Time Series Analysis Assignment

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Time Series Analysis

Assignment

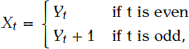

(1) Let

where Yt is stationary time series. Is Xt stationary ?

(2) Suppose that

Xt = (1 + 2t)St + Zt

where St = St−12. Suggest a transform for Xt so that the transformed series is stationary.

(3) Derive ACFs ρk, k = 1, 2, ... for the following models.

(a) Xt = Zt − θ1Zt−1 − θ2Zt−3

(b) Xt − 0.5Xt−1 = Zt, where {Zt} ∼ WN(0, 1).

(4) If the ACF of some stationary time series is

ρ1 = 0.5467, ρ2 = 0.3667, ρ3 = 0.2, ρk = 0,fork ≥ 4

what kind of model you would like to choose for the time series ?

(5)

(a) Suppose R calculations of fitting an AR(2) model to the data are

{\sf

Call: arima(x = x, order = c(2, 0, 0))

Coefficients:

\begint{rrrr}

& ar1 & ar2 & intercept \\

& 1.1503 & -0.8009 & 0.8738\\

s.e. & 0.1250 & 0.1184 & 0.0623

\endt

sigma\^{}2 estimated as 0.03005: log likelihood = 5.38, aic = 1-2.77 }

write down the estimated AR model

(6) Based on the time plot of International Airline Passengers. Answer the following questions.

⊲ (a) Is it stationary ? Justify it .

⊲ (b) What kind of time series components do the data contain ?

⊲ (c) Suggest a transformation so that it may equalize the seasonal vari-ation.

2024-01-17