Derivative Securities Assignment 4

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Business School F421

Derivative Securities

Assignment 4

Problem 1. The stock of GreatSteps Inc. is priced at $82 per share today. No dividend is expected from this company within a few years. Based on the historical data, analysts estimate that the volatility of the stock price is 60% per annum. The interest rate is 3%. A put option on the stock strikes at 80 and matures in exactly seven months from now.

(a) Suppose the put is European. What is the value of the put if you value it in a seven-step binomial model? Display the binomial tree in your answer.

(b) Now, suppose the put is American and value it again using a seven-step binomial model. By how much is the American put value higher than its European version? Indicate the nodes on which the American put will be exercised.

(c) If the volatility jumps instantaneously to 70% per annum today, will the European put value increase or decrease according to your seven-step binomial model? By how much? What if the put is American?

(d) If the European put is quoted for $18.42 in the exchange now, with what volatility will your seven-step binomial model give the option price quoted in the market? (This volatil- ity is called the implied volatility of this put option; it is implied by the premium quoted or traded for in the market.) What if the put is American?

Problem 2. A common stock often pays dividend. Many of them pay dividend regularly. For each dividend payment, three days are important for investors. The first is the “declaration date” — the day the board of directors announces its intention to pay a dividend. On that day, a liability is created and the company records that liability on its books; it now owes the money to the stockholders. The second is “ex-dividend date” — the day on which shares bought and sold no longer come attached with the right to be paid the most recently declared dividend. Existing holders of the stock will receive the dividend even if they sell the stock on or after that date, whereas anyone who bought the stock will not receive the dividend. The third is “record date” — shareholders registered in the company’s record as of the record date will be paid the dividend. Registration is usually automatic for shares purchased before the ex-dividend date.

For pricing options, it is important to pay attention to the ex-dividend date, besides the dividend. It is relatively common for a stock’s price to decrease on the ex-dividend date by an amount roughly equal to the dividend paid. This reflects the decrease in the company’s assets resulting from the payout of the dividend.

Consider an American call option when the stock price is $18, the exercise price is $20, the time to maturity is six months, the volatility is 30% per annum, and the risk-free interest rate is 10% per annum. Two dividends are expected during the life of the option with the ex-dividend dates at the end of two months and five months. Each of the dividends is 40 cents.

(a) Divide the life of the option into six time steps to generate a binomial tree of the “ad- justed” stock price that excludes the value of the expected dividends. Present the bino- mial tree (i.e., the “adjusted” stock prices) in the table displayed below.

(b) Calculate the value of the expected dividend at each time step to generate a six-step bi- nomial tree of the “market” stock price that includes the value of the expected dividends. Display the dividend values and the binomial tree in the above table.

(c) Use the binomial tree of the “market” price to calculate the value of the call option and present the option values in the above table.

(d) Does optimal early exercise happen? In which steps does it happen?

Problem 3. The data file associated with this problem contains daily share price of the British Petroleum (BP), the Salomon Brothers, and the Lehman Brothers in October 1987. BP is a British oil company, traded in the London Stock Exchange. The other two companies are Amer- ican banks that no longer exist but used to be traded in the New York Stock Exchange. Salomon Brothers became part of the Citigroup through a series of mergers and acquisitions. Lehman Brothers filed bankruptcy during the global financial crisis in 2008. The data are the share prices of the three companies around the historical Black Monday, which is October 19, 1987, on which the Dow Jones Industrial Index dropped by 508 points (22.61%).

When estimating volatility in class, we approximate the number of trading days in a year by 250 days. In practice, many people use 252 days, to be more precise. However, if you try to be even more precise in this problem, you may find life interesting.

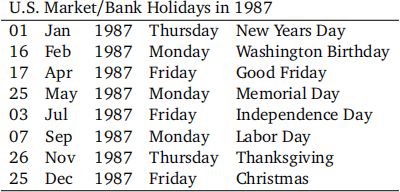

For American companies, we should use the number of the U.S. trading days. The year of 1987 is not a leap year; so it had 365 days. (The year of 1988 is a leap year!) There are 52 weeks in a year, which implies that 104 days are on weekends. In addition, the U.S. had 10 official holidays that fell on weekdays in that year, but the market closed for only seven of them. The market also closed on April 17, which was Good Friday (although not an official U.S. holiday). So, the number of U.S. trading days in 1987 is 365- 104- 8 = 253 days. Clearly, 250 is not a bad approximation. The table below lists the market holidays in the U.S. in 1987.

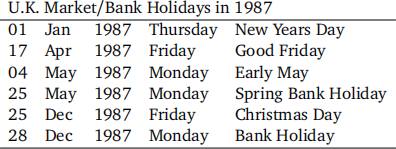

For stocks traded in U.K., we should use U.K. trading days. U.K. had six official holidays falling on weekdays in 1987 to cause bank and market to close. So, the number of trading days in 1987 for U.K. companies is 365 - 104 - 6 = 255 days. The table below lists the market holidays in the U.K. in 1987.

After all, using either 250 or 252 as approximation is fine for this problem. If you are curious, you may want to explore with the above exact the numbers of trading days for U.S. and U.K. in 1987 to see by how much your results change.

(a) Use the provided data to estimate the volatilities of the three share prices.

(b) Use only the data for the second half of October (from the 16th to the 30th) to estimate the three volatilities again. How do the new estimates compare to those obtained in (a), larger or smaller?

Problem 4. Binary options are a category of exotic derivative securities. The two primary types are the cash-or-nothing and the asset-or-nothing options. A cash-or-nothing option pays a fixed amount of cash if the option expires in-the-money. In contrast, an asset-or-nothing option pays an amount equivalent to the price of the underlying security if it expires in-the-money. Both types are typically European-style options.

More specifically, a cash-or-nothing put option on a stock that pays out B dollars upon striking at X and maturing in T years will provide the holder B dollars if ST < X . If not, it pays nothing, where ST denotes the stock price at maturity. In contrast, an asset-or-nothing put option on a stock that strikes at X and matures in T years will award the holder ST dollars if ST < X and nothing otherwise.

Historically, binary options have been traded over-the-counter (OTC), meaning issuers sold contracts directly to buyers. They were also often embedded into more complex contractual agreements. In more recent times, various websites have emerged to offer platforms for the trading and clearing of binary options. However, investors should be aware that the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) have issued joint warnings about potential fraudulent practices in binary options trading.

Given this context, consider a stock of BinBet.com that is currently trading at $51 per share, with an annual volatility of 30%. The prevailing risk-free interest rate is 6%.

(a) Evaluate a cash-or-nothing put option on BinBet.com’s stock that promises a payout of $50 when it strikes at $50 and matures in six months. Use the simulation method with a sample size of 10,000, and display the initial 10 simulations in your answer.

(b) For an asset-or-nothing put option on the stock that strikes at $50 and matures in six months, calculate its value using the simulation method. Select a sample size of 10,000 in the simulation. Present the first 10 simulations in your response.

(c) Regular put options are often referred to as plain-vanilla options. Determine the value of such an option on BinBet.com’s stock that has a strike price of $50 and is set to mature in six months. Base your answer on 10,000 simulations and show the first 10 simulations.

(d) Based on the values you’ve obtained for the above three options, can you discern any relationship among them? Can you explain the reason for the relationship?

2023-10-30