EFIMM0122 International Financial Reporting 2021

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

EXAMINATION FOR DEGREES IN THE SCHOOL OF ACCOUNTING & FINANCE

January 2021

EFIMM0122

International Financial Reporting

Question 1

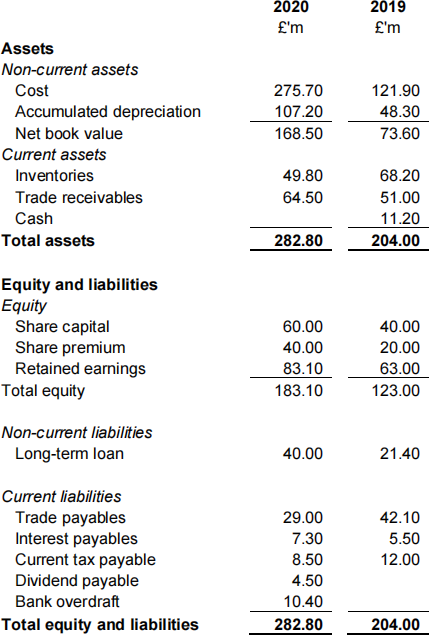

Pharmascience Ltd is a specialty consumer health company in the UK. In early 2020, Pharmascience Ltd launched a project to develop and produce a new range of home fitness equipment which has required significant investment in non-current assets.

The Statements of Financial Position for Pharmascience as at 31 December 2020 and 2019 are shown below:

Notes:

1) A dividend of £4.5m was approved and declared in December 2020. This dividend will be paid in March 2021.

2) During 2020, Pharmascience Ltd disposed of non-current assets costing £25m with an accumulated depreciation of £7.7m. These assets were sold for £20m. There were no other disposals during 2020.

3) Pharmascience’s Income Statement for the year ended 31 December 2020 showed a finance cost of £8m and corporation tax on profits for 2020 was £6m.

REQUIRED

a. Prepare a Statement of Cash Flows in accordance with IAS 7 – Statement of Cash

(14 marks)

b. The directors of Pharmascience Ltd are surprised at the movement on cash for the year given the profits that were recorded. Explain:

a) why differences arise between cash flows and profits

b) the main differences between profit and cash flows in Pharmascience’s accounts in 2020

c) your assessment of Pharmascience’s cash flow and prediction for future profitability

c. Explain why profit is useful for measuring performance but cash is the ‘lifeblood’ of a business.

(3 marks)

Total 25 marks

Question 2

Answer both parts 1 and 2.

Part 1

Digital Vision Ltd designs and develops corporate websites and also provides website maintenance and update services. Digital Vision agreed a contract with a new media company to design their website and provide a maintenance and update service for a 36- month period after the launch of the website for a total price of £5,400. The website was launched on 1 September 2020 and the client paid in full on that date. The website design would normally have cost £3,000 and a 36-month website maintenance service would normally be sold for £100 per month.

REQUIRED

a. Explain the concept of ‘performance obligation’ under IFRS 15 Revenue from Contracts with Customers using the Digital Vision contract as an example. Also explain the criteria for the satisfaction of performance obligations over time and at a point in time with reference to Digital Design.

(7 marks)

b. Explain steps 4 and 5 of the five-step approach to revenue recognition under IFRS 15 with reference to the Digital Vision contract and show how the contract should be accounted for in Digital Design’s financial statements for the year ended 31 December 2020.

(7 Marks)

Part 2

The IFRS Conceptual Frameworks have seen a changing emphasis on the, at times, controversial concept of prudence.

“It may seem obvious that prudence is a desirable thing when preparing financial information; after all, would you wish for imprudent accounting?” (Cooper, 2015, p1)

REQUIRED

Explain the concept of prudence and its changing emphasis in the IFRS Conceptual Frameworks. As part of your answer explain, with examples, how some applications of prudence could lead to creative accounting and hidden reserves.

(11 Marks)

Total 25 marks

Question 3

Answer both parts 1 and 2.

Part 1

Connemara Ltd expanded its business on 1 January 2020 with a new production line. The new production line required additional machinery with a cost of £543,600. Connemara has limited access to loan financing and so obtained the necessary machinery through a leasing agreement from their regular equipment supplier. The lease agreement required four annual payments in advance of £150,000 the first commencing on 1 January 2020. The plant would have a useful life of four years with no residual value at the end of this life. Connemara depreciates plant and machinery on a straight-line basis. Connemara’s accounting year runs to 31st December.

REQUIRED

Show how the leasing of the asset will be presented each year in the financial statements of Connemara Ltd in accordance with IFRS 16 Leases

(12 Marks)

“The spectacular rise and fall of Enron Corp. offers a vivid illustration of how companies can use the legal form of transactions to obscure the economic substance underlying those transactions………….It is the argument of this paper that had the concept of substance over form been applied at Enron, investors and creditors would have been provided with a more realistic view of the company’s financial position and its results of operations, potentially avoiding what became the one of the largest corporate bankruptcies in US history.” (Baker and Hayes, 2004, p767)

REQUIRED

a. the concept of substance over form;

b. how leases have been used as a form of off-balance sheet financing and how IFRS 16 serves to combat this; and

c. reasons why scandals such as Enron might occur and the impacts of these scandals.

(13 Marks)

Total 25 marks

Question 4

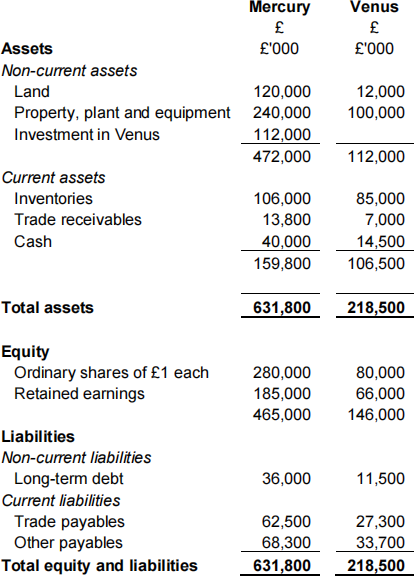

Mercury purchased 60 million shares in Venus on 1 July 2019. On that date, the retained earnings of Venus were £27,500,000. Venus has not issued any new shares since the acquisition. On 1 July 2019, the fair value of Venus’ land was calculated to be £15,000,000 and the carrying value of this land on Venus’s accounts was £12,000,000. The land has not subsequently been revalued in the financial statements of Venus and land is not depreciated. There were no other differences between the book value and the fair value of the assets and liabilities of Venus at the date of acquisition.

The Statements of Financial Position of Mercury and Venus as at 30 September 2020 are as follows:

![]()

Notes:

1) During the year ended 30 September 2020, Mercury sold 30 million units of product to Venus at £2 per unit. The total cost of the 30 million units was £45,000,000. Of these items, 20 million units have been sold onwards to customers outside of the Group during the year and the remaining units were still in the inventories of Venus at year end.

2) On 30 September 2020, Mercury had a trade receivables balance of £2,600,000 due from Venus. On 28 September 2020, Venus sent a cheque for £1,500,000 to Mercury that was not received until 2 October 2020.

3) The management of Mercury estimated that the fair value of goodwill in Venus at 30 September 2020 was £28,000,000.

4) It is the group policy to value non-controlling interest using the proportionate share of net assets method.

REQUIRED

a. Prepare the Mercury Group Consolidated Statement of Financial Position as at 30 September 2020

b. During the Annual General Meeting (AGM), a group of Mercury’s shareholders expressed concern regarding the amount of consideration paid by Mercury for the acquisition of its share in Venus. They claimed that ‘Mercury acquired part of Venus, but the amount paid is higher than the acquired share of Venus’ net assets on the balance sheet at acquisition’ . The shareholders have asked the management of Mercury to explain the rationale for the amount paid. Write a response to the concern raised by the shareholders, including a discussion on the appropriateness of the balance sheet for measuring company value, an explanation of the concept of goodwill, and using the figures from the question to illustrate your points.

c. Explain the difference between valuing a non-controlling interest at the proportionate share of net assets and at fair value and the impact on goodwill.

(3 marks)

Total 25 marks

Question 5

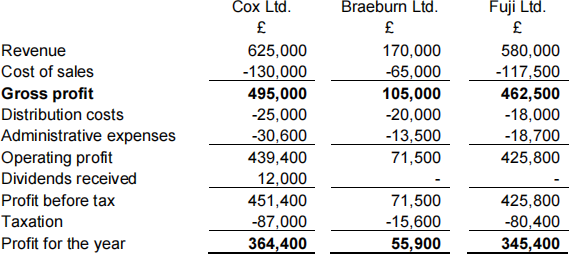

On 1st April 2019, Cox Ltd acquired 120,000 shares in Braeburn Ltd from a total share capital of £150,000 (£1 shares). On 1st January 2020, Cox Ltd also acquired 40% of the shares of Fuji Ltd.

The Statements of Profit or Loss for the year to 31 March 2020 for the three companies are shown below:

1) In February 2020, Braeburn Ltd sold goods to Cox Ltd for £20,000. The sales were made at a profit margin of 25%. At the year-end, 40% of these goods remain in the inventories of Cox Ltd.

2) The income and expenses of Fuji Ltd can be assumed to accrue evenly over the year to 31st March 2020.

3) Braeburn Ltd paid dividends of £10,000 during the year to its shareholders. No other dividends were paid within the group.

4) On 31st March 2020, Braeburn Ltd revalued its non-current assets upwards by £35,000. It is the Cox Group’s policy to revalue group assets.

REQUIRED

a. Prepare the Consolidated Statement of Comprehensive Income for the Cox Group for the year ended 31 March 2020.

(11 marks)

b. Cox Ltd’s accountants have become worried that one of their fruit-selling shops needs to be impaired on the accounts. Cox classifies their shops as separate cash generating units. Explain what a cash generating unit is, the process for determining if there has been an impairment, and any difficulties that may arise in estimating the possible impairment. Provide specific examples of possible indicators of impairment for a fruit-selling shop.

(11 marks)

c. Explain the accounting rationale for the depreciation of non-current assets.

(3 marks)

Total 25 marks

Question 6

Brennan et al (2009) indicated that their review of corporate narrative disclosures suggested that

‘impression management is pervasive in corporate financial communications using multiple impression management methods, such that positive information is exaggerated, while negative information is either ignored or is underplayed’ (p789)

In his review of sustainability reports prepared using Global Reporting Initiative (GRI) standards, Boiral (2013) found that

‘A total of 90 per cent of the significant negative events were not reported, contrary to the principles of balance, completeness and transparency of GRI reports.’ (p1036)

REQUIRED

a. Explain the concept of impression management including examples of impression management techniques as discussed by Brennan et al (2009)

b. In relation to sustainability reporting:

a. Explain the Reporting Principles for Defining Report Quality in the most recent GRI Standards.

b. Discuss examples of the types of information that may be provided in sustainability reports prepared in accordance with the GRI Standards, how impression management methods might be used in presenting this information, and how this presentation could conflict with the principles for report quality described in part a.

(17 marks) Total 25 marks

2022-01-08