BUSFIN 1331 – Financial Markets and Institutions Homework #1

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

BUSFIN 1331 – Financial Markets and Institutions

Homework #1

Problems from “Interest rates and security valuation”

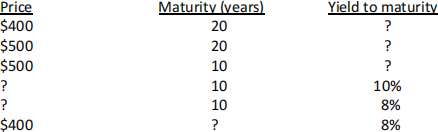

1. The table below features zero-coupon bonds by price, maturity, and yield to maturity. Fill in the missing entries (assume semi-annual compounding and a maturity value of $1,000).

2. The market thinks that over the next year, interest rates will remain unchanged. You expect interest rates to fall. Suppose you are correct. In each of the following, explain which would provide the greater capital gain.

a. A Treasury bond with 20 years to maturity paying a 7% coupon annually or a Treasury bond with

20 years to maturity paying a 10% coupon annually.

b. An AAA-rated bond with an 9% annual coupon rate and 20 years to maturity or a BBB-rated bond with an 9% annual coupon rate and 20 years to maturity.

3. You are trying to decide in which of the three investments below to invest. What role does your forecast of future interest rates play in your decision?

a. A money market fund with an average maturity of 30 days offering a current annualized yield of 3%.

b. A one-year savings deposit at a bank offering an interest rate of 4.5%.

c. A 20-year U.S. Treasury bond offering a yield to maturity of 6% per year.

4. You are obligated to pay $10,000 at the end of each of the next two years. Suppose bonds currently yield 8%.

a. What is the present value of your obligation?

b. What is the duration of your obligation?

c. What maturity zero-coupon bond would immunize your obligation? What would be the face value of this bond?

5. Consider a 3 year, 8% coupon bond (assume annual coupons) with a face value of 1,000. If the YTM of this bond is 8%.

a. Calculate this bond’s Macaulay duration and Modified duration.

b. If the bond interest rate immediately drops to 7.9%, calculate the approximate proportional change in the bond’s price using duration. Compare your answer to the actual change in the bond’s price.

c. Repeat the comparison in b. above if the new interest rate is 7.99%. What do you conclude from your answers to b. and c.?

Problems from “Interest rates”

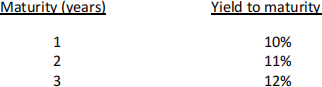

6. The current yield curve for default-free zero-coupon bonds is as follows:

a. What are the implied one-year forward rates?

b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will the pure yield curve (that is, the yields to maturity on one- and two-year zero-coupon bonds) be next year?

c. If you purchase a two-year zero-coupon bond now, what is the expected rate of return over the next year? What if you purchase a three-year zero-coupon bond? Ignore taxes. (Hint: Compute the current and expected future prices.)

7. Increasing prices erode the purchasing power of the dollar. It is interesting to compute what goods would have cost at some point in the past after adjusting for inflation. Go to the Federal Reserve Bank of St. Louis, FRED database website at https://fred.stlouisfed.org and find the consumer price index for all urban consumers. What would a car that cost $30,000 today have cost the year that you were born? (To find this, multiply the $30,000 by the price index in the year you were born and divide by the price index today.)

8. Answer each of the following two questions by drawing the appropriate supply-and-demand diagrams from the loanable funds theory framework discussed in class. (Hand drawn diagrams are fine. Principle, not precision, is what I am looking for.)

a. Using the supply-and-demand for bonds, show why interest rates are procyclical (rising when the economy is expanding and falling during recessions).

b. Suppose that many big corporations decide not to issue bonds, since it is now too costly to comply with new financial market regulations. Can you describe the expected effect on interest rates?

2023-06-13