Money and Banking Exercise Set 1 Spring 2024

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Money and Banking

Spring 2024

Exercise Set 1

Due Thursday, 2/8

Question 1 [22 points]

Consider an economy with three dates (T=0, 1, 2) and the following investment opportunity. If an agent invests $1 in a project at T=0, the project yields $4 at T=2. The project can be liquidated at T=1 but early liquidation yields $1 at T=1.

An agent has $1 and is risk avers and can be of two types. With probability 0.2 an agent is a type-1 consumer and with probability 0.8 an agent is a type-2 consumer.

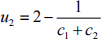

If an agent is a type1-consumer, he only values consumption at T=1 and his utility function is

where c1 is the amount consumed at T=1. If an agent is a type-2 consumer, he values consumption at both T=1 and T=2 according to the utility function

where c1 and c2 are the amounts consumed at T=1 and T=2, respectively.

a) What is the expected utility of the agent? [3 Points]

Now consider a bank that invests in these projects. There are N=1,000 agents. All agents are identical ex ante in the above sense. Suppose they all deposit $1 each with the bank. The bank offers the following demand deposit contract (d1, d2) where d1 is the amount and agent can withdraw at T=1 and d2 is the amount he can withdraw at T=2.

b) Suppose d1=1.2. What is the amount d2 that the bank can offer an agent who withdraws at T=2? What is the expected utility of an agent? [4 Points]

c) Suppose d2=3.6. What is the amount d1 that the bank can offer an agent who withdraws at T=1? What is the expected utility of an agent? [4 Points]

Suppose the bank offers (d1,d2) = (1.4, 3.6). An agent expects that M=630 other agents will withdraw at T=1.

d) What is the best response of the type-2 consumer, i.e. does he has an incentive to run to the bank and withdraw at T=1? [3 Points]

e) What is the maximum number of withdrawals at T=1 such that a type-2 consumer has no incentive to withdraw at T=1. [8 Points]

Question 2 [10 points]

Now consider policy responses in the above economy where a bank offers a demand deposit of (d1,d2) = (1.3, 3.7).

a) Suppose the government wants to suspend convertibility of demand deposit into cash if too many agents are withdrawing. When should a suspension kick in (i.e. how many agents are allowed to withdraw at T=1) in order to avoid that a type-2 consumer withdraws at T=1? Is this number unique? [4 Points]

Suppose the government designs a deposit insurance fund and insures an amount ofI.

b) In order to avoid a bank run of type-2 consumers, the minimum insurance is I=3.7. Please explain if this statement is correct. [3 Points]

c) Suppose I=1.3. How many type-2 consumers will withdraw at T=2? [3 Points]

Question 3 [16 points]

Suppose an agent has $100. He opens a demand deposit of $100 with a bank which has asset x where x is a random variable and can take the following values:

a) What is the information sensitivity of the demand deposit (i.e. expected loss) of the agent? [2 Points]

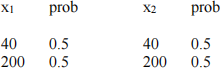

Suppose there are two agents with $100 each. Both of them invest in the same bank and the bank invests in two projects {x1, x2 } where

and the projects (random variables) are statistically independent.

b) What is the information sensitivity of the demand deposit (i.e. expected loss) of an agent where payoffs are shared equally in case of default? [6 Points]

Suppose there are three agents with $100 each. All of them invest in the same bank and the bank invests in three projects {x1, x2, x3 } where

and the projects (random variables) are all statistically independent.

c) What is the information sensitivity of the demand deposit (i.e. expected loss) of an agent where payoffs are shared equally in case of default? Note, the joint distribution of three binary random variables has eight states. [8 Points]

Question 4 [12 points]

Suppose an agent has $100. He opens a demand deposit of $100 with a bank which has asset x where x is a random variable.

a) Suppose x is uniformly distributed on the interval [100, 200]. The density of x is f(x)=1/100 on [100,200] and f(x)=0 otherwise. What is the expected loss of the depositor? [2 Points]

b) Suppose changes in the economy changes the distribution of x. Now x is uniformly distributed on the interval [60, 200]. The density of x is f(x)=1/140 on [60, 200] and f(x)=0 otherwise. What is the expected loss of the depositor? [3 Points]

c) Suppose x is uniformly distributed on the interval [0, 200]. The density of x is f(x)=1/200 on [0, 200] and f(x)=0 otherwise. Calculate the expected loss of the depositor. [3 Points]

d) Suppose x is uniformly distributed on the interval [0, 200]. Given the macroeconomic environment, the government introduces deposit insurance. There is deposit insurance of an amount I=90. Calculate the expected loss of the depositor. [4 Points]

2025-08-15