ECON113: ADVANCED ECONOMICS OF FINANCE SUMMER TERM 2022

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

SUMMER TERM 2022

CENTRALLY-MANAGED ONLINE EXAMINATION

ECON113: ADVANCED ECONOMICS OF FINANCE

Time allowance

You have 2 hours to complete this examination, plus an Upload Window of 20 minutes. The Upload Window is for uploading, completing the Cover Sheet and correcting any minor mistakes and should not be used for additional writing time.

If you have been granted SoRA extra time and/ or rest breaks, your individual examination duration will be extended pro-rata and you will also have the 20-minute Upload Window added to your indi- vidual duration.

All work must be submitted anonymously in a PDF file and you should follow the instructions for submitting an online examination in the AssessmentUCL Guidance for Students.

If you miss the submission deadline, you will not be able to submit your work via AssessmentUCL and you will not be permitted to submit the work via email or any other channel. If you are unable to submit your work due to technical difficulties which are substantial and beyond your control, you should apply for a Deferral via the AssessmentUCL Query Form.

Your work should not exceed 3000 words. This includes footnotes and any tables containing large amounts of text. The word count does not include your figures, mathematical formulae, data tables or tables with short amounts of text. If your submitted answer exceeds the permitted word count stated, Faculty Word Limit Penalties will apply as follows:

● For work that exceeds the specified maximum length by less than 10% the mark will be reduced by five percentage marks, but the penalized mark will not be reduced below the pass mark and marks already at or below the pass mark will not be reduced.

● For work that exceeds the specified maximum length by 10% or more the mark will be reduced by ten percentage marks, but the penalized mark will not be reduced below the pass mark and marks already at or below the pass mark will not be reduced.

Answer all questions from Part A, and the question from Part B .

Questions in Part A carry 10 per cent of the total mark each, and the question in Part B carries 50 per cent of the total mark.

In cases where a student answers more questions than requested by the examination rubric, the policy of the Economics Department is that the student’s first set of answers up to the required number will be the ones that count (not the best answers). All remaining answers will be ignored.

If you have a query about the examination paper, instructions or rubric, you should complete an As- sessmentUCL Query Form. Please note that you will not receive a response during your examination.

By submitting this assessment, you are confirming that you have not violated UCL’s Assessment Regulations relating to Academic Misconduct contained in Section 9 of Chapter 6 of the Academic Manual.

PART A

Answer ALL questions from this section. Present all work when computations are required. Each question in this section is designed such that it can be answered with 300 words or less.

A1 Explain what are the universal economic assumptions that lie behind the generality of the

Fundamental Asset Pricing Equation (FAPE) with a positive stochastic discount factor (SDF) and the existence of a risk premium in asset prices.

A2 John Cochrane has remarked that even though the field is called ‘asset pricing’ the focus is

almost exclusively on returns. Show which properties of returns compared to prices explain the focus on returns, and why expected excess returns in particular are the best indicator of an asset’s riskiness. Provide an example where this distinction between prices and returns is crucial and seems to result in paradoxical results.

A3 Over the last half century the structure of the economy and financial markets have changed

substantially. There has been a substantial fall in traditional manufacturing and rise in services and digital economy, substantial increases in inequality and indebtedness in many advanced economies as well as significant demographic shifts. Financial markets have seen the emergence of new investment strategies (e.g. hedge funds, private equity, algorithmic trading), new asset classes (e.g. securitization, cryptocurrencies) and substantial changes in trading technology. Discuss whether these long run trends and transformations, which may affect risk premia over time, represent challenges for applying the unconditional beta representation of the FAPE as well as the applicability of FAPE itself.

A4 You have been invited to teach asset pricing to economic undergraduate students. Briefly discuss

two costs and two benefits of teaching CAPM compared to teaching the general asset pricing theory based on no-arbitrage using the FAPE with SDF.

A5 It is often said that options are ‘dangerous’ . Using the following example, show how options can

indeed be dangerous (lead to more risk taking, bigger losses), but can also make investments safer. Briefly explain the main characteristic of options that means they can be both dangerous and a great hedge. The price of a non-dividend paying asset is currently £50 and both an at-the-money call and an at-the-money put on this asset cost £5 each. The probability that in 3 months’ time the price will be above £50 is 60%. The expected price of the asset conditional on it being above £50 is £60, and the expected price of the asset conditional on it being below £50 is £45. Lastly, there is only a 2% chance the price will fall below £20 in 3 months’ time.

PART B

Answer ALL the sub-questions from the question below. Each sub-question in this section is designed such that it can be answered with 300 words or less. Remember to present all work and be explicit about all formulas and assumptions used in your answers. Answers without explanations and/or derivations will be given no credit.

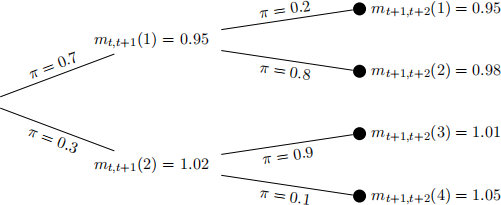

B 1 Consider an economy with three periods (t; t + 1; t + 2), with 2 states (st+1 = 1; 2) in the second

period t + 1 and 4 states (st+2 = 1; 2; 3; 4) in the third period t + 2. Every agent in this economy can freely trade a complete set of Arrow-Debreu securities. The diagram below shows the evolution of the stochastic discount factor (SDF) consistent with no-arbitrage in this economy. In the diagram below, mt+k,t+k+1(j) denotes the SDF at period t+k for state j in period t+k+1, for k = 0; 1.

(a) The preferences of the representative agent in this economy are given by U (ct; ct+1; ct+2) = Et [ k=〇∶2 ![]() k u (ct+k)], with u\ > 0 and u\\ < 0 and

k u (ct+k)], with u\ > 0 and u\\ < 0 and ![]() > 0. Explain what can be said about the pattern of aggregate consumption across time and states in this economy if

> 0. Explain what can be said about the pattern of aggregate consumption across time and states in this economy if

i. ![]() 5 1

5 1

ii. ![]() = 0:99

= 0:99

(b) Compute all the spot and forward interest rates consistent with no-arbitrage in this economy

and explain why the Expectation Hypothesis holds or not.

(c) One asset in this economy, asset A, pays {xA,t+2(1); xA,t+2(2); xA,t+2(3); xA,t+2(4)} = {100; 100; 50; 50} in period t + 2 and nothing in period t + 1.

i. Compute the 1-period expected excess returns in period t and t + 1 and explain the intuition for their pattern.

ii. What type of real world asset might have payoffs resembling those of asset A?

(d) Consider both a put and a call option on asset A, both with a strike price of 75 and expiring in t+2.

i. Explain which option (the put or the call above) should achieve a higher 2-period expected excess return in period t.

ii. Explain why you can or cannot generate a complete market by trading only in a risk-free bond, asset A and any call or any put options on asset A.

2023-04-24