ECON0060: ADVANCED MICROECONOMETRICS SUMMER TERM 2021

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

SUMMER TERM 2021

24-HOUR ONLINE EXAMINATION

ECON0060: ADVANCED MICROECONOMETRICS

PART A

Answer all questions. 50 marks total.

Question 1 (25 marks total)

The following two-equation system of simultaneous equations contains an interaction between an endogenous and an exogenous variable:

y1 = α0 + γ12y2 + γ13y2z1 + α1z1 + α2z2 + ε1

y2 = β0 + γ21y1 + β1z1 + β3z3 + ε2

a. Assume that γ13 = 0 so that the model is a linear simultaneous equations system. Discuss identification of the parameters in each equation under this assumption. Which parameters are identified and why? State any additional assumptions required.

b. Now assume that γ13 is unrestricted. It could be zero or nonzero. Find the reduced form for y1 and y2 in terms of the variables (z1, z2, z3), the error terms (ε1, ε2), and the parameters.

c. Assuming that E (ε1| z) = E (ε2| z) = 0, find E (y1| z).

d. Argue that, under the additional assumptions stated in part a., the parameters of the model are identified regardless of the value of γ13.

e. Suppose that β3 = 0 and γ13 ≠ 0. Can the parameters in the first equation be consistently estimated? How?

Question 2 (25 marks total)

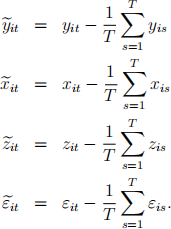

Consider the linear panel data model

yit = αi + βxit + γzit + εit

for i = 1, ..., N and t = 1, ..., T. Assume xit is a k × 1 vector of time-varying variables, zit is a time-varying scalar, αi is a time-constant unobserved effect, and εit is the idiosyncratic error. Assume xit is strictly exogenous with respect to εit. That is, assume

E (x'isεit) = 0 for all s, t = 1, ..., T.

However, xit may be correlated with αi . Further, zis may be correlated with (αi , εit).

a. Suppose that T = 2. Does the ordinary least squares estimator applied to the first differ-enced data provide consistent estimates of β? Does it provide consistent estimates of γ? Explain.

b. Maintaining the assumption that T = 2, propose an instrumental variables estimator for (β, γ). State any additional conditions required. If additional conditions are required, discuss whether those conditions are testable and how you would test them.

c. Now consider the general case where T > 2. Add the assumption that E(zisεit) = 0 for s < t. That is, previous values of zis are uncorrelated with the current value of εit. Explain carefully how you would estimate (β, γ).

d. In the general case with T > 2, consider the model after transformation by the “within transformation”

where

If you use zi,t−k for k ≥ 1 as instruments, does the instrumental variables estimator provide consistent estimates of (β, γ)? Explain.

PART B

Answer all questions. 50 marks total.

Question 3 (25 marks total)

Assume each consumer chooses a mode of transport according to a conditional logit model and that there are J = 3 modes from which to choose. Let di ∈ {1, 2, 3} indicate the mode chosen by consumer i. The probability that consumer i chooses mode j is

where Xi = [xi1, xi2, xi3] is a K × J matrix, xij is a K × 1 vector of observable variables, β is a K × 1 parameter vector, and (α1, α2, α3) are scalar parameters. Assume you observe (di, xi1, xi2, xi3) for i = 1, ..., N.

a. Consider the two parameter vectors (α1, α2, α3, β) and (0, α2 − α1, α3 − α1, β). Show that both imply the same mode-choice probabilities. Is it possible to identify (α1, α2, α3)?

b. Assume α1 = 0. What is the log likelihood function and the score of the log likelihood?

c. Suppose you had data only on the subsample of people with di = 1 or di = 2. Continue to assume α1 = 0. What is the log likelihood for this selected subsample? (Hint: it should be based on Prob (di = j| Xi , j ≤ 2)) Can you consistently estimate β with this selected subsample? Explain.

d. Let  be the estimate of β obtained using the full sample and log likelihood from question b. Let

be the estimate of β obtained using the full sample and log likelihood from question b. Let  be the estimate obtained from the selected subsample and log likelihood in question c. How could you test the hypothesis that the two estimates are the same? If you reject that they are the same, what would you conclude?

be the estimate obtained from the selected subsample and log likelihood in question c. How could you test the hypothesis that the two estimates are the same? If you reject that they are the same, what would you conclude?

Question 4 (25 marks total)

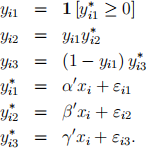

Suppose yi1 = 1 if house i is owner-occupied and yi1 = 0 if it is rented. Let  be the latent variable that determines whether house i is owner-occupied or rented. Assume it is owner-occupied if

be the latent variable that determines whether house i is owner-occupied or rented. Assume it is owner-occupied if  ≥ 0. Let

≥ 0. Let  be the log purchase price of a house which is observed only for owner-occupied houses. Let

be the log purchase price of a house which is observed only for owner-occupied houses. Let  be the log rent for a house which is observed only for rental houses. (, ) are not always observed. Instead you observe (yi1, yi2, yi3) where (yi1, yi2, yi3) are generated from the following Tobit model:

be the log rent for a house which is observed only for rental houses. (, ) are not always observed. Instead you observe (yi1, yi2, yi3) where (yi1, yi2, yi3) are generated from the following Tobit model:

Let εi = (εi1, εi2, εi3) and assume that xi ⊥⊥ εi . Further, assume that εi ∼ N(0, Σ) and that σ11 = Var(εi1) = 1. (α, β, γ) are parameter vectors, and xi is a K dimensional vector of observable explanatory variables. The vector xi includes characteristics of the house such as size, location, number of bedrooms, etc. You have data on (xi , yi1, yi2, yi3) for i = 1, ..., N. In the questions below, σij is the element of the matrix Σ in row i and column j.

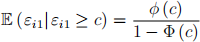

a. What is the probability that house i is rented, conditional on xi? How would you estimate α? State any additional conditions required.

b. What is the expected log house price conditional on a house being owner-occupied? That is, what is E (|yi1 = 1, xi)? What is the expected log house price conditional on a house being rented? Hint: Use the fact that εi1 and εi2 are jointly normal. Further, recall that since εi1 is a standard normal random variable, for any real number c,

where φ (·) and Φ (·) denote the standard normal pdf and cdf, respectively.

c. Solve for the conditional density for yi2 given yi1 = 1 and xi . Solve for the conditional density of yi3 given yi1 = 0 and xi . What is the log likelihood for this model?

Hint: There are two cases to work out: case 1 (yi1 = 1, yi2, yi3 = 0) and case 2 (yi1 = 0, yi2 = 0, yi3). Further, since (εi1, εi2, εi3) are jointly normal, the conditional density of εi2 given εi1 ≥ c is

where f (εi2| εi1; σ22, σ12) is the density of εi2 conditional on εi1. You can use this expression in your answer.

d. Propose two different ways to consistently estimate β and γ. Which provides a more efficient estimator asymptotically?

e. Are the parameters (σ12, σ13, σ23) identified? Discuss.

2024-03-17