ECO00032M Investment and Portfolio Management 2019

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECO00032M

MSc Degree Examinations 2019

DEPARTMENT OF ECONOMICS & RELATED STUDIES

Investment and Portfolio Management

Answer any THREE questions

1. You manage a risky portfolio with expected rate of return of 20% and standard deviation of 36%. The riskless T一bill rate is 5%.

(a) [20 marks] You client chooses to invest 60% of a portfolio in your fund and 40% in T一bills.

What is the expected value and standard deviation of the rate of return on her portfolio? Answer:

E(r) = (0:6 × 20%) + (0:4 × 5%) = 14%

Std. dev. = 0:6 × 36% = 21:6%

(b) [20 marks] What are the reward-to-volatility ratios (S) of your and your clientís risky portfolios? Answer: Your reward-to-volatility ratio:

S = 0:20(0)一:36(0) :05 = 0:4167

Your clients:

S = ![]() 2(一)

2(一)![]() = 0:4167

= 0:4167

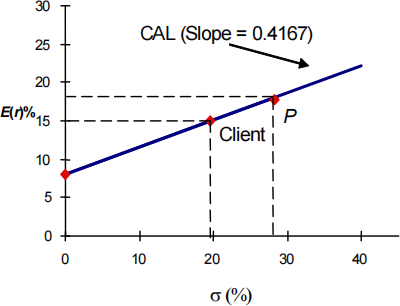

(c) [20 marks] Draw the Capital Allocation Line (CAL) of your portfolio on an expected return-standard deviation diagram. What is the slope of the CAL? Show the position of your

client on your fundís CAL.

Answer:

(d) [20 marks] If your clientís degree of risk aversion is A = 1:6 (assume a quadratic utility function):

● What proportion y of the total investment should be invested in your fund?

● What is the expected value and standard deviation of the rate of return on your clientís optimized portfolio?

Answer:

y* =

1 一 y* =

![]() E(rp ) 一 rf 0:2 一 0:05 0:15

E(rp ) 一 rf 0:2 一 0:05 0:15

A7p(2) 1:6 × 0:362 0:20736

0:2766

Therefore, the clientís optimal proportions are: 72:34% invested in the risky portfolio and 27:66% invested in T一bills.

E(rc ) = 0:05 + 0:15 × y* = 0:05 + (0:7234 × 0:15) = 0:1585 or 15:85% 7c = 0:7234 × 36 = 26:04%

(e) [20 marks] During a particular year, the T一bill rate was 5%, the market return was 17:5% and a your portfolio with beta of 2:0 realized a return of 30%.

● Evaluate your performance based on the portfolio alpha.

● Reconsider your evaluation of your portfolio performance in view of the

Black-Jensen-Scholes Önding that the security market line is too áat? Now, how do you assess your portfolio performance relative to a well-diversiÖed portfolio with a similar risk characteristic?

Answer: Your portfolioís alpha is:

a = 30% 一 [5% + 2:0 × (17:5% 一 5%)] = 0

From Black-Jensen-Scholes and others, we know that, on average, portfolios with low beta have historically had positive alphas. (The slope of the empirical security market line is shallower than predicted by the CAPM.) Therefore, given your portfolioís beta, performance might actually be subpar despite the estimated alpha of zero.

2. Suppose that the index model for stocks A and B is estimated from excess returns with the following results:

RA = 3% + 0:85RM + eA

RB = 一2% + 1:3RM + eB

and where RM is the excess return on the stock market index with standard deviation 7M = 25%.

The regression coe¢ cients of determinations are: adjusted R一squaredA = 0:17, adjusted R一squaredB = 0:11:

(a) [20 marks] What is the standard deviation of the return of each stock?

Answer: The standard deviation of each stock can be derived from the following equation for R2 :

Ri(2) = ![]() =

= ![]()

Therefore, for stock A:

7 A(2) = ![]() =

= ![]() = 0:2656

= 0:2656

7A = 51:54%

For stock B :

7 B(2) = ![]() =

= ![]() = 0:9602

= 0:9602

7B = 97:99%

(b) [20 marks] Break down the variance of each stock to the systematic and Örm-speciÖc

components.

Answer: The systematic risk for A is:

β A(2)7 M(2) = 0:852 × 0:252 = 0:0452

The Örm-speciÖc risk of A (the residual variance) is the di§erence between Aís total risk and its systematic risk:

7 (e)A(2) = 0:2656 一 0:0452 = 0:2204

The systematic risk for B is:

β B(2)7 M(2) = 1:32 × 0:252 = 0:1056

B ís Örm-speciÖc risk (residual variance) is:

7 (e)B(2) = 0:9602 一 0:1056 = 0:8546

(c) [20 marks] Assume that the non-systematic risk is purely Örm speciÖc, i.e. the residuals are uncorrelated. What are the covariance and correlation coe¢ cients between the two stocks?

Answer: The covariance between the returns of A and B is (since the residuals are assumed to be uncorrelated):

Cov(rA ;rB ) = βA β B 7 M(2) = 0:85 × 1:30 × 0:0625 = 0:0690

The correlation coe¢ cient between the returns of A and B is:

![]() Cov(rA ;rB ) 0:0690

Cov(rA ;rB ) 0:0690

7A 7B 0:5153 × 0:9799

(d) [20 marks] What is the covariance between each stock and the market index? Answer:

Cov(rA ;rM ) = β A 7 M(2) = 0:85 × 0:0625 = 0:0531

Cov(rB ;rM ) = β B 7 M(2) = 1:30 × 0:0625 = 0:0812

(e) [20 marks] What is the covariance between the market index and the portfolio consisting in 60% of stock A and 40% of stock B ?

Answer:

Cov(rP ;rM ) = Cov(0:6rA + 0:4rB ;rM ) = 0:6 × Cov(rA ;rM ) + 0:4 × Cov(rB ;rM ) = (0:6 × 0:0531) + (0:4 × 0:0812) = 0:064

3. The Digital Electronic Quant System (DEQS) Corporation pays no cash dividends currently and is not expected to for the next 5 years. Its latest earnings per share (EPS) was $10, all of which was reinvested in the company. The Örmís expected return on equity (ROE) for the next 5 years is 20% per year, and during this time it is expected to continue to reinvest all of its earnings. Starting 6 years from now the Örmís ROE on new investments is expected to fall to 15% and the company is expected to start paying out 40% of its earnings in cash dividends, which it will continue to do forever after. DEQSís market capitalization rate is 15% per year.

![]()

![]()

(a) [30 marks] What is your estimate of DEQSís intrinsic value per share?

Answer: The year一6 earnings estimate is based on growth rate:

g2 = 0:15 × (1 一 :0:40) = 0:09:

Time 0 1 5 6

|

Et |

$10:000 |

$12:000 |

$24:883 |

$27:123 |

|

Dt |

$0:000 |

$0:000 |

$0:000 |

$10:849 |

|

b |

1:0 |

1:0 |

1:0 |

0:6 |

|

g |

20% |

20% |

20% |

9% |

V5 = k D一6g2 = 0: 15($1)0:一0:(85)09 = $180:82

ψ

V0 = ![]() =

= ![]() = $89:90

= $89:90

(b) [30 marks] Assuming its current market price is equal to its intrinsic value, what do you expect to happen to its price over the next two years?

Answer: The price should rise by 15% per year until year 6: because there is no dividend, the entire return must be in capital gains.

V1 = V0 × 1:15 = 103:39

V2 = V0 × 1:152 = 118:89

(c) [20 marks] What e§ect would it have on your estimate of DEQSís intrinsic value if you expected DEQS to pay out only 20% of earnings starting in year 6?

Answer: The payout ratio would have no e§ect on intrinsic value because ROE = k .

(d) [20 marks] In what circumstances would you choose to use a free cash áow model rather than a dividend discount model to value a Örm? In what circumstances would you choose a dividend discount model?

Answer: Theoretically, dividend discount models can be used to value the stock of rapidly growing companies that do not currently pay dividends; in this scenario, we would be valuing expected dividends in the relatively more distant future. However, as a practical matter, such estimates of payments to be made in the more distant future are notoriously inaccurate, rendering dividend discount models problematic for valuation of such companies; free cash áow models are more likely to be appropriate. At the other extreme, one would be more likely to choose a dividend discount model to value a mature Örm paying a relatively stable dividend.

4. Consider the following table, which gives a security analystís expected return on two stocks for two particular market returns:

Probability Market return Aggressive Stock Defensive Stock

50%

50%

25%

5%

38%

一2%

12%

6%

(a) [20 marks] What are the betas of the two stocks?

Answer: Call the aggressive stock A and the defensive stock D. Beta is the sensitivity of the stockís return to the market return, i.e., the change in the stock return per unit change in the market return. Therefore, we compute each stockís beta by calculating the di§erence in its return across the two scenarios divided by the di§erence in the market return:

β A = 一0![]() 一一

一一![]() = 2:00

= 2:00

β D = ![]() 一(一)

一(一) ![]() = 0:30

= 0:30

(b) [20 marks] What is the expected rate of return on each stock if the market return is equally likely to be 5% or 25%?

Answer: With the two scenarios equally likely, the expected return is an average of the two possible outcomes:

E(rA ) = 0:5 × (一0:02 + 0:38) = 0:18 = 18%

E(rD ) = 0:5 × (0:06 + 0:12) = 0:09 = 9%

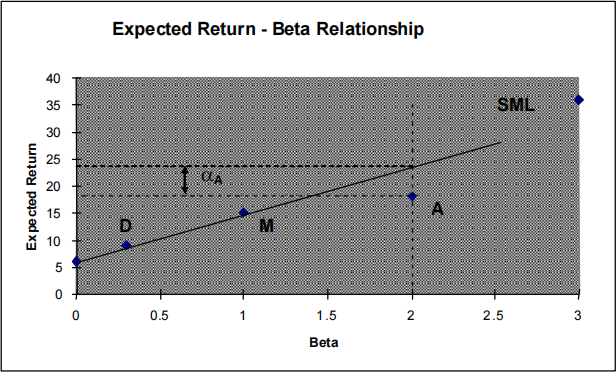

(c) [20 marks] If the T一bill rate is 6% and the market return is equally likely to be 5% or 25%, draw the Security Market Line (SML) for this economy.

Answer: The SML is determined by the market expected return of [0:5 × (:25 + :05)] = 15%, with β M = 1, and rf = 6% (which has βf = 0). See the following graph:

E(r) = :06 + β × (:15 一 :06)

(d) [20 marks] Plot the two securities on the SML graph. What are the alphas of each? Answer: Based on its risk, the aggressive stock has a required expected return of:

E(rA ) = :06 + 2:0 × (:15 一 :06) = :24 = 24% The analystís forecast of expected return is only 18%. Thus the stockís alpha is:

aA = actually expected return 一 required return (given risk)

= 18% 一 24% = 一6%

Similarly, the required return for the defensive stock is:

E(rD ) = :06 + 0:3 × (:15 一 :06) = 0:087

The analystís forecast of expected return for D is 9%, and hence, the stock has a positive alpha:

aD = actually expected return 一 required return (given risk)

= 9% 一 8:7% = 0:3%

The points for each stock plot on the graph as indicated above.

(e) [20 marks] What hurdle rate should be used to assess proÖtability of a project with the risk

characteristics of the defensive Örmís stock?

Answer: The hurdle rate is determined by the project beta (0:3), not the Örmís beta. The correct discount rate is 8:7%, the fair rate of return for stock D .

5. Investors expect the market rate of return in the coming year to be 12%. The T一bill rate is 4%. Changing Fortunes Industriesístock has a beta of 0:5. The market value of its outstanding equity is $100 million.

(a) [20 marks] What is your best guess currently as to the expected rate of return on Changing Fortunesístock? You believe that the stock is fairly priced.

Answer: E(rM ) = 12%, rf = 4%, and β = 0:5. Therefore, the expected rate of return is: 4% + 0:5 × (12% 一 4%) = 8%

If the stock is fairly priced, then E(r) = 8%.

(b) [20 marks] If the market return in the coming year actually turns out to be 10%, what is your best guess as to the rate of return that will be earned on Changing Fortunesístock?

Answer: If rM falls short of your expectation by 2% (that is, 10% 一 12%) then you would expect the return for Changing Fortunes Industries to fall short of your original expectation by:

β × 2% = 1%

Therefore, you would forecast a revised expectation for Changing Fortunes of: 8% 一 1% = 7%

(c) [20 marks] Suppose now that Changing Fortunes wins a major lawsuit during the year. The settlement is 5$ million. Changing Fortunesístock return during the year turns out to be 10%. What is your best guess as to the settlement the market previously expected Changing Fortunes to receive from the lawsuit? (Continue to assume that the market return in the year turned out to be 10%.) The magnitude of the settlement is the only unexpected Örm-speciÖc event during the year.

Answer: Given a market return of 10%, you would forecast a return for Changing Fortunes of 7%. The actual return is 10%. Therefore, the surprise due to Örm-speciÖc factors is

10% 一 7% = 3%, which we attribute to the settlement. Because the Örm is initially worth $100 million, the surprise amount of the settlement is 3% of $100 million, or $3 million, implying that the prior expectation for the settlement was only $2 million.

(d) [20 marks] If you believe that the U.S. dollar will depreciate more dramatically than do other investors, what will be your stance on investments in U.S. auto producers?

Answer: A depreciating dollar makes imported cars more expensive and American cars less expensive to foreign consumers. This should beneÖt the U.S. auto industry.

(e) [20 marks] Here are four industries and four forecasts for the macroeconomy. Match the industry

to the scenario in which it is likely to be the best performer.

Industry Economic Forecast a. Housing construction (i) Deep recession: falling ináation, interest rate and GDP

b. Health care

c. Gold mining

(ii) Superheated economy: rapidly raising GDP, increasing ináation and interest rates

(iii) Healthy expansion: rising GDP, mild ináation, low unemployment

d. Steel production (iv) Stagáation: falling GDP, high ináation

Answer:

Industry Economic Forecast

|

a. |

Housing construction (cyclical but interest-rate |

sensitive) |

(iii) Healthy expansion |

|

b. |

Health care (a noncyclical industry) |

|

(i) Deep recession |

|

c. |

Gold mining (counter-cyclical) |

|

(iv) Stagáation |

|

d. |

Steel production (cyclical industry) |

|

(ii) Superheated economy |

2022-01-08