ECMT6006/ECON4949/ECON4998 Mid-semester Test (Main) 2021

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECMT6006/ECON4949/ECON4998

Mid-semester Test (Main)

21 April 2021

Instructions: This is an open-book exam, and all materials are permitted. please attempt all questions. The total mark is 35 and the breakdown is shown in square brackets. The duration of the exam is 1.5 hours for writing time.

problem 1. [12 marks] Let pt be the price of a stock on date t, and assume the stock pays no dividend. Let Rt+1 and rt+1 be, respectively, the simple gross return and log return of this stock from time t to t + 1. Answer the following questions.

(i) show that a forecast of pt+1, denoted as pt+1 = Et (pt+1), can be derived from a forecast of Rt+1. [1 mark]

(ii) Let Rtyt+k be the k-period gross return. show that Rtyt+k can be written as a function of 1-period gross returns. [1 mark]

(iii) Let rtyt+k be the k-period log return deined as rtyt+k = ln(Rtyt+k). show that rtyt+k can be written as a function of 1-period log returns. [1 mark]

(iv) when the value of the log return is close to that of the arithmetic net return, and why? [1 mark]

(v) Explain how to conduct a robust joint test for the autocorrelation in the log return rt+1 using a regression-based approach. Be explicit about the regression you run, the test statistic you construct, and how you make testing decisions. [3 marks]

(vi) suppose you could not ind signiicantautocorrelation in rt+1 by the above test. what can you say about the predictability of this stock return? [2 marks]

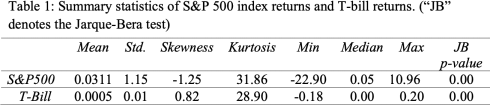

(vii) The below table shows the summary statistics of daily returns of s&p5oo index from 1999 to 2oo9 and daily returns of Us 3-month T-bill rates from 1989 to 2oo9. please interpret the table and compare these two return series. [3 marks]

problem 2. [8 marks] Consider the following weakly stationary AR(1)-ARCH(1) model for stock returns

Rt = φ0 + φ1 Rt- 1 + εt

where

Et |大t- 1 … N (O, σt(2)),

σt(2) = w + aEt(2)- 1 .

Assume |φ1 | < 1, w 持 O, a > O. Answer the following.

(i) show that {Et } is a white noise process. [2 marks]

(ii) show that {Et(2)} is an AR(1) process. what restriction should we make on a to guarantee that {Et(2)} is weakly stationary? [2 marks]

(iii) what are the conditional mean Et (Rt+1) and unconditional mean E(Rt )? [2 marks]

(iv) what are the conditional variance VaTt (Rt+1) and unconditional variance VaT(Rt )? [2 marks]

problem 3. [15 marks] consider a two-period model for returns Rt , t = 1, 2 of an asset. Let EO = 1, and

Rt = μ + Et ,

Et = σtvt , σt = | Et- 1 | ,

where μ = 1, and v1 , v2 are independent and identically distributed as

vt = { -1,2, with probability 1(with probability 2)/(/)3(3)

for t = 1, 2. Let 大t be the information set available at time t. please answer the following questions.

(i) what is the probability distribution of R1 ? [2 mark]

(ii) what is the probability distribution of R2 ? [2 marks]

(iii) compute the conditional mean E1 (R2 ) := E(R2 |大1 ). [2 mark]

(iv) compute the conditional variance var1 (R2 ) = var(R2 |大1 ). [2 marks]

(v) verify the law of iterated expectation E(R2 ) = E [E1 (R2 )] using numbers given in this problem. [2 marks]

(vi) what are the one-period ahead return point forecasts R(教)t for t = 1, 2? [2

marks]

(vii) what are the two standard deviation one-period ahead return inteTval forecasts for t = 1, 2? [3 marks]

2023-09-01