EFIMM0091 QUANTITATIVE METHODS FOR ACCOUNTING AND FINANCE 2020

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

EFIMM0091

QUANTITATIVE METHODS FOR ACCOUNTING AND FINANCE

Question 1 (50 marks)

Barton and Waymire (2004, JAE) examine whether availability of higher quality financial information lessens investor losses during the October 1929 market crash. They estimate the following cross-sectional model:

![]()

![]()

![]()

![]()

![]()

![]()

![]()

where ![]()

![]()

![]()

![]()

![]()

![]()

![]() is the October 1929 stock return of firm i,

is the October 1929 stock return of firm i, ![]()

![]()

![]()

![]() is the proxy for financial reporting quality (it is a continuous variable),

is the proxy for financial reporting quality (it is a continuous variable), ![]()

![]()

![]()

![]() is a vector capturing noise in fundamental values,

is a vector capturing noise in fundamental values, ![]()

![]()

![]()

![]()

![]() is a vector of other variables potentially associated with stock returns, and

is a vector of other variables potentially associated with stock returns, and ![]()

![]() is an error term.

is an error term.

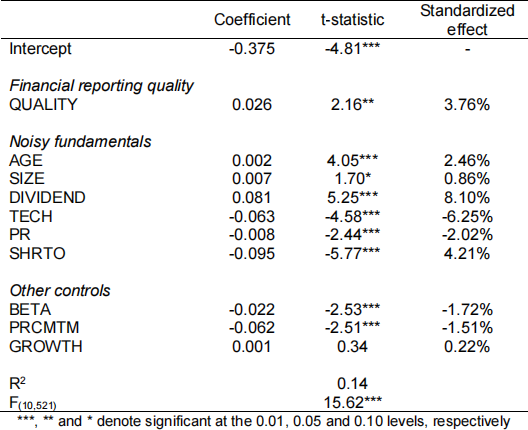

a) The following table shows the results. Evaluate the statistical and economic significance of the main explanatory variable, ![]()

![]()

![]()

![]() (10 marks).

(10 marks).

b) Which is the most important explanatory variable among the “Noisy fundamentals” variables? Explain which are the relevant coefficients you would compare to answer this question (10 marks).

c) Can you reject the null hypothesis that all the independent variables are jointly equal to zero? (10 marks).

d) The authors are worried that SIZE might have been wrongly included in the model. Explain how this can affect the OLS estimators (10 marks).

e) Explain the interpretation of the R2. How would the R2 change if we re-run the regression excluding the variable SIZE (10 marks).

Question 2 (50 marks)

Suppose you have monthly data of The Coca-Cola Company sales for the period January 1990 to December 2018.

a) Explain the nature of data (unit of analysis/frequency of data) (5 marks).

b) Explain the concept of Trend and Seasonality and whether you would expect to find these issues in the data (15 marks).

c) How can you formally test for Seasonality (15 marks)?

d) You plot Coca-Cola sales against time and find that sales have been growing over time. Would you incorporate this feature of the data when modelling this variable? How can you do that in a regression equation? (15 marks)

Question 3 (50 marks)

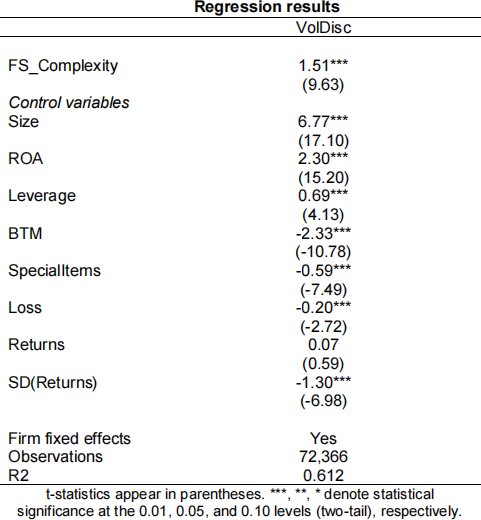

In a recent paper published in the Journal of Accounting and Economics titled “Guiding through the Fog: Financial statement complexity and voluntary disclosure,” Guay, Samuels, and Taylor examine whether managers use voluntary disclosure (VolDisc) to mitigate the negative effects of complex financial statements (FS_Complexity). Both VolDisc and FS_Complexity are continuous variables.

a) The null hypothesis is that managers do not use voluntary disclosure to mitigate the effects of complex financial statements. Based on the (fixed effects) regression results presented below, can you reject the null hypothesis? Explain your conclusions based on both, economic and statistical significance (10 marks).

b) Some other papers find that firm industry affiliation is a determinant of voluntary disclosure. Would you include Industry fixed effects in the previous regression to control for this? (10 marks)

c) The authors have excluded from the regression the number of analysts following the firm (the literature generally agrees that the higher the number of analysts the better the information environment). This variable which might be correlated with FS_Complexity and VolDisc. Do you expect this to affect the OLS estimators? If so, explain the potential consequences (10 marks).

d) The authors want to estimate the relationship between the probability of voluntarily disclosing information and FS_Complexity. They have created a dummy variable equal to

1 if the company voluntarily discloses information in a given quarter, and 0, otherwise.

i. What is the regression equation that the authors are estimating in this case? (4 marks).

ii. Which models are suitable for estimating this specification? Discuss the advantages and disadvantages of each of them (8 marks).

iii. What is the interpretation of the coefficient of interest in this specification? (8 marks).

2022-01-05