r) is the forward rate, i.e., the interest rate between t1 and t2 one can lock in today (t = 0), and C is the cost of storing the commodity between t1 and t2 discounted to time t1 .

2.1. R = er − 1 = e.05 − 1 = 0.0512711 = 5.13% and r = ln(1 + R) = ln(1 + .10) = 0.0953102 = 9.53%.

2.2. a) 100(1 + R) = 110 ⇒ R = 10%; b) We have 100(1 + 2/R)2 = 110, and hence 1 + R 2/R = √1.1 ⇒ R = 9.76%;

c) 100er = 110 ⇒ r = 9.53%.

2.3. a) F = SerT = 40 × e.10 × 1 = 44.21; b) F6 = S6 er(T −t) = 45 × e.10 × .5 = 47.31

c) If the stock price is 30 or worth 30, you lose (44 .21 − 30) = 14.21 as you promise to buy it at 44.21. If the stock price is 50, you make (50 − 44.21) = 5.79.

d) If ST = 30, make 17.31 (as you promise to sell it at 47.31 and whoever on the other side has to buy it from you at this price); and if ST = 50, lose 2.69.

e) If ST = 30, (17.31 − 14.21) = 3.1; and if ST = 50, (5.79 − 2.69) = 3.1 (actually, it is always equal to 3.1 whether the stock price is 50 or 100 or whatever!)

2.4. a) D = 1 × e − .08 × 12/2 + 1 × e − .08 × ![]() = 1.954; b) F = (S − D)er(T −t) = (50 − 1.954)e.08 × .5 = 50.01;

= 1.954; b) F = (S − D)er(T −t) = (50 − 1.954)e.08 × .5 = 50.01;

c) D3 = 1 × e − .08 × 12/2 = 0.987, F3 = (S3−D3)e r(T −t) = (48−0.987)e .08×.25 = 47.96

2.5. * (The stared problem is optional to MBAs, but encouraged to MSs. The problem

is challenging, and may be demanding at times!)

On the cash loan, the bank earns a spread over the risk-free rate:

10.44% − 9.25% = 1.19% (p.a.)

(10.44% is the continuous compounding rate of 11%) to compensate for default risk, administrative costs, etc.

Assume first that there is no interest on the gold loan. The bank can buy gold from the market and loan it to its client; and sell a futures contract at price

F0 = S0 e(r+c)(T −t) = S0 e( .0925+ .005)T = S0 e.0975T

so, assume no default risk, the bank is going to earn 9.75% on its money spent on gold.

Now, the continuous compounding rate on the gold loan is 1.98%. The bank can lock in this payment in the futures market as well. Together, it can earn 11.73%. The spread over the risk-free rate is 2.48%. This rate appears too high which may be the reason why in practice banks are ready to make loans at 2% (p.a.). However, the high rate may be due to the fact that more administrative costs are incurred in a gold loan.

2.6. * Suppose F2 > (F1 + C)eˆ(r)(t2 −t1 ) , then an arbitrageur can do: a) long a futures

contract which matures at t1 ; b) short a futures contract which matures at t2 ; c)

lock in the rate ˆ(r) on F1 + C between t1 and t2 .

When the first contract matures, the asset is bought at F1 and stored until t2

when the asset is sold at F2 . A positive profit of [F2 − (F1 + C)eˆ(r)(t2 −t1 ) ] is then

made. This cannot prolong and hence F2 ≤ (F1 + C)eˆ(r)(t2 −t1 ) .

3.1. A 1-year forward contract on a non-dividend paying stock is entered into when the stock is $50 and the risk-free rate is 6% p.a.

a) What is the value of the short position six months later when the stock is $30 and the risk-free rate is 7% p.a. ? The short position ?

b) What is the value of the contract at maturity when the stock is $100 ?

c) What are the answers if the stock pays $1 dividend in 3 and 9 months ?

3.2. (Hull’s Problem) Suppose that you enter into a short futures contract to sell July silver (the maturity is July) for $5.20 per ounce on the New York Commodity Exchange. The size of the contract is 5000 ounces. The initial margin is $4,000 and the maintenance one is $3,000.

a) What change in the future price will lead to a margin call ?

b) What happens if you do not meet the margin call ?

3.3. (Hull’s Problem) Some people have the view that “speculation in futures markets is pure gam- bling. It is not in the public interest to allow speculators to buy seats on a futures exchange.” What arguments can you make to against this viewpoint ?

3.4. Suppose a farmer has all his wealth in wheat and owns 1,000,000 bushels of it. Assume further that the cash price (the spot price or the wheat price in the wheat market) is $5 per bushel today, and the riskfree interest rate is 5%.

a) If the wheat price drops to $3 per bushel tomorrow, what will be his wealth ?

b) Suppose the August futures contract matures in exactly 3 months from today, what should be the futures price today and tomorrow?

c) If he wants to lock in a sell-price today, should he be long or short ? If the contract size is 5000, how many contracts ? What will be his wealth tomorrow?

3.5. In practice, a wheat futures contract calls for the delivery of 5000 bu (bushels) of wheat (the size of the contract is 5000 bu). The price is quoted in cents and the tick size (minimum trading price move) is ![]() cents (worth $12.50=5000 ×

cents (worth $12.50=5000 × ![]() cents). On January 14, 1999, the open, high, low and close prices are 274, 277

cents). On January 14, 1999, the open, high, low and close prices are 274, 277 ![]() , 274 and 276

, 274 and 276 ![]() for the March contract.

for the March contract.

a) If you buy one wheat futures at the open, how much money will you make at the end of the day?

b) If the initial margin and maintenance margin are $950 and $700 for trading one wheat futures contract (slightly different at different futures brokerages), how much money do you need in your account to trade the wheat contract?

c) If you buy one wheat futures at the open on 1/14/99, you will lose money when the price goes down in the following days. Starting with $1000, at what price level will you receive the margin call ?

d) How much money do you need to never receive a margin call?

4.1. You are a consultant in risk management.

a) If a corn farm wants to lock in a sell price for his 100,000 bu of corn anticipated to harvest. Should you suggest him to sell/short or buy/long corn futures?

b) How many contracts to sell or buy given that the size is 5000 bu. ?

c) If a producer/buyer needs 1,000,000 bu of corn, how would you answer a) and b)?

4.2. The standard deviation (std) of monthly changes in the spot price of live cattle is (in cents per pound) 1.2. The std of monthly changes in the futures price of live cattle is 1.4. The correlation between the price changes is 0.7. It is now Oct. 15. A beef producer plans to purchase 200,000 pounds of live cattle on Nov. 15, and wants to use the Dec. contract to hedge risk. Each of the contract is for the delivery of 40,000 pounds of cattle. What strategy should he/she follow?

4.3. (Hull’s Problem; optional) The following table gives data on monthly changes in the spot price and the futures price for a certain commodity. Use the data to calculate a minimum variance hedge ratio for a company that knows it will purchase the commodity in one month.

∆S +0.50 +0.61 -0.22 -0.35 +0.79 +0.04 +0.15 +0.70 -0.51 -0.41 ∆F +0.56 +0.63 -0.12 -0.44 +0.60 -0.06 +0.01 +0.80 -0.56 -0.46

Evaluate how well a hedging strategy based on the minimum variance hedge ratio would have worked during each month of the ten-month period covered by the data.

4.1. a) Sell/Short, locking in a sell price; b) 100,000/5000=20 contracts; c) Long/Buy, 200 contracts.

4.2. The optimal hedge ratio is: h = 0.7 × 1.4/1.2 = 0.6, that is, short 0.6 “futures contracts” per unit of the asset. Because the beef producer want to hedge 200,000 units, she/he needs to long/buy 200, 000 × 0.6 = 120, 000 “contracts”. But, in practice, each contract controls 40,000 units, So, only need to buy 40,000/120,000 contracts.

4.3. Two ways to solve. I suggest you to just read through the first approach, but implement in detail the 2nd one as it has all the basic idea in practical hedging.

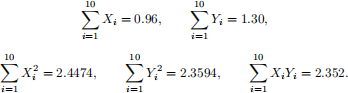

The tedious method: let Xi and Yi be the i-th observation on the change in the futures price and the change in the spot price respectively. Simple calculator computations find the following sums:

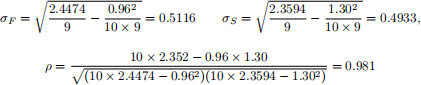

Then the standard deviations and correlations are:

and hence the hedge ratio is

h = ρσS /σF = 0.946

The efficient method: simple using a linear regression. There are two steps: a) input the two series of data into y and x in the linear regression into any package (such as Python or Excel); b) you can run a regression of y on x. Then the hedge ratio, apart from a sign which depends on how one interprets, is

h = β = 0.945636 = 0.946,

where β is the regression slope or coefficient on x.

In a perfect hedging, any ups or downs in the spot price will be offset by those in the futures price. Here it is not a perfect (often so in practice), as the hedge ratio is not 1 or minus 1. Another measure is R2 of the regression. The larger it is, the better the hedging.

For our case here, the spot went to 0.50 in the first month, the hedged (short position) lose 0.56 × 0.946. and so the net is 0.50 - 0.56 × 0.946 = -0.2976, not perfect offset. Similarly, we get 0.01402, -0.10648, 0.06624, 0.2224, 0.09676, 0.14054, -0.0568, 0.01976 and 0.02516 for all other months.

5.1. The annual dividend yield rate is 2% on the S&P500 index and the risk-free rate of return is 4%. If the current index level is 410 and the index futures contract matures in 3 months, what should the futures price be ?

5.2. Suppose that you have opened a futures account and put up $20,000 for the margin. On 9/2/99, you bought one (in a long position) September S&P500 futures contract at the closing price 1320.20 in anticipation of perhaps a good unemployment report tomorrow. For the next two trading days, the (closing) prices went up to 1362.50 and 1363.80.

a) How much money do you have in your account at the end of the two days (ignoring the interest your money may earn) ?

b) If you sell one (in a short position) S&P500 futures contract on the next trading day at the market closing price 1362.50, what obligations do you have down the road? Have you made money or lost money? Is this for sure?

c) Suppose you hold your position and sell one S&P500 futures contract some days later (before expiration) at a even higher price, say 1420.20, what is your profit in the futures trading?

d) Suppose you, as a long-term speculator, bought one December S&P500 futures contract at 1320.20. Assume further that your predict S&P500 index will go up to 1720.20 by the December expiration time (year-end rally, as known on Wall Street). If the futures price gradually rise and you sell your contract at 1720.20, what is your profit ?

e) Suppose you are right that the S&P500 futures price will be 1720.20 by the December expiration time. However, October is known as the crash month. If the stock market just drops 10% in October, and if the S&P500 futures price drops to 1188.20, what is your “profit” at this time ?

5.3. Suppose that there are only two stocks in the stock market. Stock A sells for $50 and has 1,000 shares outstanding. Stock B sells for $40 and has 1,000,000 shares outstanding.

a) If the price-weighted stock index starts from 100, what divisor will you use ?

b) If the value-weighted stock index starts from 100, what divisor will you use ?

c) If A doubles its value to 100 tomorrow and B remains unchanged, what are the levels of your indices ?

d) If A doubles its value to 100 tomorrow and B remains unchanged, and if A splits its shares 2-for-1, what are the levels of your indices ?

5.4. Suppose you are a stock portfolio manager who has already made 25% return with a current value of the portfolio worth $1,000,000,000. Assume that you are concerned about a big drop of the stock market in October because of its high valuation, and you want to hedge half of your portfolio by using the December S&P500 futures. The following information is available to you:

beta of your portfolio β = 1.2

value of S&P500 St = 1340

risk-free rate r = 8%

Dividend yield on S&P500 d = 3%

a) Should you buy or sell futures ?

b) If there are 92 days from today (in September) to the December expiration, what should be the fair futures price today?

c) How many contracts should you buy/sell ?

d) If the S&P500 index drops 30% after 31 days on one “Black Monday” in October, and if your portfolio drops 1.2 times that, what is the value of your entire portfolio (with the hedge) ? And what is the value if you did not hedge ?

e) Alternatively, you can also sell half of your portfolio today (in September) to achieve the same hedging result as d), then why do you use futures?

f) Suppose that one lucky person is going to get a huge amount of inheritance money in December and she/he wants to invest a portion of it to S&P500 index, should she/he buy or sell futures to hedge the price risk ?

6.1. (Hull’s problem) What is the difference between the way in which prices are quoted in the foreign exchange futures market, the foreign exchange spot market, and the foreign exchange forward market?

6.2. (Hull’s problem) The forward price of the Swiss franc for delivery in 45 days is quoted as

1.8204. The futures price for a contract that will be delivered in 45 days is 0.5479. Explain these two quotes. Which is more favorable for an investor wanting to sell Swiss francs?

6.3. (Hull’s problem) The two-month interest rates in Switzerland and the United States with continuous compounding are 3% and 8% per annum, respectively. The spot price of the Swiss franc is $0.6500. The futures price for a contract deliverable in two months is $0.6600. What arbitrage opportunities does this create?

6.4. (Hull’s problem) A foreign exchange trader working for a bank enters into a long forward contract to buy one million pounds sterling at an exchange rate of 1.6000 in three months. At the same time, another trader on the next desk takes a long position in 16 three- month futures contracts on sterling. The futures price is 1.6000 and each contract is on 62,500 pounds. Within minutes of the trades being executed the forward and the futures prices both increase to 1.6040. Both traders immediately claim a profit of $4,000. The bank’s systems show that the futures trader has made a $4,000 profit, but the forward trader has made a profit of only $3,900. The forward trader immediately picks up the phone to complain to the systems department. Explain what is going on here. Why are the profits different?

6.5. (Hull’s problem) When a known cash outflow in a foreign currency is hedged by a company using a forward contract, there is no foreign exchange risk. When it is hedged using futures contracts, the marking to market process does leave the company exposed to some risk. Ex- plain the nature of this risk. In particular, assume that the forward price equals the futures price. Consider whether the company is better off using a futures contract or a forward contract when

(a) The value of the foreign currency falls rapidly during the life of the contract.

(b) The value of the foreign currency rises rapidly during the life of the contract.

(c) The value of the foreign currency first rises and then falls back to its initial level.

(d) The value of the foreign currency first falls and then rises back to its initial level.

2025-10-14