EC404 MACROECONOMICS Midterm Test 2021–2022

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

EC404

Midterm Test 2021–2022

MACROECONOMICS

1. Answer all parts of this question.

Consider the neoclassic growth model discussed in the course.

(a) [10 marks] What are the factors that drive output to grow in the neoclassic growth model? List at least 3 factors in the model that contribute to output growth. Briefly explain how they contribute to aggregate output growth. Discuss, sepa- rately for each of them, whether it contributes to output per capita growth.

(b) [10 marks] What are the other factors that are not present in the neoclassic growth model, but important for economic growth in the real world? List at least 2. Briefly explain how they contribute to growth.

2. Answer all parts of this question.

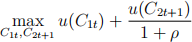

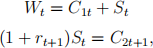

Consider the OLG economy discussed in the lectures. Assume no exogenous techno-logical growth or population growth (g = 0, n = 0). Households maximise

subject to

where u(C) = log C. St denotes savings, ρ > 0 the discount rate, and rt+1 the real rate of return on savings. The production function is Cobb-Douglas: Yt = Kt(α)Lt(1)−α .

Assume full depreciation: δ = 1.

(a) [10 marks] Derive the Euler equation of the household’s problem. Interpret the Euler equation. In particular, explain how consumption growth is related to in- terest rate rt+1 and time discount ρ, and why.

(b) [10 marks] Derive the dynamic equation of capital kt that characterizes the equi- librium. Plot a phase diagram to illustrate how the steady state level of capital k∗ is determined and how capital converges to the steady state level if initial capital k0 < k ∗ .

(c) [10 marks] The economy is at the steady state at time t = 0. Surprisingly, at time t = 1, time discount ρ increases to ρ′ > ρ . How does the steady state changes and how does the economy converges to the new steady state? Use the phase diagram to illustrate.

3. Answer all parts of this question.

Consider the Ramsey growth model analysed in the lectures with modification on labor supply. For simplicity, assume that growth rates of population and technology are both zero, and normalize population N and TFP A both to 1. The representative household supplies labor l (t) at time t. Her instantaneous utility at time t is u(c(t), l (t)) =

ln(c(t) − l (t)2 /2). So the representative household’s lifetime utility is

Production function is Cobb-Douglas: Y (t) = K (t)α L(t)1−α , where L(t) = l (t) * N = l (t). Depreciation rate is δ .

(a) First, assume that labor supply is inelastic,i.e., l (t) = 1 for all t. This setting is similar to the setting in the benchmark neoclassic growth model discussed in the lectures,

i. [10 marks] Solve the household’s problem. Solve for the equations of mo- tion that describe the optimal consumption and savings.

ii. [10 marks] Derive the dynamic equations that characterize the equilibrium.

iii. [10 marks] Plot the phase diagram and use it to illustrate how the steady state is determined and how the economy converges to the steady state. Is the steady state different from that in the benchmark model discussed in the lectures, where labor supply does not enter the utility function,i.e., u(c) = ln(c)? Why?

(b) Now assume that the labor supply is elastic and optimally chosen by the repre- sentative household.

i. [10 marks] Derive the optimality condition forl in the household’s problem. Solve for l as a function of w.

ii. [10 marks] Derive the dynamic equations that characterize the equilibrium.

(Hint: one equation expresses l as a function of k, one equation is related to c, and one is related to k(˙)). What is the marginal productivity of capital at the aggregate level? Does it decrease, increase or stay constant as k increases? Why?

2024-01-30