MATH0031 Exercises 6 2023

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

MATH0031 Exercises 6

2023

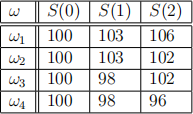

1. (a) Consider the following filtration, where the interest rate r = 0:

S(t) is the asset price at time t in dollars.

(i) In this model, replicate the European call option with strike K = $101 over the two periods and so find the fair price of the option.

(ii) Find all the conditional probabilities for this filtration and the corresponding probability on Ω = {ω1 , ω2 , ω3 , ω4 }. Confirm that EQ [X] is the fair price.

2. (Use the filtration above). A trader sells 6 (six) European call options to a client for the option premium. For every path ωi explain how the trader creates a portfolio at each time step in order to deliver the option payoff to the client at expiration. Demonstrate that this trading strategy is self-financing.

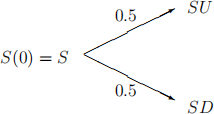

3. A one-period model where the initial stock price is S has equal proba- bility of going up to SU or down to SD at time T where U = 1/D and U > 1.

Assuming rates are zero show that there must exist an arbitrage op- portunity.

2023-03-05