BFW2751 Derivatives 1 Assessment 2

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

BFW2751

Derivatives 1

Assessment 2

Learning Outcomes

This assignment assesses the following learning outcomes:

|

Learning Outcome Number |

Learning Outcome Description |

|

LO1 |

Discuss the operations of derivatives markets |

|

LO2 |

Evaluate the options and futures markets for hedging and trading purposes |

|

LO3 |

Demonstrate how to price and value standards futures and options contracts and other derivatives |

|

LO4 |

Implement trading strategies and measure positions |

Weighting

This assignment is worth 30% of your overall grade for this unit.

Requirements

This assignment has the following requirements:

|

Assignment Type |

Individual |

|

Response Format |

Written copy (Typed). Only answers. |

|

Response Specifications

|

Use Times Roman 12 font double spacing for your typed answers. You are not allowed to cut and paste any formulas, tables, graphs, or pictures in your answer space. |

|

Due Date |

4.30 pm (Malaysian Time), 18 September 2023 |

|

Submission Process |

Submit with Moodle as Word doc or PDF format |

|

Notes: |

tutorials, lectures, and text book materials |

Assignment Instructions

There are two parts, you are required to attempt all questions in Part 1 and Part 2. Provide the required answers and show all illustrations (workings) for each question as given below. Use Times Roman 12 font double spacing for your typed answers. You are not allowed to cut and paste any formulas, tables, graphs, or pictures in your answer space.

In Part A you are required to explore the Derivatives market operations and understand the mechanics of the Futures contract market. Compute the Optimum Hedge Ratio between the price movements of an underlying asset and its Futures contracts. Part B mainly examines the difference between speculation using forward and option strategies that can be implemented in hedging currency risk and addressing market conditions when it is volatile. You are also required to select the best option strategy in the given market conditions while evaluating its cost-benefit. These would require knowing the concepts of options strategies, the basic payoff for long and short positions, and factors that impact the option premium.

Part A (Total marks 25)

The case puts you in the shoes of a research analyst who is examining the jet fuel hedging strategy of JetBlue Airways for the coming year 2012. Airlines cross-hedge their jet fuel price risk using derivatives contracts on other oil products such as WTI and Brent crude oil. Consequently, an airline is exposed to basis risk. In 2011, dislocations in the oil market led to a Brent-WTI premium wherein jet fuel started to move with Brent instead of WTI, as it traditionally did. Several U.S. airlines started to change their hedging strategies, moving away from WTI. Entering 2012, should JetBlue also switch its hedging instruments toward Brent. The hedging strategy is for 20 million gallons per month. Each WTI and Brent futures contract size equals 42,000 gallons (1,000 barrels).

Assignment Questions (Total Marks 25)

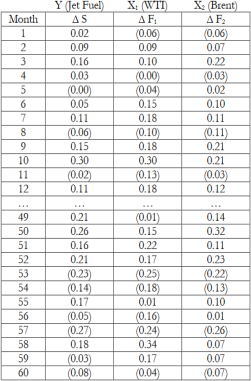

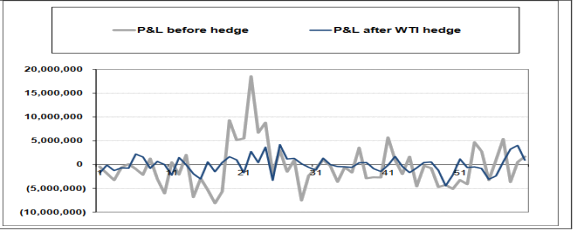

You are recommended to refer to figures 1 through 5 in order to address the following questions.

Q.1 Given the high price of jet fuel at the end of 2011 (refer to figure 1), should JetBlue hedge its fuel costs for 2012? And, if so, should it increase or decrease the percentage hedged for 2012? Provide your reason with a brief explanation. (5 marks)

Q.2 What is the effect of other competing U.S. airlines’ decisions to hedge on JetBlue’s own decision? Does it matter if competitor airlines hedged at high levels (as in Europe) or instead hedged very little (as in Asia)? Briefly provide your arguments. (5 marks)

Q3. How do airlines hedge their jet fuel price risk? Briefly discuss. Can also refer to Figure 3. (5 marks)

Q.4 Referring to Figure 5, Compute the hedging ratio and number of contracts to hedge the position for WTI and BRENT oil futures. (10 marks)

Figure 1: Historical Monthly Price Changes in the last 60 months in Jet Fuel spots and Price changes in Traded Oil Futures (WTI crude oil, Brent crude oil)

Figure 2: Hedge with WTI Futures – Profit and loss past five years

Figure 3: Hedge with Brent Futures – Profit and loss past five years

Figure 4: 2012 Fuel Hedging at JetBlue Airways. The correlation between monthly price changes in Jet Fuel spot price and price changes in traded oil futures (WTI, Brent, Heating Oil)

Figure 5: Correlation and standard deviation

Part B (Total Marks 75 marks)

i) Options Strategies for a Volatile Market (Total Marks 60 marks)

Meghna, a trader employed at Wellvet Partners, a provider of financial services, had the task of devising and executing option strategies tailored for unpredictable markets. Collaborating with Aruna, a seasoned Senior Options Strategist, they devised a plan to leverage Nifty March 2020 options for executing these strategies amidst market volatility. During the final week of February, India's VIX (Volatility Index), an indicator of stock return volatility traded on the NSE, experienced a surge of 70%. This surge bolstered Meghna's conviction in the market's volatility, anticipating Nifty to exhibit a movement of at least 10% in either direction throughout March 2020. Nevertheless, Aruna cautioned Meghna about the potential for market stability and advised her to assign equal probabilities to both volatile and stable market scenarios when selecting an option strategy.

Although this scenario is contextualized within the context of the COVID-19 pandemic outbreak in February and March 2020, its relevance extends to any period characterized by market volatility. The analysis employs the NIFTY index from the National Stock Exchange of India to elucidate pertinent principles. Furthermore, the principles deliberated herein are equally applicable to options linked with various underlying assets such as commodities, currencies, bonds, and more

ASSIGNMENT QUESTIONS

1. How do options strategies differ from speculation using options? (6 marks)

2. What option strategies are useful/profitable under the assumption of volatile market conditions? (8 marks)

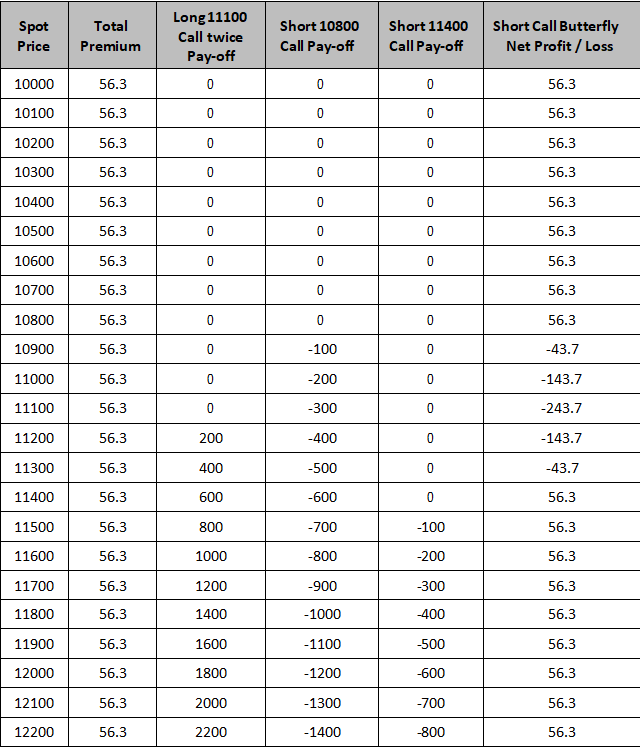

3. Draw a pay-off table and a diagram for each of the following strategies. Show maximum profit, maximum loss, and breakeven point(s). Use the suitable tables provided below.

a. Long Straddle (10 marks)

Long ATM Call and ATM Put have the same underlying asset and same maturity. Long 11100 Call @ Rs. 287.75 and Long 11100 Put @ Rs. 273.3. Long Strangle

Long OTM Call and OTM Put having the same underlying asset and same maturity Long 11200 Call @ Rs. 238.75 and Long 11000 Put @ Rs. 233

b. Long Strangle (10 marks)

Long OTM Call and OTM Put having the same underlying asset and same maturity Long 11200 Call @ Rs. 238.75 and Long 11000 Put @ Rs. 233

c. Short Call Butterfly (10 marks)

Long ATM Call twice, Short ITM call, and Short OTM call

Long 11100 Call twice @ Rs. 287.75, Short 10800 Call @ Rs. 481.85, and Short 11400 Call @ Rs. 149.95

d. Short Put Butterfly (10 marks)

Short ATM Put twice, Long ITM Put, and Long OTM Put

Long 11100 Put twice @ Rs. 273.3, Short 10800 Put @ Rs. 174.15 and Short 11400 Put @ Rs. 421.45

4. Compare and contrast each strategy and find out which strategy is better. (6 marks)

Note: Use the following tables to support the above questions

Table 1: Nifty Option Closing Prices in Rupees as of March 02, 2020

Table 2: Pay-off Table for Long Straddle

Table 3: Pay-off Table for Long Strangle

Table 4: Pay-off Table for Short Call Butterfly

Table: 5 Pay-off Table for Short Put Butterfly

ii) Forward strategy for currency hedging (Total Marks 15)

Wellvet Partners is renowned for its provision of currency hedging services to international clients. Recently, Square Corporation, a US-based firm, approached them for advice regarding a future transaction scheduled for December 2022, involving an invoice of AUD $10 million. The US firm is uncertain about its exposure to foreign currency fluctuations in December. In response, Wellvet Partners is recommending the use of a forward contract to mitigate this risk, employing the USD/AUD exchange rate when the December forward rate stands at USD 0.760 per AUD, while the spot rate is USD 0.71 per AUD. The size of one USD/AUD forward contract equals AUD 100,000.

ASSIGNMENT QUESTIONS

a) Determine the payoff and effective exchange rate for the long or short party if, at expiration, ST turns out to be USD 0.780/AUD for AUD$10m (5 marks)

b) Find the optimal number of contracts by using the optimal hedge ratio if the historical data estimate R2F (Dec USD/AUD) 0.177, R2S (Dec USD/AUD)0.162, and ![]() 0.928 (5 marks)

0.928 (5 marks)

c) Should the decision be made to hedge only 50% of the exposure, how many contracts would the US firm engage in? (5 marks)

2023-09-16