ECON 6002 Problem Set 2 (Business Cycle Models)

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Problem Set 2 (Business Cycle Models)

ECON 6002

Due date: Monday, 8 May, 6pm

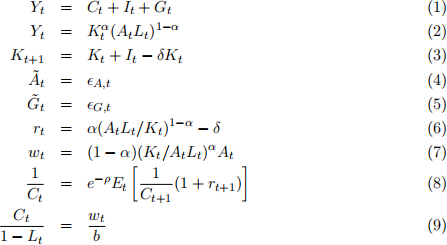

1. Abstracting from long-run growth by setting n = g = 0 and from persistent shocks by setting ρA = ρG = 0, with ![]() t = lnAt _ ln

t = lnAt _ ln![]() and

and ![]() t = lnGt _ ln

t = lnGt _ ln ![]() , and normalizing the population to N = 1, the following nine equations describe the “baseline” RBC model in Chapter 5:

, and normalizing the population to N = 1, the following nine equations describe the “baseline” RBC model in Chapter 5:

(a) Find the steady state for this economy under the following calibration: α = ![]() , δ = 0.05,

, δ = 0.05, ![]() = 0.03,

= 0.03, ![]() = 1, and

= 1, and ![]() = 0.5 and choose

= 0.5 and choose ![]() such that

such that ![]() /

/![]() = 0.2.In particular, you should find the remaining parameters values b and ρ that are consistent with steady state and determine steady-state values for the endogenous variables,

= 0.2.In particular, you should find the remaining parameters values b and ρ that are consistent with steady state and determine steady-state values for the endogenous variables, ![]() ,

, ![]() , I¯,

, I¯, ![]() ,

, ![]() , and

, and ![]() . (Hint: first solve for ρ using (8), then solve for

. (Hint: first solve for ρ using (8), then solve for ![]() using (6), then I¯ using (3), then

using (6), then I¯ using (3), then ![]() using (7), then

using (7), then ![]() using (2), then

using (2), then ![]() using (1), then b using (9).)

using (1), then b using (9).)

(b) Now consider the special case of the model where δ = 1 instead of δ = 0.05 and Gt = 0 for all t (note: ρ will remain the same and b will be different, but you do not need to solve for it). Solve for Yt , Ct , It , Kt+1 , rt, and wt as analytical expressions of exogenous and predetermined variables At and Kt and constants. (Hint: with 100% depreciation, there is a constant saving rate s = αe −p and constant labour supply Lt = ![]() . Given this solution to the household optimization problem, first solve for Yt , rt , and wt from equations (2), (6), and (7) and then the solutions for Ct , It, and Kt+1 are straightforward.)

. Given this solution to the household optimization problem, first solve for Yt , rt , and wt from equations (2), (6), and (7) and then the solutions for Ct , It, and Kt+1 are straightforward.)

(c) Again, for the special case of the model, what is the percentage change in output and percentage point change in the interest rate if the economy is at steady state at time t _ 1, but there is a shock sA,t = 0.25 (i.e., 25%) at time t? Explain the economic intuition behind the responses of output and the interest rate in terms of the marginal products of labour and capital. (Hint: note that the sA,t = 0.25 shock is to lnAt, but the model solution is for the level of At . First solve for the steady-state level of output and then solve for output and the real interest rate given the shock.)

2. Consider Calvo price-setting firms with partial indexation. That is, if a firm is not visited by the Calvo tooth fairy in period t, its price in t is the previous period’s price plus γπt − 1 , 0 < γ < 1. The average price in period t is pt = αxt + (1 _ α)(pt − 1 + γπt − 1 ), where α is the fraction of firms visited by the Calvo tooth fairy in any given period and xt is the price they set. The resulting Phillips curve is a hybrid one: πt = ![]() 8yπt − 1 +

8yπt − 1 + ![]() Etπt+1 +

Etπt+1 + ![]() κy˜t , where β > 0 is the discount factor, κ =

κy˜t , where β > 0 is the discount factor, κ = ![]() a[1 _ β(1 _ α)]φ > 0 determines the slope of the Phillips curve, y˜t is the output gap, and Etπt+1 is the expectation (taken at time t) of inflation at t + 1.

a[1 _ β(1 _ α)]φ > 0 determines the slope of the Phillips curve, y˜t is the output gap, and Etπt+1 is the expectation (taken at time t) of inflation at t + 1.

(a) Show that xt _ pt = ![]() (πt _ γπt − 1 ).

(πt _ γπt − 1 ).

(b) Use the result in (a) and the representative firm’s optimal price under Calvo pricing with partial indexation being xt = pt + (1 _ β(1 _ α))φy˜t + β(1 _ α)(Et(xt+1 _ pt+1) + Etπt+1 _ γπt) to derive the hybrid Phillips curve.

(c) What value of γ would lead to the highest degree of inflation persistence? Why?

(d) Now assume that β = 0.9, γ = 0.5, and κ = 0.1. Assume that the central bank has some control of the evolution of y˜t . Suppose that the central bank announces a permanent and fully credible reduction in its target or steady-state inflation rate from 7% to 2% at t = 1 (prior to this, the economy was at the steady state with 7% inflation and zero output gap). Determine the cost of this disinflation episode. How much is the output gap reduced?

2023-07-14