MATH 262 FINANCIAL MATHEMATICS

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

MATH 262

FINANCIAL MATHEMATICS

Question 1

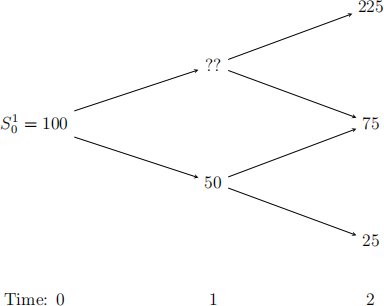

Consider a binomial model market with interest rate i = 12%, two time periods N = 2 (three time points T = {0, 1, 2}), one risky asset S1 , where the prices of S1 (at each time point) are given by

(a) Find the missing price (justify your answer) [4 marks]

(b) Find all fair prices at each node for a European put option (on the risky asset) with strike K = 110 and maturity T = 2. [7 marks]

Question 2

Consider a market with time horizon N = 1, d = 2 risky assets, an interest rate i = 10%, a probability space Ω = {1, 2, 3, 4}, where P({ω}) = ![]() for any ω ∈ Ω . The initial prices of the risky assets are S0(1) = 80 and S0(2) = 85, and their final prices at time 1 are S1(1) and S1(2), where for any ω ∈ Ω,

for any ω ∈ Ω . The initial prices of the risky assets are S0(1) = 80 and S0(2) = 85, and their final prices at time 1 are S1(1) and S1(2), where for any ω ∈ Ω,

Find an arbitrage. [6 marks]

Question 3

Consider a market model with d = 1 risky asset, time horizon N = 1, interest rate i = 10%, a probability space Ω = {1, 2}, where P({1}) = ![]() , and P({2}) =

, and P({2}) = ![]() . The risky asset has an initial price S0(1) = 110, and a final price S1(1) at time 1, where for any ω ∈ Ω,

. The risky asset has an initial price S0(1) = 110, and a final price S1(1) at time 1, where for any ω ∈ Ω,

Let (Fn )n=0,1 be the filtration given by F0 = {∅ , Ω}, F1 = σ(S1(1)). Find the equivalent martingale measure(s). [7 marks]

Question 4

Let Ω be a probability space. The following two questions are independent.

(a) Let (Dn )n≥0 be a sequence of independent {−1, 1} valued process with P(Dn = 1) = ![]() = P(Dn = −1) and assume that for n ≥ 1, Fn is generated by D1 , . . . ,Dn and F0 := {∅ , Ω}. Define S0 := 0, and Sn := 对k(n)=1 Dk for n ≥ 1 and let Xn := Sn + 1 for n ≥ 0.

= P(Dn = −1) and assume that for n ≥ 1, Fn is generated by D1 , . . . ,Dn and F0 := {∅ , Ω}. Define S0 := 0, and Sn := 对k(n)=1 Dk for n ≥ 1 and let Xn := Sn + 1 for n ≥ 0.

Prove that (Xn )n≥0 is a martingale. [9 marks]

(b) Let (Fn )n≥0 be a filtration. Let (Xn )n≥0 be a martingale, (Mn )n≥0 be a supermartingale and let (Yn )n≥0 be an adapted process. Suppose that for any n ≥ 0, Mn = Xn −Yn , prove that (Yn )n≥0 is a submartingale. [7 marks]

2023-05-24