ECON6008 Sample 1 Numerical Group Project

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECON6008

Sample 1

Numerical Group Project (Report)

Please find the attached mod. and m. files in the CODE .zip file .

Q1. mod is the Dynare file for question 1.

Q21. mod is the Dynare file for question 2 part 1.

Q22. mod is the Dynare file for question 2 part 2.

Q3. mod is the Dynare file for question 3.

Plot. m is the Matlab file to generate the graphs in the report .

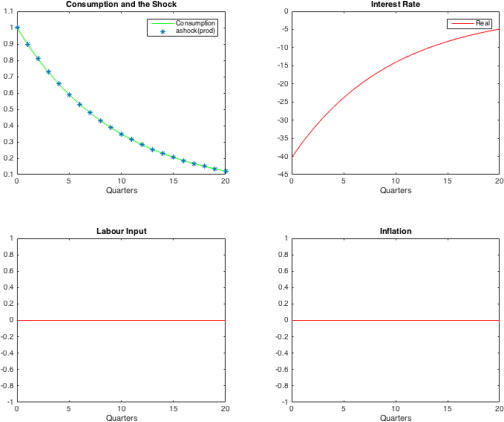

Q1. RBC, under a 1% productivity shock

Interpret the impulse response

The graphs show a 1% increase in productivity under the flexible pricing equilibrium and perfect competition (RBC) .

The shock will lead to 1% increase in output according to the production function . Output gap remains zero since there is no deviation of output from the potential output . Besides , there will be no change in the level of inflation . The productivity shock increases the real wage .

According to the model, these would lead to consumption to increase by the same amount as in the productivity, which is 1% .

Labor is independent of consumption in the household’s utility function, which means it remains constant . However, there is a decrease in the shadow price of consumption . As a result, real interest rate would fall (by around 40 basis points) as well .

As the productivity shock is a stationary AR (1) process, the effect diminishes toward zero in the limit and all real variables gradually converge to the zero deviation from the steady state .

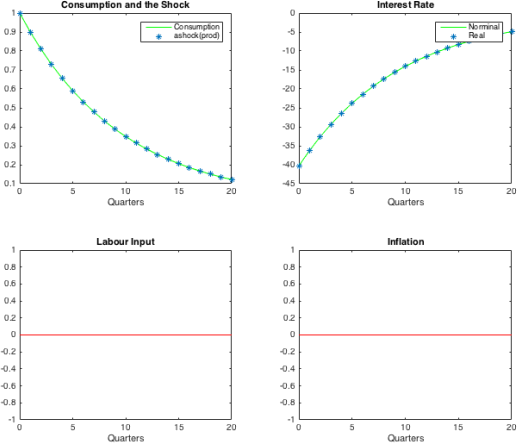

Q2. (1) NK with zero-inflation policy, under a 1% productivity shock

Interpret the impulse response

In the standard New Keynesian framework with a special case that the monetary policy authorities manage to keep net inflation to zero , the model is identical to the RBC model in question 1 and monetary policy would not affect any real terms . Hence the impulse responses of variables will be the same as those in the RBC model .

The shock will also lead to 1% increase in output . Output gap and inflation remains zero since it is identical to the flexible pricing . This increase in productivity increases the real wage . Consumption would increase by the same amount as in the productivity, which is 1% . Labor is independent of consumption in the household’s utility function, which means it remains constant . However, there is a decrease in the shadow price of consumption . As a result, real interest rate would as well . To accommodate the change in real interest rate, the central bank fully adjust the level for the nominal interest rate .

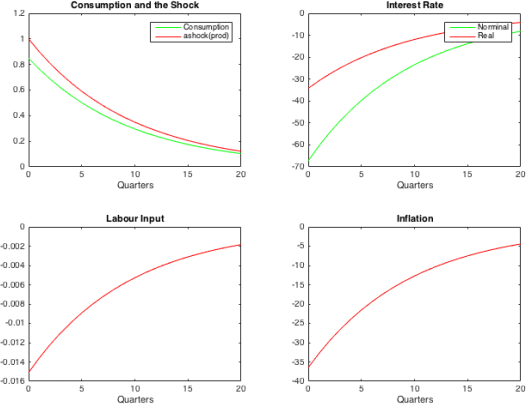

Q2. (2) NK with Taylor-like rule, under a 1% productivity shock

Interpret the impulse response

The graphs show a 1% increase in productivity, under the NK model with Calvo sticky price , monopolistic competition and Taylor-like monetary policy rule . As the productivity shock is a stationary AR (1) process, the effect diminishes toward zero in the limit as well .

Comparing to RBC, this model incorporates price stickiness and monopoly power of the firms . In the model, 1% increase in productivity will lead to a less than 1% increase in the real output and consumption (around 0 .85%) . Inflation will also decrease by less than 1% (around 37 basis points) . These are because monopoly power will lead to relatively lower output level and some prices are sticky and remain unchanged for a period of time .

Since potential output would increase by 1% , the output gap will be negative . As for labor input, it will decrease since income effect of decrease in prices dominates the substitution effect .

Since output gap and inflation both go down , policy authorities will respond by decreasing the nominal interest rate according to the policy rule . The real interest rate will go down as well (but will be less negative than the nominal interest rate due to negative inflation) . Thus , output gap will increase and be closer to zero, which in turn makes inflation closer to zero .

Which policy rule yields higher welfare for the household? What can you say about the role of the values of τπ and τy for the ability of the above Taylor rule to mimick the allocation under the optimal Ramsey policy?

In a Ramsey policy, monetary policy affects welfare through minimizing the level and the variations in these distortions if possible . In a simple interest rate rule, the authorities could accommodate the expectations of household utility around the Ramsey steady state . Given the equilibrium equations of the model and the assume policy rule, the authorities search for τπ and τy that maximize the level of welfare for the household . As a result, the second rule yields a higher welfare .

In the above NK model with Taylor like rule, we need to choose the coefficients to minimize the gap between Ramsey policy and this policy should be as close as possible . These two coefficients, τπ and τy shows the how important the inflation deviation (relative price distortion) and output gap (markup distortion) to the central bank in terms of stabilizing the economy .

Different coefficients would have different effects on stabilizing the economy . For example, if τπ is smaller than 1, a decrease in inflation would lead to less than one to one decrease in nominal interest rate, which will lead to an increase in real interest rate . As a result, the negative output gap and negative inflation will further decrease , and this would not be a stationary equilibrium . If τπ is larger than 1, a decrease in inflation is response by a more than proportionate decrease in nominal interest rate, which will lead to a decrease in real interest . Decrease in real interest rate shifts aggregate demand curve to the right , and lead to a higher output for a given inflation . Then higher output will further lead to higher inflation . As a result, the output gap and inflation will increase . This response would stabilize the economy . If policy authorities respond strongly enough to the productivity shock, the output gap and inflation can be stabilized at 0 level . And productivity does not lead to policy trade-off between output gap and inflation .

In contrast, in flexible price model (RBC), money have the attribute of neutrality . Central bank can affect the short term nominal interest rate only . Any changes in nominal interest rate will be absorbed completely by 1 to 1 increase in inflation and expected inflation, so it does not affect the real interest rate, real interest rate is only affected by real factors . So MA will not have any effect on output, and it can only affect inflation .

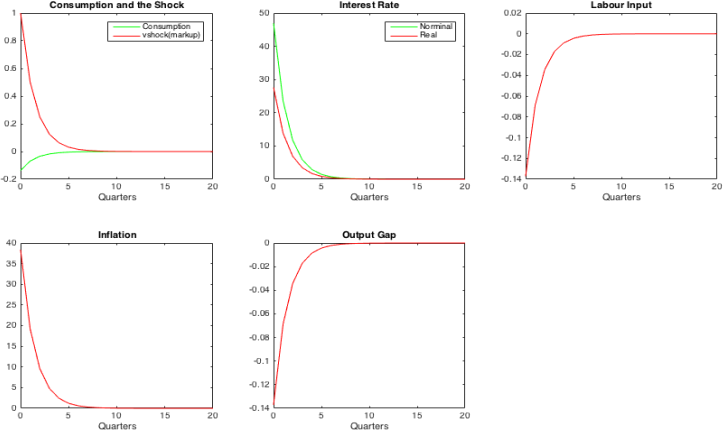

Q3. NK with Taylor-like rule, under 1% markup shock

Interpret the impulse response and policy trade-off

Here is a 1% positive mark-up shock, under the NK model with Calvo sticky price and monopolistic competition, with Taylor-like rule . As the productivity shock is a stationary AR (1) process, the effect diminishes toward zero in the limit as well .

The mark-up shock increases the cost of production and the price level, which leads to a decrease in demand . As a result, the society would face an increase in inflation and a decrease in real output and consumption . Labor input will decrease as there will be a decrease in wage and the substitution effect dominates the income effect .

As the temporary shock does not affect the long run potential output, output gap would become negative . Due to a negative output gap and a positive inflation level, the monetary policy authority will face a trade-off between closing the output gap and reduce the level of inflation . If authority decides to simulate the economy , i .e . decrease the nominal interest rate , the negative output gap will be smaller , but the level of inflation will be higher (more positive) . If authority decides to conduct a contractionary policy, i .e . increase the nominal interest rate, the inflation will be pinned down while the output gap will be more negative . Output and consumption will decrease as well . So it is not possible to stabilize these two factors at the same time .

2023-05-25