4QQMB101 Accounting and Financial Reporting Examination 2022/23

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Examination 2022/23

Module Code and Title: 4QQMB101 Accounting and Financial Reporting

Examination Period: Exam Period 1, January 2023

Answer all four questions.

Question 1

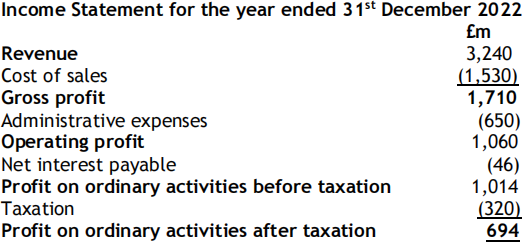

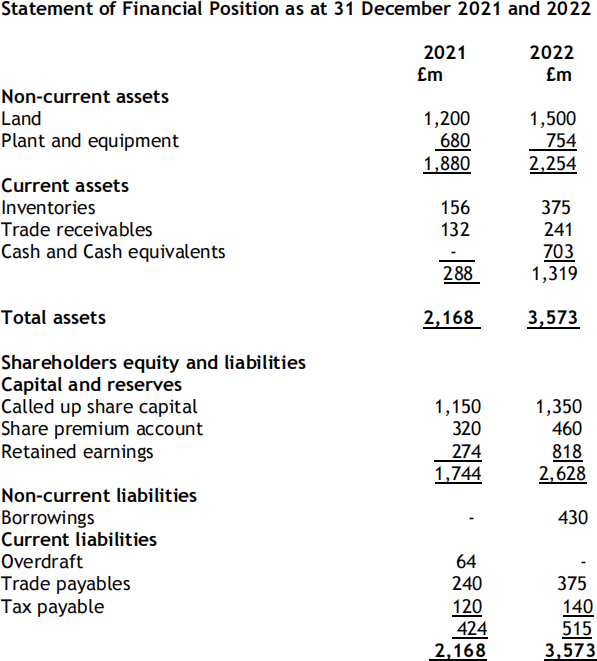

Blackheath plc’s Income Statement for the year ended 31 December 2022 and the Statements of Financial Position as at 31 December 2021 and 2022 are as follows:

During 2022, the business spent £590m on additional non-current assets.

There were no other non-current assets acquisitions or disposals. A dividend of £150m was paid on ordinary shares during the year.

REQUIRED

a) Prepare a cash flow statement for Blackheath plc for the year ended 31st December 2022. [13 marks]

b) Make any relevant comments about Blackheath’s plc’s cash flow statement which you feel should be drawn to the attention of its management. [12 marks]

Total marks for Question 1 [25 marks]

Question 2

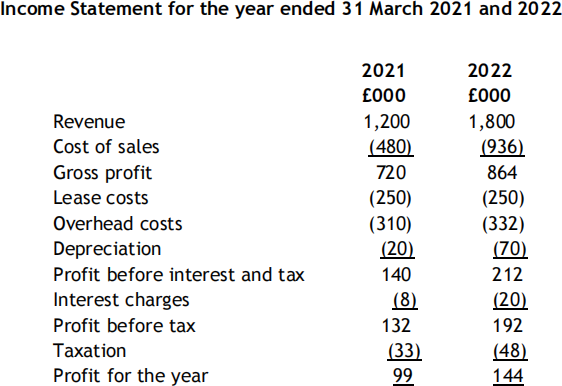

The income statement and the statement of financial position for the year ended 31 March 2021 and 2022 for Ashuka Limited.

Additional information:

Note 1

Non-current assets are analysed as below:

No assets were sold during the year end 31st March 2022

Note 2

Note that trade payables and accruals shown in the statement of financial position are analysed as below:

REQUIRED

a) Calculate the following ratios for 2021 and 2022 from the income

statements and statements of financial position provided above (ratio formulas included at the end of the booklet) .

• Gross profit margin

• Return on capital employed

• Current ratio

• Quick ratio

• Gearing ratio

• Interest cover ratio

• Average inventories turnover period

• Average settlement period for receivables [8 marks]

b) Using the information provided in the financial statements and the ratios that you have calculated, write a management report to the board of directors commenting on the company’s operations for the financial year end 31st March 2022 compared to the previous year. [17 marks]

Total marks for Question 2 [25 marks]

Question 3

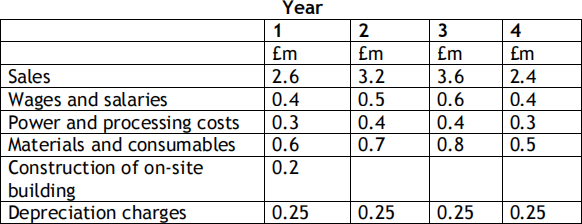

Chipping plc is considering purchasing a mature forest in Finland at a cost of £3m. The company's lawyers have spent the last year examining the potential of the purchase and have incurred costs to date of £0.2m. The purchase price for logging equipment will be £1.5m in order to cut and process the timber and these assets can be sold for £0.5m in four years’ time when the timber has been cut. The forest will then be sold ready for a new operator to start the next growing cycle. The proceeds from the sale are expected to be £0.8m which will be received at the end of year 4.

The Finance Director of the company has prepared the following projected figures for each year of operations:

The following additional information is available:

i. The project will require an investment of £0.4m of working capital from the beginning of the project until the end of the project.

ii. At the end of year 4, the company will incur costs of £0.2m cleaning up the site.

iii. Chipping plc intends to allocate head office costs of £0.2m per year to the project. These costs have not been included above and will be incurred whether or not the project is undertaken.

The company has a cost of capital of 10%.

Ignore taxation.

REQUIRED

a) Calculate the Net Present Value (NPV) and Internal Rate of Return

(IRR) for the above project stating if the project should be undertaken or not, giving reasons for your choice. [15 marks]

b) Compare and contrast NPV and IRR as investment appraisal methods, include in your comparison which method you consider to be the best one to use for investment appraisal. [10 marks]

Total marks for Question 3 [25 marks]

Question 4

a) Given the following information taken from the budgets of Winchester Ltd completed during the budget process, prepare a cash budget for Winchester Ltd for the 3 months April to June. [9 marks]

Other information

• Winchester Ltd sells 25% of its goods for cash. The remainder of customers take one month’s credit.

• Purchases are paid the month after they are incurred.

• Wages are paid one month in arrears and are calculated on a commission basis of 20% of the monthly sales revenue.

• Overheads are paid the month after they are incurred and the numbers above include £500 per month of depreciation

• Winchester Ltd intends to buy a new machine for a cost of £6,000 on 1st March. The machine will be classified as a non-current asset and depreciated over five years on a straight line basis. Payment will be in the form of an initial deposit of £1,200 paid on 1st March followed by 12 equal monthly instalments starting 1st April.

• The cash balance forecast at the beginning of April is £400.

b) Alpha plc operates a retail business. Purchases are sold at cost plus 25%. The management team are preparing the cash budget and have gathered the following data:

i. The budget sales are as follows:

Month

January 90

February 100

March 80

April 120

ii. It is management policy to hold inventory at the end of each month which is enough to meet the sales demand for the next half month. Sales are budgeted to occur evenly during each month.

iii. Creditors are paid one month after the purchase has been made

Calculate the entries for purchases that will be shown for February, March and April. [3 marks]

c) “Managing costs is very important given the competitive environment in which modern businesses operate. ”

Discuss this statement including in your discussion some of the recent

approaches to costing which have emerged to help businesses manage their costs. [13 marks]

Total marks for Question 4 [25 marks]

RATIO FORMULAS

Profitability Ratios

Return on capital employed (ROCE) (%) = operating profit divided by capital employed x100

*capital employed = share capital + reserves + non-current liabilities *operating profit = profit before interest and tax

Gross profit margin (%) = gross profit divided by sales revenue x 100.

Operating profit margin (%) = operating profit divided by sales revenue x 100.

Efficiency Ratios

Sales revenue to capital employed (£) = sales revenue divided by share capital + reserves + non-current liabilities

Average inventories turnover period = inventory divided by cost of sales x 365

Average settlement period for receivables = trade receivables divided by sales revenue* x 365

*or credit sales if known

Average settlement period for payables = trade payables divided by cost of sales* x 365

*or credit purchases if known

Liquidity Ratios

Current ratio (:1)= current assets divided by current liabilities

Quick or acid test ratio (:1) = current assets less inventory divided by current liabilities

Gearing Ratios

Gearing ratio (%) = non-current liabilities divided by share capital + reserves + non-current liabilities x 100.

Interest cover ratio (times) = operating profit divided by interest payable

Investment Ratios

Earnings per share = earnings available to ordinary shareholders divided by number of ordinary shares in issue

Price / earnings ratio (times) = market value per share divided by earnings per share

Dividend yield ratio (%) = dividends per share divided by market value per share x 100

Dividend cover (times) = earnings for the year divided by dividend for the year

2023-08-11