Final, Math 177 - Summer session 2021

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Final, Math 177 - Summer session 2021

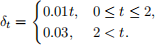

1. (10 points) Alice’s investment yields the following force of interest:

For a 5 year investment starting at time 0, what is her annual effective yield rate?

2. (15 points) Mr Neverdie is 55 years old and wants to retire at the age of 65. Because he expects to never die, he purchases a perpetuity-immediate that makes monthly level payments of 3000 starting at the end of the first month following his 65th birthday.

To purchase this perpetuity, he will be making ten annual payments starting at his 50th birthday. Each payment after the first payment will increase by 5%. Assuming a constant annual effective interest rate of 5% what will be the ammount of his tenth payment?

3. (15 points) Study problem: Find out what it means that a bond is valued at par. Then solve the following problem:

Consider a 25-year bond with face value 1000 and semi-annual coupons with normal coupon rate r.

Assume that Bob purchased the bond at-par for 1500. Determine the coupon rate r.

4. (14 points) Bob borrowed D from Alice. He is repaying his loan in n annual level payments starting one year after receiving the loan. The effective annual interest rate is 3.5%. Assume that he reduced the principal by 100 in his (n − 2)th payment.

(a) Find out the level payment K per year.

(b) Find out the interest he pays in his (n − 12)th payment.

5. Company A must pay a liability of 100, 000 in 3 years. The current effective annual interest rate is 5%.

Company A wants to immunize itself and buys X many 1-year and Y many 4-year zero coupon bonds.

The company would like to achive a Redington Immunization.

(a) (7 points) What would be X and Y? Hint: use condition (i) and (ii).

(b) (7 points) Is your proposed immunization from the first part a Redington Immunization? Hint: check condition (iii).

6. (12 points) According to the current term structure of interest rates, the effective annual interest rates for 1, 2 and 3 year maturity zero coupon bonds are 0.09, 0.11 and 0.13 respectively. Find the one-year forward effective annual rate of interest and find the two-year forward effective annual rate of interest.

7. Study problem: Find out what is a European call and European put. Then solve the following problem:

Consider a non-dividend paying asset. Let C0(K) denote the price of a European call at time 0 with strike price K and strike date T. Let P0(K) denote the price at time 0 of a European put with strike price K and strike date T. Let F(0, T) denote the forward price of the underlying asset at time 0 with delivery date T. Let r denote the force of interest.

(a) (10 points) Show that the price at time 0 of a forward contract of delivering one unit of the asset at time T with delivery price K is given by

.

(b) (10 points) Show by using an arbitrage argument that

2021-09-13