Econ 518 Quiz 2

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Quiz 2 (Econ 518, 2021 Fall)

1. (15 points) Consider a regression model y = β0 + β1x1 + ··· + βkxk + u. Wooldridge’s Introduc- tory Econometrics, A Modern Approach (7ed, p.173) explains the LM test procedure for q exclusion

restrictions as follows.

Step 1. Regress y on the restricted set of independent variables and save the residuals, ![]() .

.

Step 2. Regress ![]() on all of the independent variables and obtain the R-squared, say, R

on all of the independent variables and obtain the R-squared, say, R![]() (to distinguish it from the R-squared obtained with y as the dependent variable).

(to distinguish it from the R-squared obtained with y as the dependent variable).

Step 3. Compute LM = nR![]() (the sample size times the R-squared obtained from step (2)).

(the sample size times the R-squared obtained from step (2)).

Step 4. Compare LM to the appropriate critical value, c, in a χ![]() q) distribution; if LM > c, the null hypothesis is rejected. Even better, obtain the p-value as the probability that a χ

q) distribution; if LM > c, the null hypothesis is rejected. Even better, obtain the p-value as the probability that a χ![]() q) random variable exceeds the value of the test statistic. If the p-value is less than the desired significance laven, then H0 is rejected. If not, we fail to reject H0 .

q) random variable exceeds the value of the test statistic. If the p-value is less than the desired significance laven, then H0 is rejected. If not, we fail to reject H0 .

Provide a theoretical explanation why (or under what conditions) the LM is what you learned is the LM statistic.

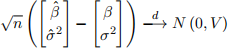

2. (10 points) Consider a linear regression model ln y = x′β + u, u|x ∼ N(0,σ2). You have a random sample {(yi

, xi), i = 1, · · · , n}.Let βˆ and ˆσ2 be the ML estimators for β and σ2

respectively so that  for some V . You want to estimate E[y|x = x0]. Provide a consistent

for some V . You want to estimate E[y|x = x0]. Provide a consistent

estimator for it and a 95% asymptotic confidence interval of it.

2021-12-03