BFC3140 Corporate Finance 2 Week 03

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

BFC3140 Corporate Finance 2

Week 03 Tutorial Answers – Capital Structure: Financial Distress, Managerial Incentives and Information Asymmetry (Chapter 16)

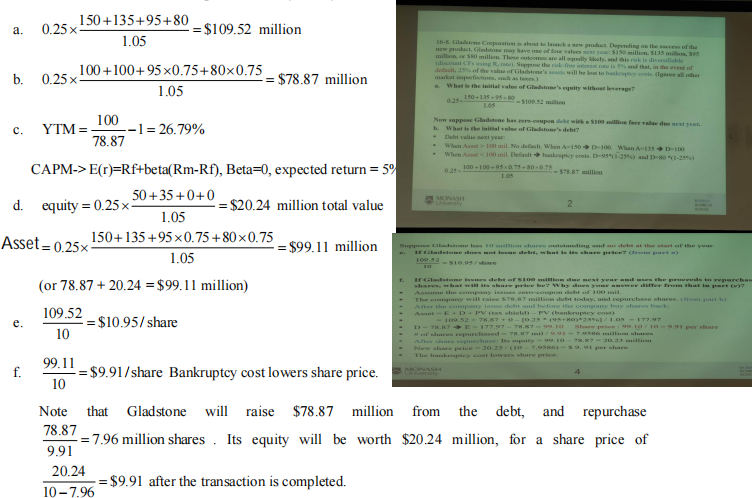

16-8. As in Problem 1, Gladstone Corporation is about to launch a new product. Depending on the success

of the new product, Gladstone may have one of four values next year: $150 million, $135 million, $95 million, or $80 million. These outcomes are all equally likely, and this risk is diversifiable. Suppose the risk-free interest rate is 5% and that, in the event of default, 25% of the value of Gladstone’s assets will be lost to bankruptcy costs. (Ignore all other market imperfections, such as taxes.)

a. What is the initial value of Gladstone’s equity without leverage?

Now suppose Gladstone has zero-coupon debt with a $100 million face value due next year.

b. What is the initial value of Gladstone’s debt?

c. What is the yield-to-maturity of the debt? What is its expected return?

d. What is the initial value of Gladstone’s equity? What is Gladstone’s total value with leverage?

Suppose Gladstone has 10 million shares outstanding and no debt at the start of the year.

e. If Gladstone does not issue debt, what is its share price?

f. If Gladstone issues debt of $100 million due next year and uses the proceeds to repurchase shares, what will its share price be? Why does your answer differ from that in part (e)?

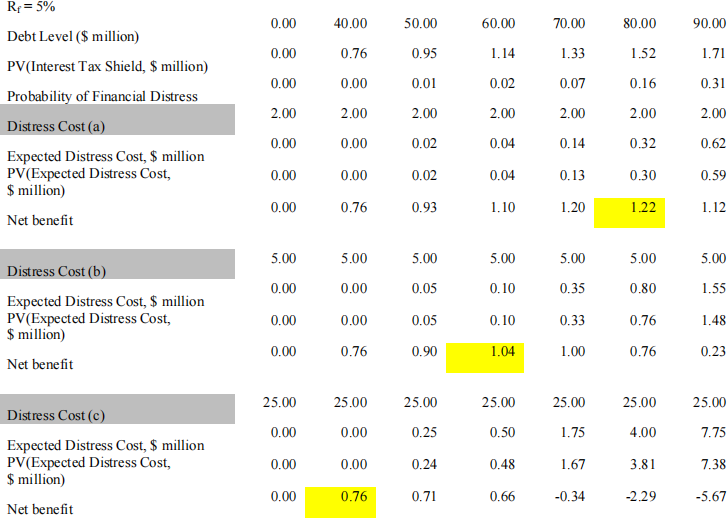

16-13. Your firm is considering issuing one-year debt, and has come up with the following estimates of the value of the interest tax shield and the probability of distress for different levels of debt:

Suppose the firm has a beta of zero, so that the appropriate discount rate for financial distress costs is the risk-free rate of 5%. Which level of debt above is optimal if, in the event of distress, the firm will have distress costs equal to

a. $2 million?

b. $5 million?

c. $25 million?

a. 80

b. 60

c. 40

Where

Expected Distress Cost = Probability of Financial Distress * Distress Cost

PV(Expected Distress Cost) = Expected Distress Cost/(1+ Rf)

16-15. Real estate purchases are often financed with at least 80% debt. Most corporations, however, have less than 50% debt financing. Provide an explanation for this difference using the tradeoff theory.

According to tradeoff theory, a tax shield adds value while financial distress costs reduce a firm’s value. The financial distress costs for a real estate investment are likely to be low, because the property can generally be easily resold for its full market value. In contrast, corporations generally face much higher costs of financial distress. As a result, corporations choose to have lower leverage.

|

16-16. |

On May 14, 2008, General Motors paid a dividend of $0.25 per share. During the same quarter GM lost a staggering $15.5 billion or $27.33 per share. Seven months later the company asked for billions of dollars of government aid and ultimately declared bankruptcy just over a year later, on June 1, 2009. At that point a share of GM was worth only a little more than a dollar. a. If you ignore the possibility of a government bailout, the decision to pay a dividend given how close the company was to financial distress is an example of what kind of cost? b. What would your answer be if GM executives anticipated that there was a possibility of a government bailout should the firm be forced to declare bankruptcy? a. Agency cost—cashing out |

b. By paying a dividend, executives increased the probability of bankruptcy and therefore the probability of receiving government funds. Since these government funds are funds that investors would not otherwise be entitled to, the payment of a dividend could actually raise firm value in this case.

|

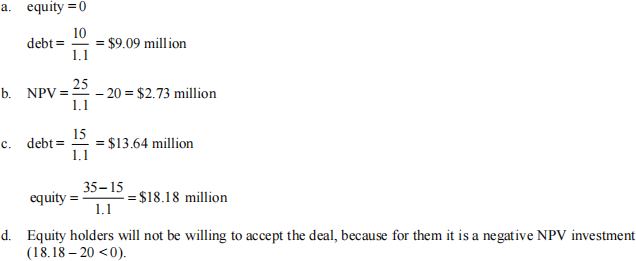

16-18. |

Consider a firm whose only asset is a plot of vacant land, and whose only liability is debt of $15 million due in one year. If left vacant, the land will be worth $10 million in one year. Alternatively, the firm can develop the land at an upfront cost of $20 million. The developed land will be worth $35 million in one year. Suppose the risk-free interest rate is 10%, assume all cash flows are risk-free, and assume there are notaxes. a. If the firm chooses not to develop the land, what is the value of the firm’s equity today? What is the value of the debt today? b. What is the NPV of developing the land? c. Suppose the firm raises $20 million from equity holders to develop the land. If the firm develops the land,what is the value of the firm’s equity today? What is the value of the firm’s debt today? d. Given your answer to part (c), would equity holders be willing to provide the $20 million needed to develop the land?

|

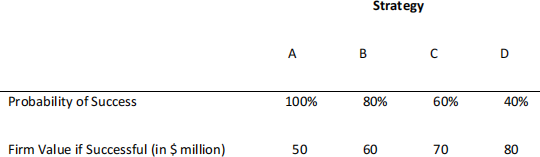

16-21. Petron Corporation’s management team is meeting to decide on a new corporate strategy. There are

four options, each with a different probability of success and total firm value in the event of success, as shown below:

Assume that for each strategy, firm value is zero in the event of failure.

a. Which strategy has the highest expected payoff?

b. Suppose Petron’s management team will choose the strategy that leads to the highest expected

value of Petron’s equity. Which strategy will management choose if Petron currently has

(i) No debt?

(ii) Debt with a face value of $20 million?

(iii) Debt with a face value of $40 million?

c. What agency cost of debt is illustrated in your answer to part (b)?

Thus, the firm will choose strategy A when D = 0, B when D = 20, and C when D = 40.

c. This result illustrates the agency cost of excessive risk taking with leverage. As the amount of leverage increases, the firm’s equity holders prefer that the firm adopt riskier strategies, even though these riskier strategies lower the total value of the firm.

2023-08-26

Capital Structure: Financial Distress, Managerial Incentives and Information Asymmetry