906 Groupwork Project

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

906 Groupwork Project

Introduction:

By using the Box-Jenkins approach, we focus on the finding the best fit model for the time series of the stock market in Australia, United State and China respectively.

Data description:

we choose the choose the S&P/ASX 300 index, S&P 500 and CSI300 as the representatives of the stock market in Australia, United State and China respectively, and we collect the actual daily data in 2016.

Model:

In Australia stock market:

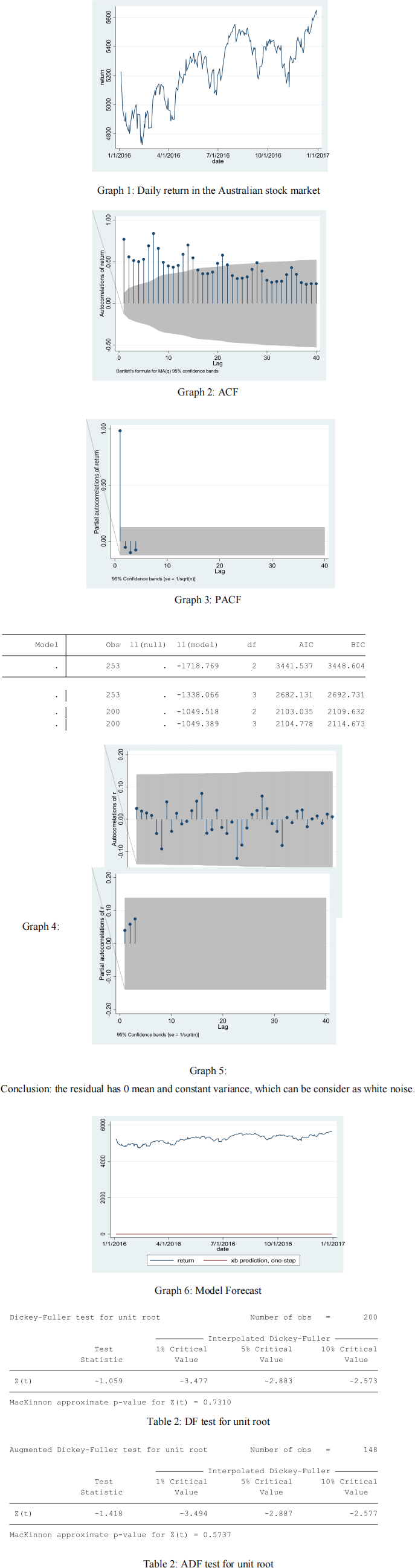

Empirical Findings for the Australian stock market:

![]() From graph 1, we can infer that the stock returns may have a trend.

From graph 1, we can infer that the stock returns may have a trend.

![]() From graph 2, ACF: exponentially decay and the sample autocorrelations show that there

From graph 2, ACF: exponentially decay and the sample autocorrelations show that there

is large even at long lags, so it is a nonstationary time series.

![]() From graph 3, PACF: it exhibits a single statistically significant spike at lag 1, while all

From graph 3, PACF: it exhibits a single statistically significant spike at lag 1, while all

other coefficients are within the confidence bands and thus insignificant. This essentially means that the remaining higher order autocorrelations are well explained by the lag 1 autocorrelation.

![]() Conclusion: it could be an AR ( 1) model with no moving average.

Conclusion: it could be an AR ( 1) model with no moving average.

![]() By comparing ARIMA (0,0,0), ( 1,0,0), (0, 1,0) and (1, 1,0) respectively with AIC and BIC

By comparing ARIMA (0,0,0), ( 1,0,0), (0, 1,0) and (1, 1,0) respectively with AIC and BIC

from table 1, ARIMA (0, 1,0) is the best model.

![]() From graph 6, although the model satisfies all the conditions it needs to be a univariate

From graph 6, although the model satisfies all the conditions it needs to be a univariate

model, it has no forecasting power as it is a simple random walk model without constant.

![]() From Table 2 and table 3, we can conclude that there is no unit root in the AU stock

From Table 2 and table 3, we can conclude that there is no unit root in the AU stock

market.

In US stock market:

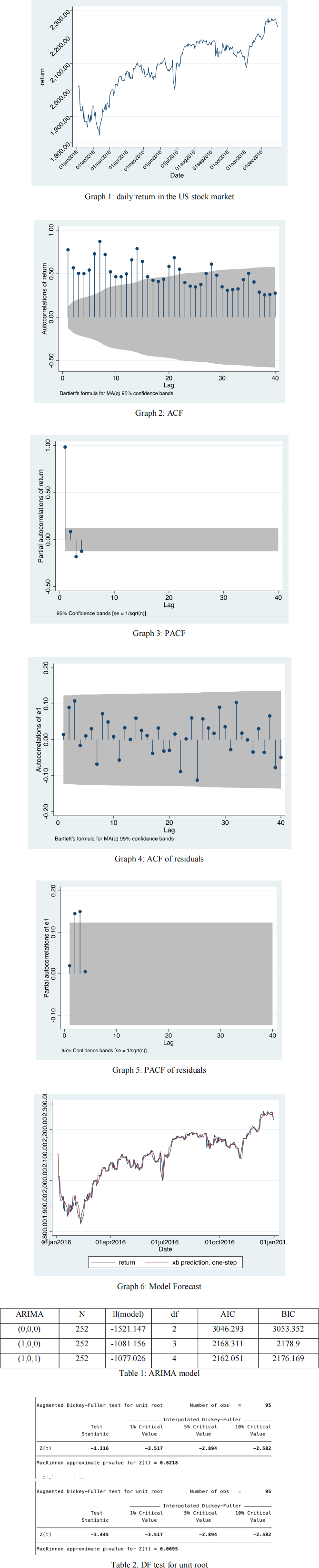

Empirical Findings for the American stock market:

![]() From graph 2, the data probably have a trend component and a seasonal component.

From graph 2, the data probably have a trend component and a seasonal component.

From graph 3, PACF: it exhibits a single statistically significant spike at lag 1, while all

other coefficients are within the confidence bands and thus insignificant. This essentially means that the remaining higher order autocorrelations are well explained by the lag 1 autocorrelation.

![]() Conclusion: it could be an AR ( 1) model with no moving average.

Conclusion: it could be an AR ( 1) model with no moving average.

![]() By comparing ARIMA (0,0,0), ( 1,0,0), and ( 1,0, 1) respectively with AIC and BIC from

By comparing ARIMA (0,0,0), ( 1,0,0), and ( 1,0, 1) respectively with AIC and BIC from

table 1, ARIMA ( 1,0, 1) is the best model.

![]() From graph 6, although the model satisfies all the conditions it needs to be a univariate

From graph 6, although the model satisfies all the conditions it needs to be a univariate

model, it has no forecasting power as it is a simple random walk model without constant.

![]() From Table 1, we can conclude that there is no unit root in the US stock market at 1%

From Table 1, we can conclude that there is no unit root in the US stock market at 1%

significance level.

In China stock market

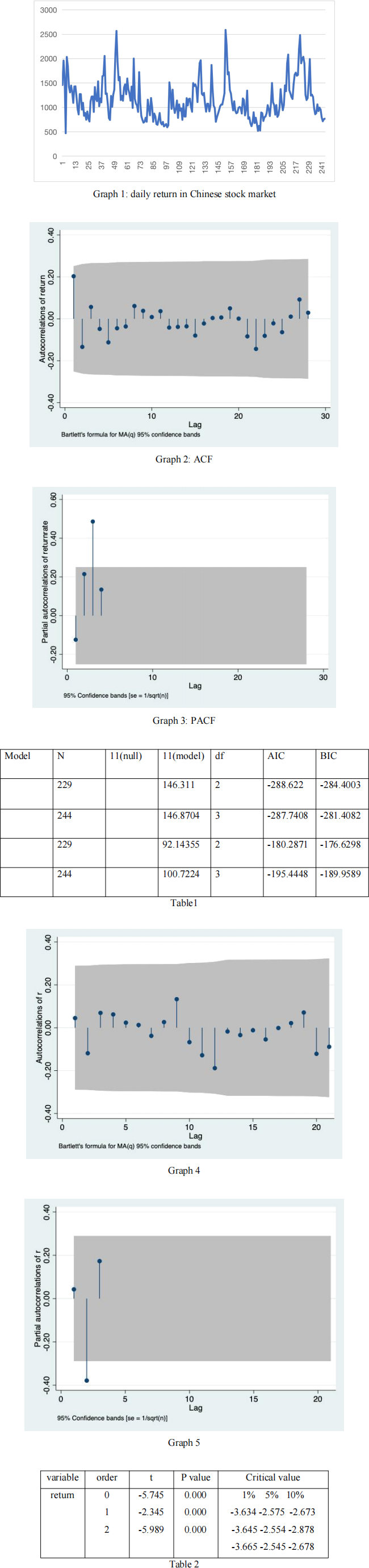

Empirical finding for the Chinese stock market:

![]() From the graph 1, it illustrates that in China stock market has some bubbles, after that, the

From the graph 1, it illustrates that in China stock market has some bubbles, after that, the

stock market has the trend

![]() ACF: the autocorrelation implies that it may be large even at long lags, at the difference

ACF: the autocorrelation implies that it may be large even at long lags, at the difference

of 0 order, the significance p-value is 0.000, and it is very significant, so we can reject the null hypothesis, and it is a non- stationary time series.

![]() PACF: The partial autocorrelation graph is shown that upper and lower confidence limits,

PACF: The partial autocorrelation graph is shown that upper and lower confidence limits,

it only represents the statistically significant in lag ( 10).

![]() Comparing ARIMA (0,0,0), ( 1,0,0)(0, 1,0)(1, 1,0)with AIC and BIC from

Comparing ARIMA (0,0,0), ( 1,0,0)(0, 1,0)(1, 1,0)with AIC and BIC from

table1.ARIMA(0, 1,0)is the best model.

![]() From graph4 and 5, the residual has 0 mean and constant variance, and it can be white

From graph4 and 5, the residual has 0 mean and constant variance, and it can be white

noise.

![]() The ADF result is on the table 2.The result show that p-value is 0.000,it means that

The ADF result is on the table 2.The result show that p-value is 0.000,it means that

significant, so we will reject the null hypothesis, it is a non-stationary time series , and has no unit root in China stock market.

Conclusion:

By using the Box-Jenkins approach to analyze the three stock market,we found that Britain's departure from Europe has no effect on atuogression and changes on these stock market.The model ARIMA( 1,0, 1)means that it has nothing to d0 with the market,and it in a random walk progress.The real policy changes on countries will have effected on their stock market.

Reference:

S&P500:

https://au.finance.yahoo.com/quote/%5EGSPC/history?period1=1420070400&period2=1577750 400&interval=1d&filter=history&frequency= 1d&includeAdjustedClose=true

S&P/ASX300:

https://au.finance.yahoo.com/quote/%5EAXKO/history?period1=1420070400&period2=157775 0400&interval=1d&filter=history&frequency= 1d&includeAdjustedClose=true

CSI 300 index:

https://www.csindex.com.cn/#/indices/family/detail?indexCode=000300

STATA code

***AU stock market

import excel "\\Client\C$\Users\75874\Desktop\au 2016.xlsx", sheet("Sheet 1") firstrow tsset date

ac return

pac return

corrgram return

*ic

varsoc return

arima return, arima(0,0,0) nolog

estat ic

arima return, arima( 1,0,0) nolog

estat ic

estat ic

arima return, arima( 1, 1,0) nolog

estat ic

*Validation

predict r,residual

sum r

corrgram r

ac r

pac r

*Forecast

arima return, arima(0, 1,0) nolog

predict forecast,xb

tsline return forecast

***US stock market

import excel "/Users/si/Desktop/2016stock.xlsx", sheet("Sheet 1") firstrow

tsset Date

tsline return

corrgram return

ac return

pac return

predict r, residuals

predict y

corrgram r, lag( 10)

ac r

pac r

arima return, arima( 0,0,0)

estat ic

arima return, arima( 1,0,0)

estat ic

arima return, arima( 1,0, 1)

estat ic

arima return, arima(2,0,0)

estat ic

arima return, arima(2,0, 1)

estat ic

arima return, arima(2,0,2)

estat ic

arima return, ar( 1/2) nolog

predict forecast, xb

tsline return forecast

***CHN stock market

tsset date

tsline returnrate

corrgram returnrate

ac returnrate

pac returnrate

varsoc returnrate

arima returnrate,arima(0,0,0)nolog

estat ic

arima returnrate,arima( 1,0,0)nolog

estat ic

arima returnrate,arima(0, 1,0)nolog

estat ic

arima returnrate,arima( 1, 1,0)nolog

estat ic

predict r,residual

sum r

corrgram r

ac r

pac r

arima returnrate, arima (0, 1,0)nolog

predict forecast,xb

tsline returnrate forecast

2023-07-12