ECO00007M Continuous-Time Finance and Derivative Assets

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECO00007M

MSc Examinations 2020-21

Continuous-Time Finance and Derivative Assets

Question 1

a)

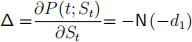

(i) Prove that the Delta of a European put option is:

where P(t;St) is the price of a European put option with strike price K and time of maturity T and is given by the formula

where N(.) is the cumulative standard normal distribution and

St is the current price of the underlying asset which follows a Geometric Brownian motion process

r is the risk free interest rate and σ is the volatility.

(Confine your answer within 200 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[13 marks]

(ii) Derive the general expression for the forward price using a no arbitrage argument and describe the main differences between forward contracts and futures.

(Confine your answer within 400 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[12 marks]

![]() b)

b)

(i) Given that the stochastic process Xt satisfies the following equation:

find the explicit functional form of Xt .

(Confine your answer within 300 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

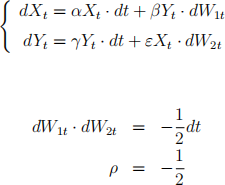

(ii) Suppose that Xt and Yt follow the system of processes:

where W1t and W2t are Wiener shocks, dW1t ∼ N (0,dt) and dW2t ∼ N (0,dt), ρ is the coefficient of linear correlation

and Zt is defined as

Find dZt .

(Confine your answer within 300 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[15 marks]

[TOTAL 50 marks]

Question 2

a)

(i) Discuss the main assumptions of the Black and Scholes model with a detailed discussion about the distribution of the underlying asset.

(Confine your answer within 300 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

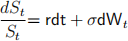

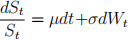

(ii) Consider St as the current price of the underlying asset which follows a Geometric Brownian motion process

where µ is the drift and σ is the volatility. Express  as a function of the risk free interest rate r and the risk premium with a detailed discussion about the risk neutralization and the interpretation of the risk premium.

as a function of the risk free interest rate r and the risk premium with a detailed discussion about the risk neutralization and the interpretation of the risk premium.

(Confine your answer within 150 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

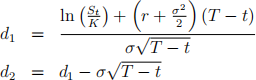

(iii) Applying the Black and Scholes model, show that the price of a European put option with strike price K and time of maturity T is given by the formula

where

and N(.) is the cumulative standard normal distribution.

(Confine your answer within 150 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

b)

(i) How would the payoff of a call option change if the price of the underlying asset at maturity T, ST reached a very low level never seen before? Provide some intuition for this result.

(Confine your answer within 150 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

(ii) Is the Black and Scholes model for option pricing adequate to represent financial market stress? After motivating your answer, suggest possible alternative models.

(Confine your answer within 450 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

[TOTAL 50 marks]

Question 3

a)

(i) Derive the distribution of the squared infinitesimal increment of Wt ,

by dividing the interval [0,t] into n equally large subintervals whose length is ![]() , and defining the quadratic variation of the Wiener process as Sn .

, and defining the quadratic variation of the Wiener process as Sn .

(Confine your answer within 150 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

(ii) Using a no-arbitrage argument, show the expression for the futures price in the case of consumption commodities and explain the main characteristics of this type of commodities.

(Confine your answer within 250 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

b)

(i) Using a no arbitrage argument, prove the parity condition between European call and put options.

(Confine your answer within 250 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

(ii) Describe the Delta Hedging principle using forward contracts. How would your answer change if you had to use options?

(Confine your answer within 300 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

(iii) Why can the Equity be priced as a call option?

(Confine your answer within 250 words. Please note that any mathematical derivation, equations, figures and graphs is not included in the word count.)

[10 marks]

[TOTAL 50 marks]

2021-12-27