ACC307 ADVANCED TAXATION

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ACC307

1st Semester 2023/24 Assignment

BA ACCOUNTING - Year 4

ADVANCED TAXATION

Deadline: 3pm 20 October 2023

Question 1

Paul is employed by Kune plc and he is trying to prepare his own income tax computation for the tax year 2022/23. The following information is available in respect of the tax year 2022/23:

(1) Salary and PAYE

Paul was paid a gross annual salary of £41,030, while PAYE of £19,130 was deducted at source in the tax year 2022/23.

(2) Car and fuel benefits

Throughout the tax year 2022/23, Kune plc provided Paul with a petrol car which has a list price of £17,900. The car cost Kune plc £17,200, and it has a CO2 emission rate of 109 grams per kilometre. During the tax year 2022/23, Paul made contributions of £1,200 to Kune plc for the use of the car.

During the period 1 July 2022 to 5 April 2023, Kune plc also provided Paul with fuel for private journeys. The total cost of fuel during this period was £4,200, of which 45% was for private journeys. Paul did not make any contributions towards the cost of the fuel.

(3) Living accommodation

Throughout the tax year 2022/23, Kune plc provided Paul with living accommodation. The property has been rented by Kune plc since 6 April 2022 at a cost of £1,100 per month. On 6 April 2022, the market value of the property was £122,000, and it has an annual value of £8,600.

On 6 April 2022, Kune plc purchased furniture for the property at a cost of £12,000. The company pays for the running costs relating to the property, and for the tax year 2022/23 these amounted to £3,700.

(4) Property income

Paul owns a freehold shop, which islet out unfurnished. The ten year old shop was purchased by Paul on 1 October 2022. Paul spent £8,400 replacing the bXilding¶s roof: the shop Zas not Xsable Xntil this Zork Zas completed on 30 November 2022, and this fact was represented by a reduced purchase price.

On 1 December 2022, the property was let to a tenant, with Paul receiving a premium of £12,000 for the grant of a 30-year lease. The monthly rent is £664 payable in advance, and during the period 1 December 2022 to 5 April 2023 Paul received five rental payments.

Due to a fire, £8,600 was spent on repairing the ceiling of the shop during February 2023. Onl\ E8,200 of this Zas paid for b\ PaXl¶s propert\ insXrance.

Paul paid insurance of £501 in respect of the property. This was paid on 1 October 2022 and is for the year ended 30 September 2023.

(5) Pension

Kune plc has contributed £30,000 into the compan\¶s occXpational pension scheme on PaXl¶s behalf eYer\ \ear. PaXl has neYer personall\ made an\ pension contributions.

(6) Other income

On 1 February 2023, Paul received a premium bond prize of £100. On 31 March 2023, Paul received the interest of £1,260 and dividends of £5,800.

Required:

Calculate the income tax payable by Paul for the tax year 2022/23.

You are advised to use the income tax proforma to work out the question.

Question 2

Andy and Bob have been in partnership since 6 April 2012 as management consultants. The following information is available for the tax year 2022/23:

(1) Personal information

Andy spent 190 days in the United Kingdom (UK) during the tax year 2022/23. Andy was resident in the UK during the tax year 2021/22.

Bob spent 100 days in the UK during the tax year 2022/23 living in his holiday home in Derby. Bob also spent 100 days in the UK in each of the previous five tax years, and was treated as resident in the UK during each of the previous three years.

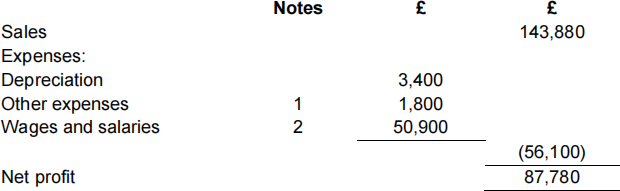

(2) Statement of Profit or Loss for the year ended 5 April 2023

The partnership¶s sXmmarised statement of profit or loss for the \ear ended 5 April 2023 is:

Notes:

1. The figure of £1,800 for other expenses includes £720 for entertaining employees. The remaining expenses are all allowable.

2. The figure of £50,900 for wages and salaries includes the annual salary of £4,000 paid to Bob (see the profit sharing note below).

(3) Plant and machinery

On 6 April 2022 the ta[ Zritten doZn YalXes of the partnership¶s plant and machinery were:

Main pool £3,100

Car 1 £21,000

The following transactions took place during the year ended 5 April 2023:

Cost

8 May 2022 Purchased Car 2 £10,150

21 November 2022 Purchased Car 3 £14,200

14 January 2023 Purchased Car 4 £11,600

Car 1 was purchased in March 2020 and has a CO2 emission rate of 125 grams per kilometre. It is used by Andy, and 80% of the mileage is for business journeys.

Car 2 was a new car purchased on 8 May 2022 and has zero CO2 emissions. It is used by Bob, and 80% of the mileage is for business journeys.

Car 3 purchased on 21 November 2022 has a CO2 emission rate of 40 grams per kilometre. Car 4 purchased on 14 January 2023 has a CO2 emission rate of 90 grams per kilometre. Car 3 and Car 4 are used by employees of the business.

(4) Profit sharing

Profits are shared 80% to Andy and 20% to Bob. This is after paying an annual salary of £4,000 to Bob, and interest at the rate of 5% on the partners¶ capital account balances.

The capital account balances are:

Andy £56,000

Bob £34,000

Required:

(a) Explain why both Andy and Bob will each be treated for tax purposes as resident in the UK for the tax year 2022/23.

(b) CalcXlaWe Whe parWnerVhip¶V Wa[ adjXVWed Wrading profiW for Whe \ear ended 5 April 2023, and the trading income assessments of Andy and Bob for the tax year 2022/23.

Your computation should commence with the net profit figure of £87,780, and should also list all of the items referred to in Notes 1 and 2 indicating by the use of zero (0) any items that do not require adjustment.

2023-10-21