Mathematical Finance, ECON5020

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

MathematicaI Finance, ECON5020

Answer ONE of the two questions.

1. consider an elementary market model. Assume that there exist a stock and a cash bond in the model. The initial price of the stock is 北40. The investor believes that with probability 1/3 the stock price will remain the same and with probability 2/3 the stock price will rise to 北80 at the end of the time period. The cash bond has an initial price of 北1 and it will with certainty deliver 北7/6 at the end of the period.

Does this model admit any arbitrage opportunities?Explain your answer.

write payofs for a digital put option with a maturity at the end of the time period and a strike price of 北65.

use the replication principle and ind a price of this contingent claim. How many bonds will investor buy?

Find the price using the risk neutral valuation formula.

Discuss the equivalence of the two approaches.

The quality of your answer is very important for the mark. please explain your answer carefully, explain the notation you use, give clear references to deinitions, theorems and claims that you use to support your statements.

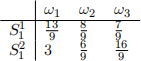

2. consider the single-period market model w = (B, S1 , S2 ) with three states of nature Ω = {w1 , w2 , w3 } . Let the interest rate be T = ![]() are given by S0(1) = 1 and S0(2) =

are given by S0(1) = 1 and S0(2) = ![]() . Random stock prices at time t = 1 are given by the following table

. Random stock prices at time t = 1 are given by the following table

use FTAp to investigate whether this market model admits an arbitrage opportunity. Is this market complete? Explain your answer.

The quality of your answer is very important for the mark. please explain your answer carefully, explain the notation you use, give clear references to deinitions, theorems and claims that you use to support your statements.

2023-08-14