FINANCIAL ECONOMETRICS A TERM EXAM

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FINANCIAL ECONOMETRICS A TERM EXAM

SHORT CALCULATION AND CONCEPTUAL

1. (3 points) Suppose Y = βX +uwhere X ∼ Ⅵ(µX ,σX(2)), u ∼ Ⅵ(0,σ2 ), and X and u are iid. What is corr(X, Y)? Report it in terms of β , µX , σX(2), and σ2 .

2. (3 points) Briefly discuss White’s covariance estimator. When and why should it be used? When should it not be?

3. (3 points) When we express the CAPM in excess return form, can the test assets be differences between risky assets i and j , Ri − Rj, not Ri − Rf , i’s return in excess of the risk-free rate? Show this using the CAPM formula. If so, what would be the interpretation of the regression coefficient?

4. (2 points) Can you run the GRS test on a model that uses industrial production growth (Δipt) as a factor, Rit(e) = αi+ βiΔipt+ uit?

5. (4 points) Fama and French (1997) report that pricing errors are correlated with betas in a test of a factor pricing model on industry portfolios. How is this possible? In what case would it not be and why?

6. (3 points) Explain in a paragraph what is meant by a hedge fund manager saying to an investor “My beta is your alpha.”

QUANTITATIVE AND INTERPRETATION

7. Your performance evaluation of an equity portfolio indexed by i using the CAPM benchmark, Rit(e) = αi+ βiRw(e)t+ uit fort = 1,...,T, led to the following statistics:

(a) (4 points) Calculate and interpret the regression coefficients

(b) (5 points) Compute the regression’s R2 and explain what it means

(c) (8 points) The correct critical values obtained from a two-sided test at a 10% significance level is ±1.66. Assume homoskedastic standard errors and

i. test the null of H0 : αi = 0

ii. test the null of H0 : βi = 1.1

(d) (3 points) What is the portfolio’s average return? What is its expected return given a market return of 5%?

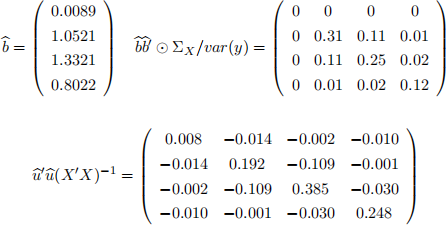

Suppose you then extended your analysis to the Fama-French 3-factor model, Rit(e) = αi + βiRw(e)t+ siSMBt+ hiHMLt+ uit fort = 1,...,T. In matrix notation you ran y = Xb + u and reported1

(e) (4 points) Explain what happened to α and β and classify the portfolio as small or big and value or growth.

(f) (2 points) Which two factors explain most of the variation in the portfolio’s return?

8. Appended at the end of the exam is a regression table on portfolios ranked by distress (the probability of default over the next 12 months) and resorted every year. I recommend you detach the table from the exam.

(a) (4 points) Examine the patterns across portfolios in mean excess returns and alphas. Does controlling for additional factors help reduce the magnitude of alphas among the most distressed portfolios?

(b) (4 points) Look at how 3-factor betas vary across portfolios. Explain how this variation makes intuitive sense in context of the sorting characteristic.

(c) (3 points) Concisely discuss if this an asset pricing anomaly.

(d) (2 points) Given the estimates, what is a reasonable interval for the price of risk for the new factor?

CODING

9. (3 points) Write the line of Matlab code for an anonymous function that evaluates the density of a normal distribution at point x with mean μ and variance σ2

10. The script appended to the end of the exam executes a series of commands. I recommend you detach the script from the exam. Some lines of code on the script are wrong and some of them are unneces- sary. The goal is to (1) remove unnecessary code and (2) fix the necessary remaining code. Assume that there is one factor and N excess returns Re, each of data length T so that Re is a TxN matrix. Reference the enumerated lines of code in your answers.

(a) (3 points) First, identify the code that is unnecessary. Instead, what should the correct code be?

(b) (5 points) There are several errors among the necessary code. List and describe the errors

(c) (5 points) Describe specifically what the following groups of lines of code do assuming the necessary code has been fixed and is correct: line 1, lines 4-7, 9-13, 15-17, and line 20

(d) (2 points) Describe briefly what this code broadly does in a paragraph

2023-10-20