ECOM044 Advanced Asset Pricing and Modelling

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECOM044 Advanced Asset Pricing and Modelling

When writing formulas, please note the following:

O It is acceptable to use the standard alphabet rather than greek letters. The following are

recommended: m for µ , s for σ, w for ω , r for ρ , d for ∆ , b for β .

![]() O For mathematical operators: add +, subtract -, multiply *, and divide /. O Where appropriate, use an underscore to indicate a subscript, e.g. r_f for rf . O Use the ^ character for power, e.g. x^2 for x2 , x^0.5 for (x.

O For mathematical operators: add +, subtract -, multiply *, and divide /. O Where appropriate, use an underscore to indicate a subscript, e.g. r_f for rf . O Use the ^ character for power, e.g. x^2 for x2 , x^0.5 for (x.

O As an alternative to x^0.5 you may type sqrt(x).

O Use brackets as necessary. To make your answer clearer use different brackets where appropriate,

e.g. [] {} ().

Question 1 [30 points]

Prove two no-arbitrage restrictions. The proofs should be by contradiction, that is, by assuming that the (in)equality does not hold and showing how you can then construct an arbitrage. All options are written on the same non-dividend paying stock, have the same strike price K, and have the same maturity T. The superscripts AM, EU denote that the corresponding option is American, European [Note: Make sure every step in your proof is justified.]

(a) (20 points)  (i.e., Put-Call Parity w/o dividends), for all 0 < t, where the subscript t denotes the time at which the corresponding option/stock price is quoted.

(i.e., Put-Call Parity w/o dividends), for all 0 < t, where the subscript t denotes the time at which the corresponding option/stock price is quoted.  is the present value operator bringing money risk-free from T to t. Explain how the Put-Call Parity is extended for a dividend paying stock.

is the present value operator bringing money risk-free from T to t. Explain how the Put-Call Parity is extended for a dividend paying stock.

(b) (10 points)  (i.e., early exercise of an American call option is never optimal on a non-dividend paying stock), for all 0 < t, where the subscript t denotes the time at which the corresponding option/stock price is quoted. Explain why the inequality you just proved does not necessarily hold.

(i.e., early exercise of an American call option is never optimal on a non-dividend paying stock), for all 0 < t, where the subscript t denotes the time at which the corresponding option/stock price is quoted. Explain why the inequality you just proved does not necessarily hold.

Question 2 [35 points]

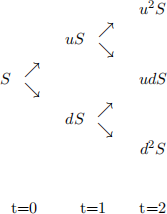

A stock price evolves in a standard binomial tree. Each period it can either go up to u = 1.20 times its previous price or down to d = 0.90 times its previous price. Consider a two period model (t = 0, 1, and 2), as depicted below, where each period corresponds to one year. The risk-free (net) return between t = 0 and t = 1 is r1 = 2.00%, while between t = 1 and t = 2 it is r2 = 3.00%. The initial stock price is S = 100 and the stock pays no dividends.

(a) (10 points) Price an American and a European Call option on the stock with strike price K = 119

and maturity at t = 2.

(b) (5 points) Price an American and a European Put option on the stock with strike price K = 119 and

maturity at t = 2.

(c) (5 points) Verify that Put-Call Parity holds for the European options at t = 0 and at both nodes at t = 1. Check whether it holds for the American options.

(d) (10 points) Price an exotic Put option with maturity at t = 2 (and no early exercise allowed) and with a strike price equal to the maximum stock price up to that point, that is, K = max}S, S1 , S2 ,, where S1 is the stock price at t = 1, and S2 is the stock price at t = 2.

(e) (5 points) Price a derivative with maturity at t = 2, that obliges you to sell the stock at t = 2 (and

not earlier) for price max}S, S1 , S2 ,, where S1 is the stock price at t = 1, and S2 is the stock price at t = 2.

![]()

Question 3 [35 points]Let dBt = rBtdt (B0 = 1) be a bond in dollars, that is, $1 now (time 0) is going

to be $exp(rt) at time t > 0, where r is a known constant. And let dDt = uDtdt (D0 = 1) be its sterling counterpart, that is, f1 now (time 0) is going to be fexp(ut) at time t > 0, where u is a known constant. Also, let the exchange rate follow the process dCt = µCtdt + σCtdWt (C0 > 0), where µ, σ are known constants, and W is standard Brownian Motion under the physical measure. Hence, Ct is the amount of dollars you have to pay to buy one sterling at time t.

(a) (5 points) Let St = CtDt. What does St represent?

(b) (10 points) What are the dynamics of St (i.e., dSt) and the dynamics of St/Bt (i.e., d (St/Bt)), under

the physical measure?

(c) (10 points) What are the dynamics of Ct (i.e., dCt) under the risk-neutral measure Q that guarantees that St/Bt is a martingale under Q. (Hint: You can blindly apply Girsanov’s theorem to change measure.)

(d) (10 points) Let FT be the forward price agreed now (at time 0) to be paid in dollars for one sterling delivered at T > 0 (this is a standard forward contract, no money changes hands at the agreement date). Use risk-neutral pricing under Q from (c), to relate FT to C0 .

2021-12-14