IC208 - Programming for Finance Seminar 6

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

IC208 - Programming for Finance

Seminar 6 – Solutions

Q1)

There has been a substantial body of empirical work on the role of the financial system in promoting economic growth. For example, King and Levine (1993) estimate cross-sectional growth regressions (using data from a number of countries) of the form:

gi = a + ![]() fi +

fi + ![]() 1x1,i + ... +

1x1,i + ... + ![]() mxm,i + ui

mxm,i + ui

where

gi = growth in per capita GDP for country i

fi = financial development indicator (ratio of credit to GDP) for country i x1,i , ... , xm,i = control variables for country i

ui = error/disturbance term for country i

The control variables include per capita GDP, secondary school enrollment, ratio of government consumption to GDP, inflation and openness (=ratio of imports+exports to GDP).

References

King, R.G. and Levine, R. (1993). Finance and growth: Schumpeter might be right. Quarterly Journal of Economics 108, 717-737.

Levine, R. (1997). Financial development and economic growth: views and agenda. Journal of Economic Literature 35, 688-726.

Levine, R. (2004). Finance and growth: theory and evidence. Forthcoming in Agion, P. and Durlaf, S. Handbook of Economic Growth. Elsevier.

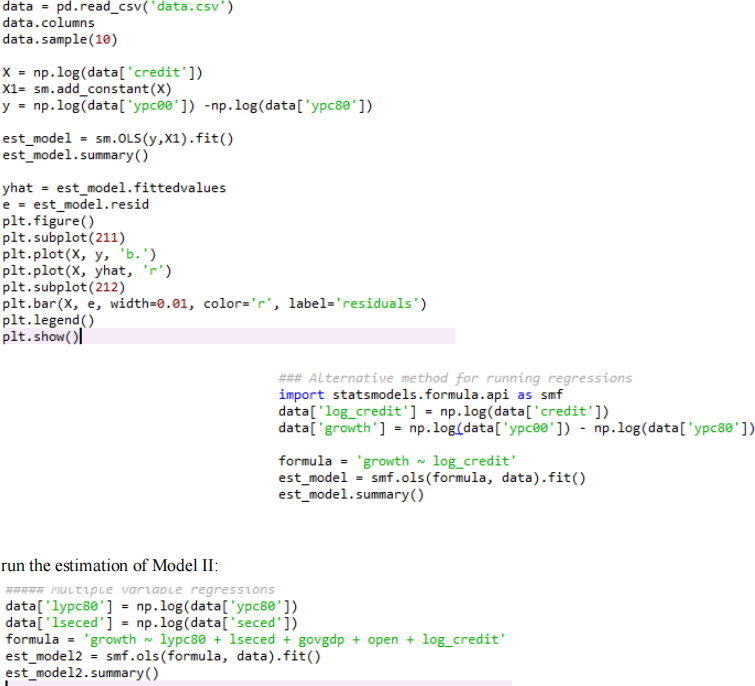

The file ‘data.csv’ contains cross-sectional data for 37 countries for the following variables:

|

ypc80 = |

Per capita GDP in 1980 (US dollars) |

|

ypc00 = |

Per capita GDP in 2000 (US dollars) |

|

govgdp = |

Ratio of government expenditure to GDP in 1980 |

|

open = |

Ratio of (exports+imports) to GDP in 1980 |

|

seced = |

Proportion of secondary school age population enrolled at secondary school in 1980 |

|

credit = |

Private credit by deposit money banks and other financial institutions to GDP in 1980 |

i-subscripts on the above variables refer to country i.

You have following tasks:

a) estimate the two cross-sectional regression models, as follows: I: dlypci = ![]() 1 +

1 + ![]() 2crediti + ui

2crediti + ui

II: dlypci = ![]() 1 +

1 + ![]() 2lypc80i +

2lypc80i + ![]() 3lsecedi +

3lsecedi + ![]() 4govgdpi +

4govgdpi + ![]() 5openi +

5openi + ![]() 6crediti + ui b) Visualise the above models

6crediti + ui b) Visualise the above models

Solution

Estimation of Model I:

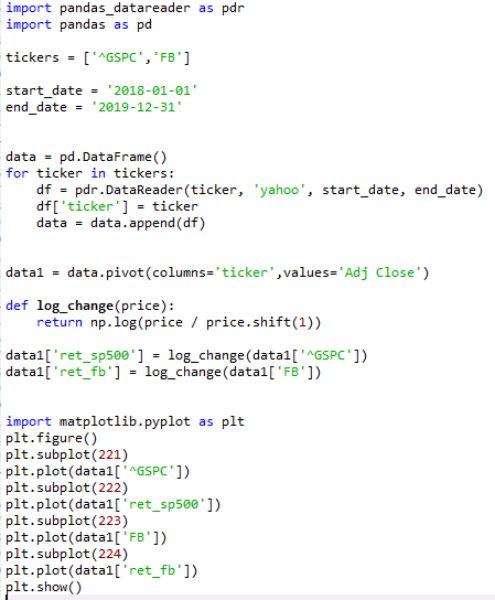

Q2) Write Python code to download historical data for S&P500 and Facebook from an online repository and plot the respective indices as a time series, and their respective returns.

Q3) Estimate a regression analysis of CAPM for Facebook. Is there any prior literature on the empirical evidence of CAPM? Is your result consistent with them?

Solution

Further independent reading is required for the sub-questions on the linkage to prior literature on CAPM.

2023-03-18